Incorporated in 2000, Indigo Paints is a fast-growing manufacturer of decorative paints, including emulsions, enamels, wood coatings, distempers, primers, putties and cement paints. It is the fifth-largest company in the Indian decorative paint industry in terms of revenue as of FY20. The company claims to be the first one to manufacture various differentiated products, such as Metallic Emulsion, Tile Coat Emulsion, Bright Ceiling Coat Emulsion, Dirtproof and Waterproof Exterior Laminate and so on.

The Indian decorative industry was valued at Rs 403 bn in 2019, wherein the organised sector (10 to 12 players) accounted for 77 per cent. Indigo Paints is a relatively small-sized company, with a market share of 2 per cent. The company owns and operates three manufacturing facilities in India, with a total installed capacity of 101,903 kilolitres per annum (KLA) for liquid paints and 93,118 metric tonnes per annum for putties and powder paints. Apart from this, the company plans to increase its liquid-paint capacity by another 50,000 KLA through the fresh issue from the IPO. Also, the company has been delivering high profitability by increasing its return on equity to 24.3 per cent in FY20 from 10.1 per cent in FY18 on the back of higher sales growth and margin expansion.

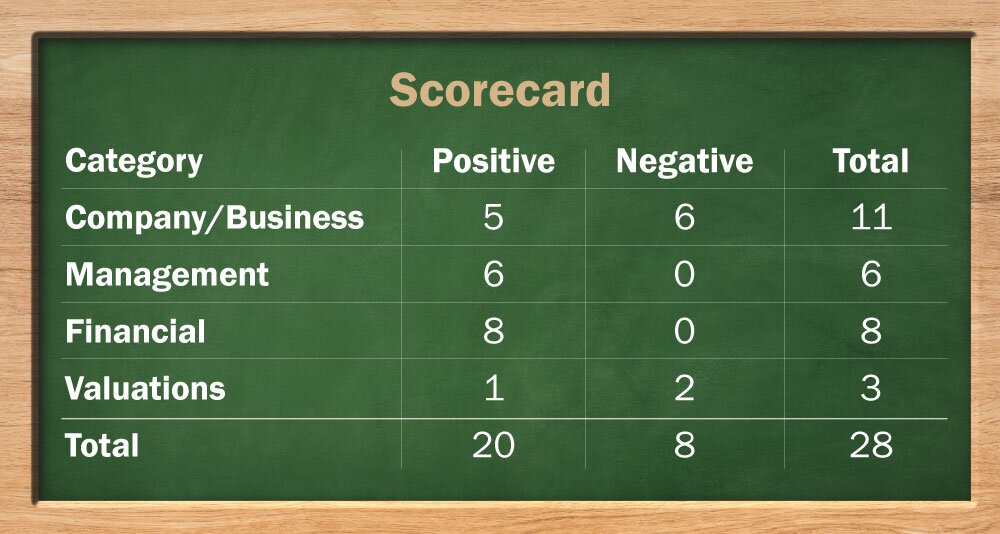

Strengths:

- Bottom-up approach: The company started its distribution with tier-3, tier-4 cities and rural areas where brand penetration was easier and gradually, started strengthening its presence across tier-1 and 2 and metro cities, which were already dominated by its large competitors. This strategy has resulted in profitable growth for the company.

- Differentiated products: Around 28 per cent of the company's revenue comes from its differentiated products, which have high margins due to their low presence among large competitors and less discount offered on these products.

- Building brand image: The company has been spending aggressively on advertisements and sales promotion, which accounted for 12.6 per cent of its revenues in FY20. On the other hand, the spend of the top four paint companies was in a range of 3.8 to 5.8 per cent. The company has also roped in Mahendra Singh Dhoni, a sportsperson with the pan-India appeal, as its brand ambassador.

- Extensive distribution network: The company has been expanding its distribution network at a rate of 10.4 per cent per annum since FY18, which has been more than that of Berger Paints and Akzo Nobel.

- Fast-growing industry: The decorative paint industry is expected to grow at a CAGR of approx. 13 per cent over the next three years (Source: F&S report) on the back of higher disposable income, a shorter demand cycle for re-painting, and government initiatives such as 'Housing for All'. Also, there has been a gradual shift towards the preference for decorative paints over the conventional whitewash.

Weaknesses:

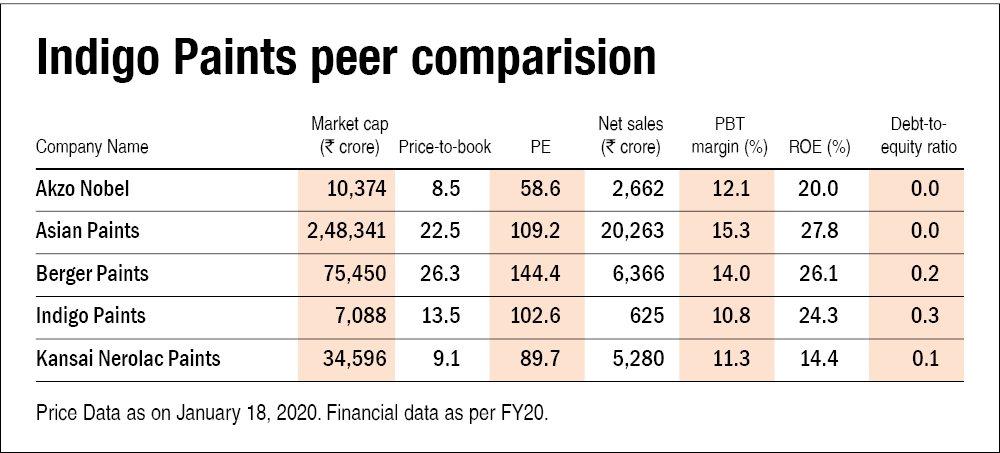

- High competition: The company has a total market share of just 2 per cent with a dealer base of around 11,000 but has a long way to go as compared to the industry leader 'Asian Paints' who has a dealer base of more than 70,000 dealers and a market share of 42 per cent.

- Tinting machines: Around 40 per cent of its dealers have tinting machines (which are used to generate different colour shades as per the customer's requirement) as against 90 per cent of Asian Paints and 65-70 per cent of Berger Paints.

- Revenue concentration: Although the company has a presence in 27 states, a majority of its revenue comes from Kerala, which contributed 34.5 per cent to the total revenue in FY20. Thus, any adverse events, such as social, political or economic disruption in its major market could have a material impact on the company's business.

Total IPO size: Rs 1,169-1,170 crore

Purpose of issue: Stakes sale by private equity firms, Sequoia Capital, SCI Investments

Offer for sale: Rs 869-870 crore

Fresh issue: Rs 300 crore

Additional details

Price band: Rs 1,488-1,490

Subscription dates: Jan 20-Jan 22

ROE (FY20): 24.3 per cent

Revenue (FY20): Rs 625 crore

Profit after tax (FY20): Rs. 48 crore

Post-IPO, promoter holding: Nil

Post-IPO, market cap: Rs 7,078-7,088 crore

Net worth (Post IPO): Rs 524 crore (as on Sep 30, 2020)

Price/earnings ratio: 102.6 (TTM as on Sep 30,2020)

Price/book ratio: 13.5

Retail allocation: 35 per cent

IPO Questions

Company / Business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

Yes, the company reported earnings before tax of Rs 91 crore on the TTM (trailing twelve months) basis as on September 30, 2020.

2. Will the company be able to scale up its business?

Yes, the company operates in Indian decorative industry which is expected to grow at a rate of 13 per cent in the next three years and being a small-sized company, it has ample room for growth.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes, the company manufactures products under the name of its umbrella brand 'Indigo' which has a pan-India presence.

4. Does the company have high repeat customer usage?

No, the company operates in a highly competitive industry dominated by the industry leader, Asian Paints, which has a very high brand value. Thus, customers can easily switch to other brands.

5. Does the company have a credible moat?

No, as stated earlier, the company operates in a highly competitive industry dominated by Asian Paints. Although it is the fifth-largest company as per revenues, its market share is just 2 per cent as compared to the largest player with a market share of 42 per cent.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the company's operations are subject to extensive government regulations such as The Explosives Act and various other environmental laws. The company needs to obtain and maintain several permits and approvals from central, state and local governments for operating its business.

7. Is the business of the company immune from easy replication by new players?

Yes, the decorative paint industry has high barriers to entry, such as the requirement for an extensive distribution network, high capex requirements for providing tinting machines to dealers and the need of creating a distinct brand identity.

8. Is the company's product able to withstand being easily substituted or outdated?

No, although the company manufactures differentiated products which accounted for 28 per cent of its revenues in FY20, its remaining products face tough competition from its large peers.

9. Are the customers of the company devoid of significant bargaining power?

No, its customers have plenty of other options to choose from. Also, the company faces competition from several unorganised players in tier two-four cities and rural areas.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes, prices of the company's key raw materials are determined by the international demand and supply for those commodities. Thus, suppliers do not have any significant bargaining power.

11. Is the level of competition the company faces relatively low?

No, the company operates in the highly competitive decorative paint industry and competes with well-established companies like Asian Paints, Berger Paints, Kansai Nerolac and Akzo Nobel.

Management

12. Does any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, pre-IPO, the promoters of the company hold a 60 per cent stake in the company. Post-IPO, the promoters will hold a 54 per cent stake in the company.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes, Mr Hemant Jalan, MD and Chairman, has been associated with the company since 2000.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

Yes, there is no material litigation going on against the company.

16. Is the company's accounting policy stable?

Yes, we have no reason to believe otherwise.

17. Is the company free of promoter pledging of its shares?

Yes, the promoter's shares are free of pledging.

Financial

18. Did the company generate the current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

Yes, the current ROE and ROCE stood at 24.2 and 27.5 per cent respectively. Also, the three-year average ROE and ROCE were 17.5 and 18.2 per cent, respectively.

19. Was the company's operating cash flow positive during the previous year and at least four out of the last five years?

Yes, the company reported positive cash flows in four of the last five years.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes, the company's revenue has grown at a rate of 29.3 per cent CAGR in the last three years.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

Yes, the company is net-debt free.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes, the company's working capital stood at around 7 per cent of its sales and the working-capital days stood at 12 days as of FY20.

23. Can the company run its business without relying on external funding in the next three years?

Yes, the company plans to use the proceeds from the IPO for capital expenditure, especially for the expansion of existing manufacturing units. Also, the company has a low working-capital cycle of 12 days, which enables it to quickly realise cash for its sales.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes, the short-term borrowings were NIL as on September 30, 2020.

25. Is the company free from meaningful contingent liabilities?

Yes. However, the company has reported Rs 31 crore of contingent liability mostly pertaining to VAT (Value added tax) which accounts for around 6 per cent of its equity post-IPO.

The Stock/Valuation

26. Does the stock offer operating-earnings yield of more than 8 per cent on its enterprise value?

No, the stock will offer a yield of 1.03 per cent post-IPO based on March 2020 numbers.

27. Is the stock's price-to-earnings less than its peers' median level?

No, the stock's P/E ratio currently stands at 102.6, which is more than its peer average of 100.5.

28. Is the stock's price-to-book value less than its peers' average level?

Yes, the stock's P/B ratio currently stands at 13.5, which is less than its peers average level of 16.6.

BRLM- KotaK Mahindra Capital, Edelweiss Financial Services and ICICI Securities.

Disclosure: Author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()