Barbeque Nation Hospitality operates 164 casual-dining restaurants under brand names, including Barbeque Nation, Toscano, La Terrace and Collage. Barbeque Nation is the primary brand of the company under which it owns and operates 153 restaurants (147 national and six international) across 77 cities in India. The brand serves North Indian cuisine under the concept of over-the-table barbeque. Also, the company has acquired a 61.35 per cent stake in Red Apple through which, it operates 11 Italian restaurants.

The Rs 4,236 Bn food-service market (in FY20) of India is fairly cluttered with a substantial presence of unorganised players. Since the opening of the first Barbeque Nation restaurant in 2006, the company has grown the number of restaurants slowly, with as many as 71 restaurants being added to the chain during FY17-20. While casual-dining restaurants attract customers mainly during weekends, Barbeque served 9.92 Mn customers in FY20, with major sales (53.4 per cent) during weekdays and lunch covering at a healthy 44.4 per cent.

COVID-19 has had a negative impact on the hospitality business. The closure of restaurants, coupled with a growing tendency to avoid crowded places, led to falling footfall. Even though the economy has now opened, the company did not recover to the pre-COVID level as of November, 2020, as it operated 156 restaurants out of 164, while monthly sales only improved to 84.2 per cent compared to the year-ago period. In a bid to drive growth, the company focused more on the delivery business. In line with this, it launched UBQ by Barbeque Nation brand for food delivery and relaunched its app BBQ (2.2 Mn downloads as of December 2020). Its delivery business scaled up quickly, accounting for around 16 per cent of eight-month sales till November 2020.

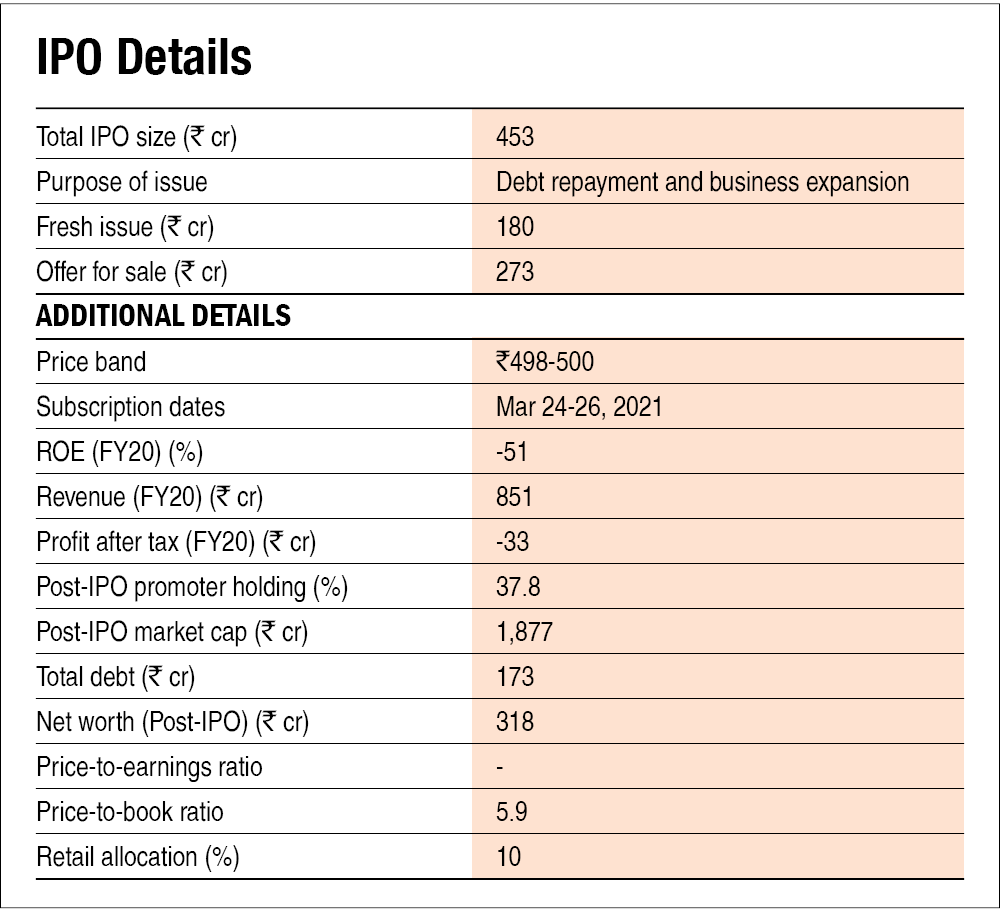

In a pre-IPO placement, the company has recently raised around Rs 150 crore at a price of Rs 252 (compared to the Rs 500 issue price). Out of the net proceeds of Rs 130 crore from the IPO, the company intends to use Rs 75 crore to repay debt, with the remaining for opening 26 new restaurants in FY 22-23. Although the company has been loss-making for the last couple of years, the management expects that the reduction of the outstanding debt post IPO, along with lowering depreciation costs (as its restaurants mature), would yield profitability sooner than later.

Strengths

- Over the years, the company has been able to build a steady network of 147 Barbeque Nation restaurants across 77 cities in India. Good coverage and the maintenance of quality experience have translated into a strong brand recall.

- Unlike other casual-dining restaurants which derive a majority of their revenues over weekends, the company derives more than 50 per cent of its sales during weekdays and around 45 per cent of it comes from lunch.

- In FY20, the company served around 9.92 Mn customers, with the average bill size at Rs 762.

- The company doesn't follow a franchise model and intends to run all its outlets by itself, thereby ensuring quality control.

Risks/Weaknesses

- COVID-19 has severely affected the company's business. It recorded a loss of Rs 100 crore for eight months ending November 2020 and its equity turned negative. Although 156 of its 164 stores were operational and sales had returned to 84 per cent of the pre-COVID levels by the end of November 2020, a growing number of cases can further dent the company's business.

- Some promoters of the company are involved in SEBI proceedings in relation to certain non-compliances under security-related laws. Further, one of the promoters is also involved in cases related to criminal and insolvency proceedings.

- The company reported lacklustre same-store sale growth of just 7.2 per cent, 5.6 per cent and -2.6 per cent, in FY18, FY19 and FY20, respectively.

- The delivery business (16 per cent of the revenue till NovFY21) can result in brand dilution for the dine-in brand over the long term.

- The company's subsidiary, Red Apple, runs a casual-dining Italian restaurant chain. In the past, the company's diversification into the burger chain (Johnny Rockets) failed. Hence, the performance of this segment needs to be monitored.

- The issue price at Rs 500 is at a steep increase to the recently conducted pre-IPO fundraise of Rs 150 crore done at Rs 252.

IPO Questions

The company/business

1. Are the company's earnings before tax more than Rs 50 crore in the last twelve months?

No, although the TTM (trailing twelve months) numbers are not available, the company has reported a loss before tax of Rs 126.5 crore in the eight months period ending November 30, 2020.

2. Will the company be able to scale up its business?

Yes. Out of the Rs 130 crore net proceeds from the fresh issue, the company intends to use Rs 55 crore towards setting up new outlets. It costs roughly Rs 2.1 crore to set up a new outlet, while the management suggests that break-even is achieved in a span of two-four months. The company has a target of opening 26 outlets in FY22-23, which it should be able to achieve from the fund to be raised.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes. Barbeque Nation is a very well-recognised brand. The company has been a pioneer in developing live barbeque-concept-based dining. Unlike other casual-dining restaurants which experience traffic mainly on weekends, Barbeque gets around 50 per cent of its revenue during weekdays, which shows its strong recognition among corporate customers.

4. Does the company have high repeat customer usage?

No. The experience of dine-in provided by the company has been replicated by other restaurants, thereby leading to low repeat customer usage. Although the company has a customer loyalty program wherein points can be redeemed during the customer's next dine-in visit or delivery order from the BBQ app or website, this program contributed around only 9.6 per cent to the customer bills for the month of December 2020.

5. Does the company have a credible moat?

No. The company provides a barbecue experience for its customers. However, several other players with similar service experience have started in recent years.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

Yes. The company is basically a restaurant chain primarily operating in India. Being a part of the organised food-service industry, it is expected to maintain heightened levels of hygiene. However, the company is sufficiently safe from regulatory risks.

7. Is the business of the company immune from easy replication by new players?

No. Over recent years, the company's concept of over-the-table barbeque has been copied by many other players. Besides, there aren't any particular differentiating factors that cannot be easily replicated.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes, the company derives around 94 per cent of its revenue from the Barbeque Nation brand of restaurants wherein it serves North Indian cuisine. North Indian cuisine accounts for 26 per cent of Indian food services and isn't likely to be substituted.

9. Are the customers of the company devoid of significant bargaining power?

No. The Rs 4,236 Bn food services industry in India is a very competitive market, with around 60 per cent of it coming from unorganised players. Within organised players, multiple formats, such as QSR (quick-service restaurant), casual dining and others, are there. Hence, customers have many options to choose from.

10. Are the suppliers of the company devoid of significant bargaining power?

No. Costs of food and beverages account for around 30-35 per cent of the company's total revenue. The company doesn't have any particular contract with any suppliers. Additionally, the small size of the company's operations gives its suppliers sufficient bargaining powers.

11. Is the level of competition the company faces relatively low?

No. The company faces substantial competition from organised and unorganised food services players, such as other casual-dining restaurants, QSRs and others.

Management

12. Does any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, the promoter and promoter group will collectively hold 37.8 per cent of the stake in the company post-IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

No, the top three managers do not have a combined experience of more than 15 years. Also, its Chief Financial Officer, Mr Amit V Betala, joined the company in January 2020.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

Yes, there are several outstanding litigation cases against the company and its promoters.

16. Is the company's accounting policy stable?

Yes, we have no reasons to believe otherwise.

17. Is the company free of promoter pledging of its shares?

No, one of the promoters of the company, Mr Kayum Dhanani, has pledged his stake for a personal loan. However, the pledged stake is just over 2 per cent of the total promoter and promoter group holding in the company.

Financials

18. Did the company generate the current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

No, the company has been posting losses in the last three years, which has led to a negative return on equity. The current and average three-year ROCE stood at 7.3 per cent and 9.6 per cent, respectively.

19. Was the company's operating cash flow positive during the previous year and at least three out of the last four years?

Yes, the operating cash flows have been positive in the last three years.

20. Did the company increase its revenue by 10 per cent CAGR in the last two years?

Yes, the company's revenue has grown at a rate of 20 per cent annually in the last two years.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

No, the company has a debt of Rs 173 crore, with a negative equity of Rs 12 crore as of November 30, 2020. However, post the Pre-IPO fundraise of Rs 150 crore and fresh issue from IPO of Rs 180 crore, the equity would rise to around Rs 340 crore post listing. Also, the company intends to reduce its outstanding debt of Rs 143 crore (as of January 2021) to Rs 68 crore using the IPO proceeds.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes. The company has a negative working-capital cycle, as it receives cash upfront while payments to suppliers, employees and others are made later. This provides the company with ample liquidity to run day-to-day affairs.

23. Can the company run its business without relying on external funding in the next three years?

Yes. The company has recently raised around Rs 150 crore for improving its liquidity. Further, around Rs 75 crore from the fresh issue is going towards the repayment of the debt, while the rest Rs 55 crore will be used for expansion. With this much liquidity, the company will be able to fund its growth plans without relying on external capital.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

No, its short-term borrowings have more than doubled in the last two years and stood at Rs 38 crore as of November 30, 2020.

25. Is the company free from meaningful contingent liabilities?

No, the company had contingent liabilities of Rs 59 crore as of November 30, 2020, most of which are related to indirect and direct tax proceedings against the company.

The stock/valuation

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No, the stock delivered an operating yield of 2.4 per cent on its enterprise value based on FY20 numbers.

27. Is the stock's price-to-earnings less than its peers' median level?

NA. The company reported losses in the last financial year ending March 31, 2020.

28. Is the stock's price-to-book value less than its peers' median level?

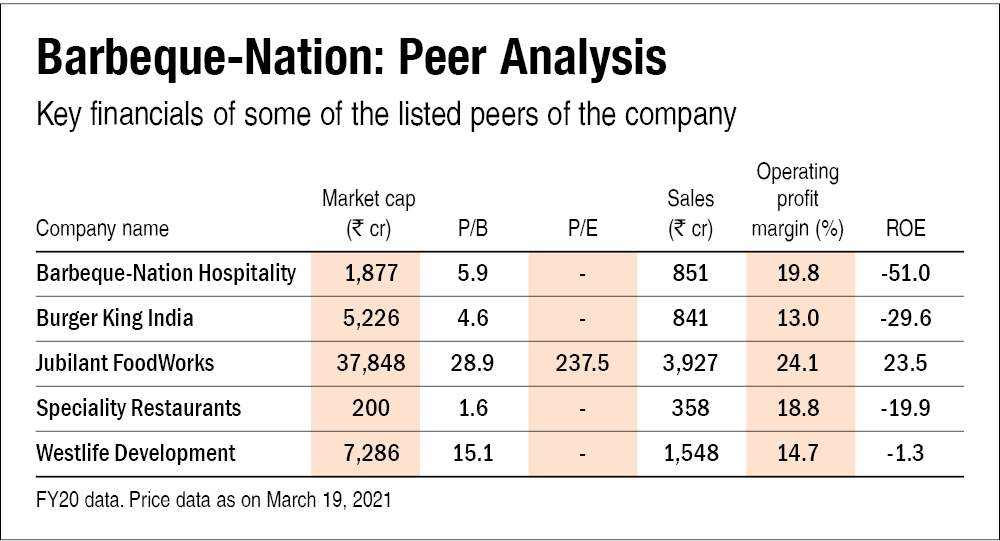

No. At the upper end of its price band, the stock's P/B ratio, on a post-IPO basis, is 5.9, which is higher than its peers' median P/B of 3.6.

Disclaimer: Authors may be an applicant in this Initial Public Offering.

Ask Value Research ![]()