Incorporated in 1999, MTAR Technologies is a leading precision-engineering solutions company, engaged in manufacturing mission-critical precision components with close tolerance. This means that these products are manufactured with high accuracy and perform critical tasks and precision movements consistently over longer repeat cycles. Since its products and components are mainly used for critical applications, such as aviation, aerospace, space, defence and nuclear power plants where errors can cause severe damage, the company needs to ensure all its products and components are high-quality and error-proof.

The company primarily caters to customers in the nuclear, space and defence and clean-energy sectors. With its biggest customer, Bloom Energy, in the US involved in generating power through renewable energy sources, the company has a major focus on the clean-energy sector. MTAR Technologies derived around 50 per cent of its revenue in the nine months ending December 31, 2020, from Bloom Energy. Nuclear Power Corporation of India Ltd. (NPCIL) is another major customer. Customers from the nuclear segment accounted for 27 per cent of its revenues as of December 31, 2020. Besides, the company is also a key supplier of mission-critical assemblies and components to the Defence Research and Development Organisation (DRDO) and Indian Space Research Organisation (ISRO).

Strengths

- The company lays great emphasis on research and development of its manufacturing processes in order to achieve design specifications with accuracy irrespective of product sizes.

- As on December 31, 2020, the company had an aggregate order book of Rs 336.1 crore. Out of this, 80.1 crore, 93.1 crore and 160.6 crore were from the clean-energy, nuclear and space and defence sector, respectively.

- Its client base includes some of India's leading organisations in the nuclear, space and defence sectors, such as the NPCIL, Indira Gandhi Centre for Atomic Research, ISRO and DRDO.

- Its expertise in designing critical and customised products for its clients has enabled it to establish long-lasting relationships with them, thereby leading to business growth.

- The 'Make in India' and 'Atmanirbhar Bharat' initiatives and an import ban on certain defence items have paved the way for the development of the domestic defence industry.

Risks

- Out of the top 39 customers, its top three customers accounted for more than 80 per cent of its revenues as of December 31, 2020. Thus, the loss of any of them could significantly affect the company's business.

- The liberalisation of the defence sector has paved the way for private and foreign players to participate in defence contracts. Therefore, the company will face more competition while bidding for such contracts.

- MTAR Technologies is involved in manufacturing mission-critical components with extremely low tolerances. Thus, adherence to quality standards is very critical and any deviation from this could severely impact its business.

IPO Questions

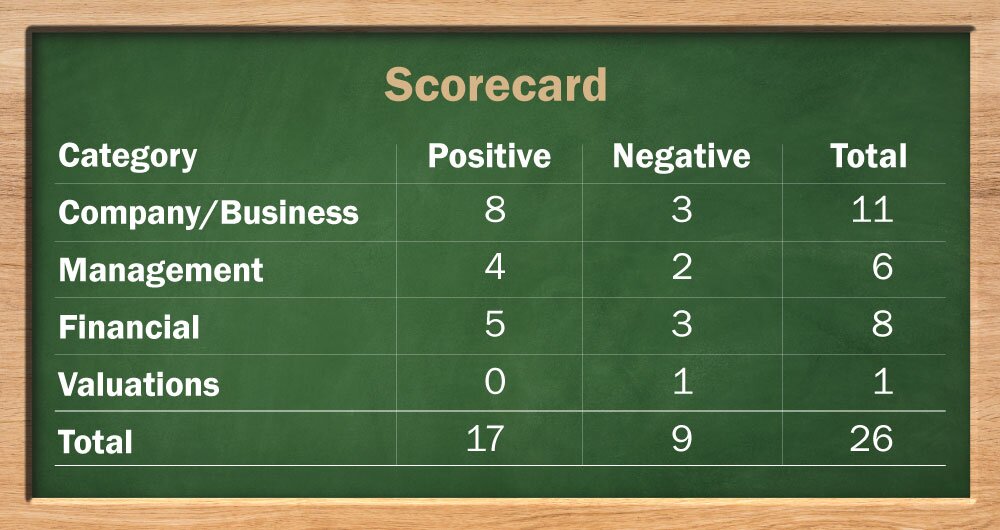

Company/business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

Yes, the company reported earnings before tax of Rs 52 crore on the TTM (trailing twelve months) basis as on December 31, 2020.

2. Will the company be able to scale up its business?

Yes, the increasing demand for nuclear-power-generating plants, the growing demand for clean energy, defence and space equipment will lead to an increase in the demand for critical-precision components, which will allow the company to expand its business operations.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes, the company has been successfully supplying products, such as liquid propulsion engines to ISRO for over three decades and critical components to DRDO for over four decades for their programmes of national importance.

4. Does the company have high repeat customer usage?

Yes, the company has long-standing relationships with some of its marquee customers, such as Bloom Energy, the Nuclear Power Corporation of India Ltd. (NPCIL) and ISRO, which contribute more than 80 per cent to its total revenues.

5. Does the company have a credible moat?

Yes, although the company faces stiff competition from its competitors present in similar business lines, having long-standing relationships with ISRO, DRDO and NPCIL in India can be a great moat for the company.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, owing to the nature of its operations, the company is subject to various environmental laws, such as The Environment Act, Water Act and Air Act, to name a few.

7. Is the business of the company immune from easy replication by new players?

Yes, even though the engineering-manufacturing industry is very fragmented, established players with developed technological expertise can be an entry barrier, especially in the precision engineering sectors such as defence, nuclear and space.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes, the company manufactures products in accordance with its customers' specific business needs and product requirements, which leads to increased customers' dependence on the company. It allows its products to withstand being easily substituted.

9. Are the customers of the company devoid of significant bargaining power?

No, as the company operates in a very fragmented market, its customers have the option to switch to other competitors present in the industry.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes, the company has a strong and diversified supplier base for sourcing raw materials and in certain cases, like in the space and defence sectors, critical and sensitive raw materials are directly procured and supplied by its customers.

11. Is the level of competition the company faces relatively low?

No, the company faces stiff competition from Larsen & Toubro, Godrej & Boyce in the precision-engineering components of the space and defence sectors.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, the promoters and the promoter group collectively hold a 62 per cent stake in the company.

13. Do the top three managers have more than 15 years of combined leadership at the company?

No, the top three managers do not have a combined experience of 15 years.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

No, material litigation is going against the company.

16. Is the company's accounting policy stable?

Yes, we have no reason to believe otherwise.

17. Is the company free of promoter pledging of its shares?

Yes, the promoters' shares are free of pledging.

Financials

18. Did the company generate current and five-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

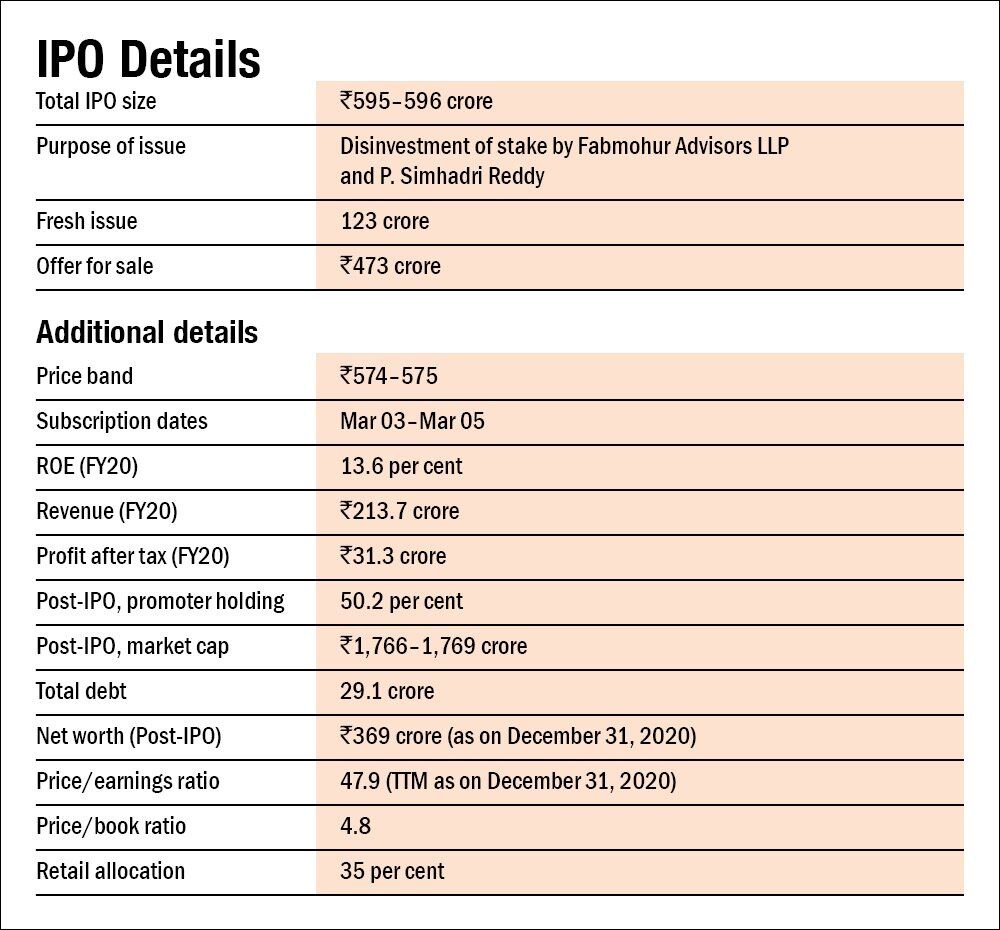

No, the company generated average ROE and ROCE of 5.1 per cent and 8.3 per cent, respectively, in the last five years. However, the current ROE and ROCE stand at 13.6 per cent and 19.4 per cent, respectively.

19. Were the company's operating cash flows positive during the previous year and at least four out of the last five years?

Yes, the company's operating cash flows were positive in the last five years.

20. Did the company increase its revenue by 10 per cent CAGR in the last five years?

Yes, the company's revenue grew at a rate of 21.5 per cent annually in the last five years.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

Yes, the company's net debt-to-equity stood at 0.18 as on December 31, 2020.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

No, the company's working capital stood at around 26.5 per cent of its sales and working-capital days stood at 153 days as of FY20.

23. Can the company run its business without relying on external funding in the next three years?

Yes, the company plans to use part of the proceeds from the IPO to fund the working-capital requirements in the next three years.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

No, the company's short-term borrowings have more than doubled in the last three years.

25. Is the company free from meaningful contingent liabilities?

Yes, as of December 2020, the quantum of contingent liabilities stood at Rs 3.2 crore, which was just 1.3 per cent of the total net worth.

Stock/valuations

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No, the stock offers an operating yield of 3.2 per cent post-IPO based on TTM numbers as on December 31, 2020.

27. Is the stock's price-to-earnings less than its peers' median level?

NA, there are no listed companies whose business portfolio is comparable with the company's business. However, the stock current P/E stood at 47.9 based on December 31, 2020 numbers.

28. Is the stock's price-to-book value less than its peers' average level?

NA, there are no listed companies whose business portfolio is comparable with the company's business. However, the stock current P/B stood at 4.8 based on December 31, 2020 numbers.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()