Incorporated in 1989 and promoted by Mr. Ravi Goenka, Laxmi Organics is a leading manufacturer of acetyl intermediates and specialty intermediates in India. At present, the company is amongst the largest manufacturers of ethyl acetate, a widely used solvent in paints, coatings, perfumes and pharmaceuticals, with a market share of approximately 30 per cent. Also, the company is the only manufacturer of diketene derivatives in India, having a market share of 55 per cent and one of the largest portfolios in diketene products.

The company's products find application in various high-growth industries, including pharmaceuticals, agrochemicals, dyes and pigments, printing and packaging, and inks and coatings, to name a few. Also, the company plans to diversify into manufacturing of fluorochemicals through its acquisition of Miteni, a manufacturer of organic fluoro specialities.

Strengths

- Laxmi organic has been one of the largest exporters of ethyl acetate to Europe from India since 2012.

- The company has a diversified customer base across high-growth industries with marquee clients such as Alembic Pharma, Dr. Reddy's Lab, Laurus Labs and UPL Ltd., to name a few.

- Currently, the company has two strategically located manufacturing facilities with close proximity to several ports in Maharashtra.

- In addition to India, the company has a high global presence, exporting its products to over 30 countries. Its exports constituted more than 22 per cent of its revenues as of September 30, 2020.

Risks

- Though the company's manufacturing facilities are strategically located, they fall under one geographical area. Thus, any social or political unrest could impact its operations.

- The CBI and ED have initiated criminal proceedings against one of the directors of the company. Also, the promoter has been booked under the Factories Act, for a criminal proceeding.

- The company is vulnerable to industrial hazards and regulatory scrutiny since it deals with critical chemicals.

- The company has a high dependence on some of its suppliers. Its top 10 suppliers accounted for more than 78 per cent of its total expenditure as of September 30, 2020.

IPO Questions

The company/business

1. Are the company's earnings before tax more than Rs 50 crore in the last twelve months?

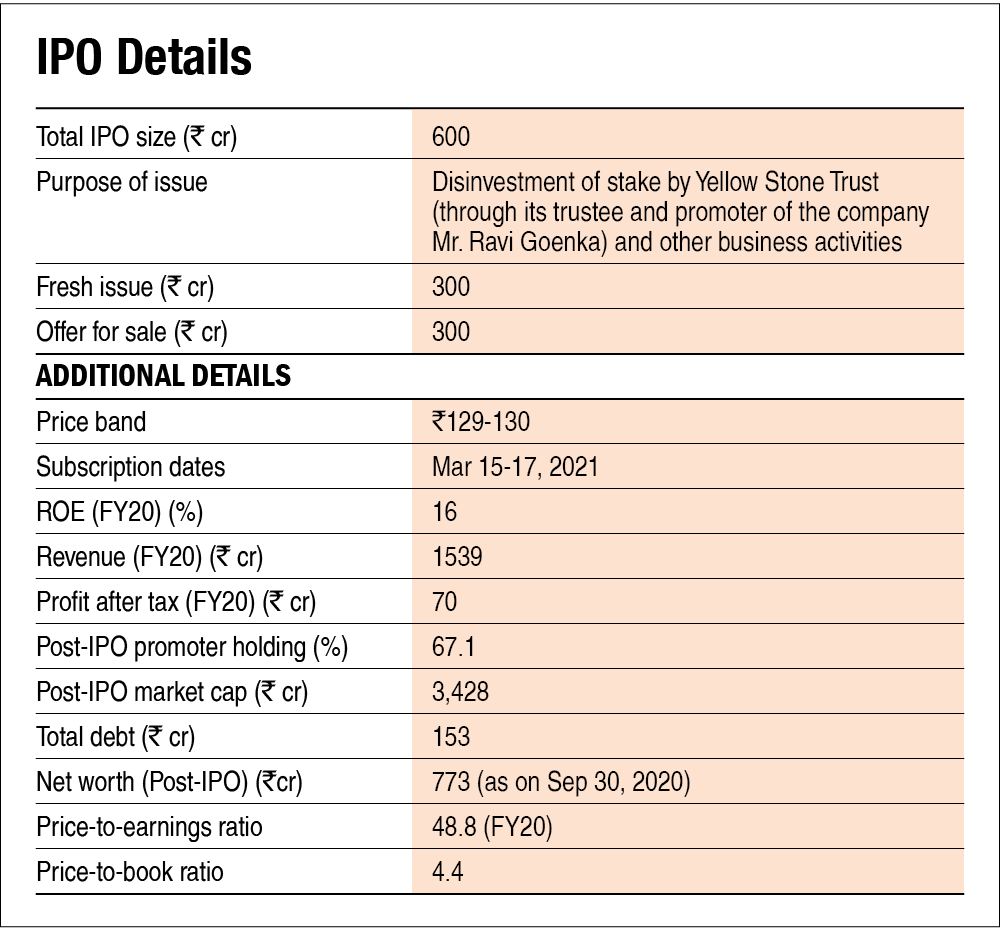

Yes, though the TTM (trailing twelve months) numbers are not available, the company has reported earnings before tax of Rs 56 crore in the six-month period ending September 30, 2020.

2. Will the company be able to scale up its business?

Yes, apart from its ethyl and diketene manufacturing businesses, the company is also venturing into fluoro specialty chemical business to expand its product lines and is deploying a portion of the proceeds from the fresh issue towards its capital expenditure.

3. Does the company have recognizable brand/s, truly valued by its customers?

N/A, the company's products find its application in a number of industries such as pharmaceuticals, agrochemicals, dyes and pigments, inks and paints, and coatings, and it's primarily engaged in B2B business. Hence, the need for an established brand is limited for the company.

4. Does the company have high repeat customer usage?

Yes, the company has established long-standing relationships with marquee customers across various industries, especially in the pharmaceuticals and agrochemicals space. Also, the majority of its top 10 customers have been associated with the company for the last five years.

5. Does the company have a credible moat?

Yes, the company is the only Indian manufacturer of diketene derivatives with a market share of more than 55 per cent, rest of which India fulfils through imports. Increasing demand for pharmaceuticals and agrochemicals is likely to increase the consumption of diketene and its derivatives. Also, the company has been one of the largest Indian suppliers of diketene-based specialty intermediaries in Europe in the calendar year 2019, as per F&S report.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, operating in the chemical industry space, the company is subject to extensive environmental laws and regulations relating to environmental protection, hazardous waste management and pollution control. However, the company doesn't face any major geopolitical risks.

7. Is the business of the company immune from easy replication by new players?

Yes, the specialty chemical industry has high entry barriers due to the involvement of complex chemistries and high knowledge along with capital intensive, high quality standards and high R&D expenditures.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes, the specialty chemical business is low-volume and high value, handling complex chemistries. The company needs to continuously spend on R&D to produce such products, which cannot be easily substituted or outdated.

9. Are the customers of the company devoid of significant bargaining power?

No, the company has a diversified customer base in India and overseas. It supplies products to customers in more than 30 countries. However, there are several other manufacturers of specialty chemicals to choose from.

10. Are the suppliers of the company devoid of significant bargaining power?

No, the top 10 suppliers of the company constituted 78 per cent of its total expenditure on raw materials as of September 30,2020, which shows its dependence on a single or few suppliers. Thus, any disruption in the supply of raw materials could adversely impact its business.

11. Is the level of competition the company faces relatively low?

No, operating in a highly competitive industry, the company is required to compete with domestic as well as global peers in both its business segments.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, the promoter will continue to hold a 67 per cent stake in the company post-IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes, Mr. Ravi Goenka, Managing Director of the company, has been associated with the company for more than 30 years.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes, we have no reason to believe otherwise.

15. Is the company free of litigation in court or with the regulator, that casts doubts on the intention of the management?

No, there are three criminal proceedings against the directors of the company. However, they might not have any major impact on the company's operations.

16. Is the company's accounting policy stable?

Yes, we have no reason to believe otherwise.

17. Is the company free of promoter-pledging of its shares?

Yes, the promoter's stake is free of any pledging.

Financials

18. Did the company generate current and five-year average return on equity (ROE) of more than 15 per cent and return on capital employed (ROCE) of more than 18 per cent?

Yes, the company generated an average five-year ROE and ROCE of 18.8 per cent and 18.6 per cent, respectively. Although the current ROE and ROCE stood at 16 per cent and 16.1 per cent, respectively.

19. Was the company operating-cash-flow positive during the previous year and at least four out of the last five years?

Yes, the company's operating cash flow has been positive in the last five years except for FY18.

20. Did the company increase its revenue by 10 per cent CAGR in the last five years?

No, the company's revenue grew at a rate of 7.4 per cent (CAGR) in the last five years.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest coverage ratio more than 2?

Yes, the company's net debt-to-equity ratio stood at 0.15 as on September 30, 2020.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes, the company's working capital stood at around 7.6 per cent of its sales and its working capital days stood at 25 days as of FY20.

23. Can the company run its business without relying on external funding in the next three years?

Yes, the company plans to use the fresh proceeds from the IPO for various purposes including its expansion plans, funding its working capital requirements and repayment of its borrowings. This will reduce its dependence on external funding in the next three years.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes, the company's short-term borrowings have declined from Rs 139 crore in FY18 to Rs 34 crore in FY20.

25. Is the company free from meaningful contingent liabilities?

No, the company's contingent liabilities stood at more than 37 per cent of its equity as of September 30, 2020, most of which were the guarantees issued by the company on behalf of its subsidiaries to their lenders.

The stock/valuations

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No. Based on the post-IPO enterprise value of Rs 5754 crore and the company's trailing twelve month operating earnings as of December 2020, the yield would be around 2.5 per cent.

27. Is the stock's price-to-earnings ratio less than its peers' median level?

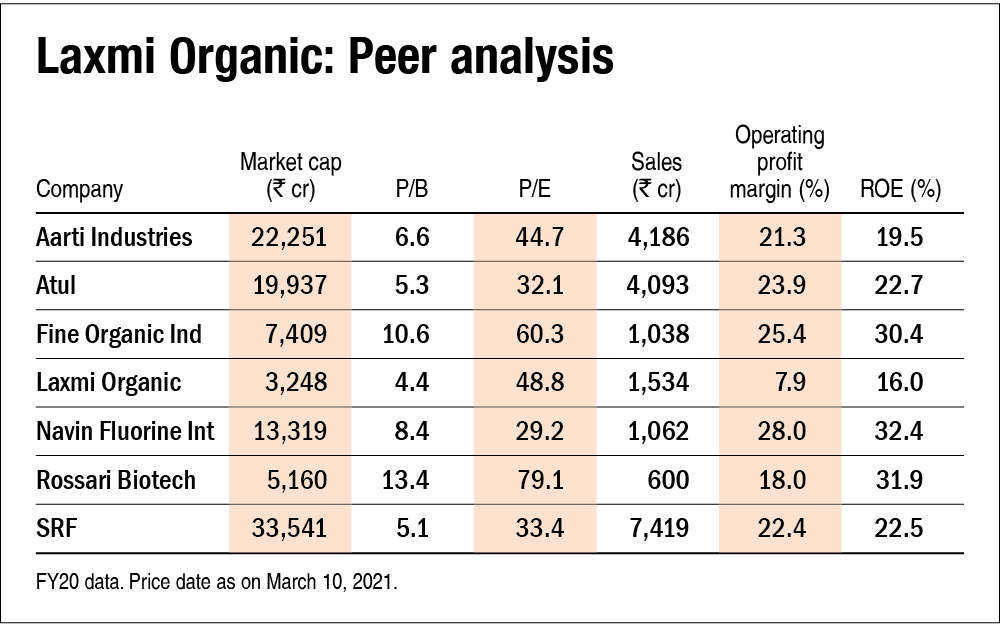

No. As TTM numbers are not available, so based on March 2020 earnings, the stock would trade at a P/E of around 48.8, which is way higher than its peers' median P/E of 39.1.

28. Is the stock's price-to-book value less than its peers' average level?

Yes. Based on equity post the IPO, the stock would trade at a P/B of around 4.4, which is lower than its peers' median P/B of 7.5.

Ask Value Research ![]()