Introduction

With an AUM of around Rs 2.78 lakh crore as of September 2020, the Indian Railway Finance Corporation (IRFC) is the market-borrowing arm of Indian Railways, the Ministry of Railways (MOR). IRFC's loan portfolio is divided into three segments:

- Rolling stock (55.3 per cent of September AUM): IRFC leases assets such as locomotives, coaches, wagons, etc., to Indian Railways.

- Project assets (42.4 per cent): IRFC has currently extended loans to MOR for various railway-infrastructure assets and national projects of the Government of India. These assets are still being developed and IRFC is yet to execute a leasing agreement with MOR. Currently, these loans are shown as advances against railway-infrastructure assets to be leased.

- Loans to other PSUs (2.2 per cent): It comprises unsecured loans given to Ircon (Indian Railway Construction Ltd) and RVNL (Rail Vikas Nigam).

IRFC gets bi-annual lease income from MOR. At the beginning of each fiscal, MOR provides the company with a target fund requirement based on its planned capital expenditure. The company meets this funding requirement by raising funds through various sources, including bonds, term loans and foreign loans.

During the period between the FY13-20, the company financed on average around 30 per cent of the capital outlay of Indian Railways every year. In FY20, the figure was pegged at 45 per cent.

The business model

IRFC is the financing arm of Indian Railways. Each year, once Indian Railways provides IRFC with a target fund requirement, the company raises funds through term loans and bonds. These proceeds are then utilised to fund rolling stocks and project assets (as defined in the intro). The procurement of such assets is done by MOR but the ownership and title remain with IRFC. Thereafter, IRFC and MOR enter into a leasing agreement, which defines the term period of the lease, terms of use of these assets, costs and various other business functionalities. IRFC leases such assets to MOR for a period of 30 years, which is considered valid for the economic life of these assets. At the end of each year, the company, in consultation with MOR, decides the margin be charged to MOR over the borrowing cost of the company. For FY20, the margins for rolling stock and project assets stood at 40 bps and 35 bps (100bps= 1 per cent), respectively, over the borrowing cost. While the lease income accounted for 80 per cent of the company's FY20 revenue, the remaining 20 per cent primarily derived from the interest on loans and the pre-commencement of the lease.

Strengths

- The company is the primary borrowing arm of Indian Railways. A strong relationship with Indian Railways, in-depth knowledge of asset classes (both rolling stock and project assets) and the government ownership provide the company with a competitive advantage.

- Since the company is government-owned and lends to a sovereign entity, the credit risk is minimised. Therefore, IRFC enjoys healthy credit ratings, which enables the company to borrow at lower costs. In FY20, the company's weighted average cost of incremental borrowing stood at 7.37 per cent as compared to 6.12 per cent yield on 10-year government securities as of March 2020.

- Despite being an NBFC, the company has a low-risk business model. Its liquidity risk (the risk of not meeting short-term debt obligation) is minimised, as MOR is required to cover any funding shortfall for meeting bond redemption or term loan maturity availed by IRFC. Further, hedging costs associated with foreign exchange-rate risk are also incorporated in the costs to MoR.

- The company follows a cost-plus business model, wherein it charges MOR a particular margin above its borrowing costs. The company's ability to charge a margin ensures its sustainable profitability.

Weakness

- IRFC lacks business diversification. The company services primarily one client - Indian Railways (MOR). As of September 2020, its loan book exposure to MOR was around 98 per cent, while loans given to other PSUs accounted for only 2 per cent.

- The company's growth primarily hinges on the growth in the capital outlay of Indian Railways. Over the past six years, the government has increased budget outlay for railways. As a result, the capital raised by IRFC more than doubled to Rs 66,300 crore in FY20 as compared to Rs 24,000 crore in FY16. Nevertheless, stretched fiscal deficit can force the government to reduce capital expenditure for railways in the coming years.

Risks

- Since the company's business is primarily dependent on financial needs of Indian Railways, any changes in borrowing policies of MOR, such as raising funds directly, public-private partnerships, etc., can have an adverse effect on the company's operations.

- The company's interest-coverage ratio (the assessment of a company's short-term financial situation) for the past three years till March 2020 stood at an average of 1.34, which is quite low. Although this risk is mitigated by the fact that MOR is required to fund any shortfall by IRFC for the redemption of bonds or maturity of loans, still during extraordinary situations if MOR is not able to fulfil such a requirement, it can adversely affect the business.

- Loans extended to IRCON and RVNL accounted for around 20 per cent of the company's September 2020 equity. Although these companies are government-owned and hence have low credit risk, default on these loans can wipe out 20 per cent of the company's equity.

- IRFC has extended advances to MOR under its project assets business segment. These advances are for those infrastructure assets that will be developed first and then will be leased in the future. The company is exposed to the project-execution risk in relation to these projects.

- With Indian Railways entering into public-private partnerships wherein private players are allowed to run their trains and other operations, it poses a threat to IRFC. Moreover, in the past three years till FY20, the share of IRFC financing total rolling stock of Indian Railways decreased from 93 per cent in FY18 to 76 per cent in FY20.

IPO Details:

Total IPO size: Rs 4,455-4,633 crore

Fresh issue: Rs 3,089 crore

Offer for sale: Rs 1,544 crore

Post-IPO promoter holding: 86.4 per cent by the govt of India

Additional details

Price band: Rs 25-26

Subscription dates: January 18-20, 2021

ROE (FY20): 11.6 per cent

Revenue (FY20): Rs 13,421 crore

Post-IPO valuation: Rs 32,671-33,978 crore

Equity (Pre-IPO): Rs 31,687 crore as of September 2020

Equity (Post-IPO): Rs 34,776 crore

BRLM: DAM Capital Advisors (Formerly known as IDFC Securities), HSBC Securities and Capital Markets, ICICI Securities, SBI Capital Markets

Management

1. Has the company been free of any regulatory penalties?

Yes, the company has been free from any regulatory penalties till date.

2. Does the company adequately provide for its non-performing assets (NPAs)? More specifically, is the ratio of provisions to Gross NPAs more than 50 per cent?

Yes, the company historically has not had non-performing assets as almost all of its leasing operations are conducted with MOR. Moreover, the company has been exempted by the RBI from asset classification, provisioning and exposure norms to the extent of its exposure to the MOR.

3. Do the top five managers have stock as a meaningful part of their compensation (More than 50 per cent)?

Not applicable. Since IRFC is a government-owned company, compensation through stock isn't meaningful.

Financial strength and stability

1. Does the company have fresh slippages to total advances ratio of less than 0.25 per cent? (Fresh slippages are loans that have become NPAs in the last financial year).

Yes, the company did not have any non-performing loans and accordingly, there were no slippages.

2. Did the company generate a current return on equity (RoE) of more than 12 per cent and return on assets (RoA) of more than one per cent?

Yes, the return on equity and return on assets as of September 2020 stood at 12 per cent and 1.3 per cent, respectively.

3. Did the company increase its loan book by 20 per cent annually over the last three years?

Yes, the company has managed to increase its AUM comprising lease receivables, loan assets and advances against railways infra assets by 31 per cent YoY till March 2020 from March 2018. Financial numbers before March 2018 are not comparable due to changes in lease accounting.

4. Did the company increase its Net Interest Income (NII) by 20 per cent annually over the last three years? (Net interest income is the difference between the revenue that is generated from a banks' assets and the expenses associated with paying out its liabilities).

Yes, the company generates the majority of its income from lease income by leasing rolling stocks to Indian Railways. As of March 2020, the net interest income (lease income + interest income - interest expense) increased by 20.7 per cent from that in March 2018, YoY.

5. Is there any direct relationship between the increase in loan book and the increase in Net Interest Income (NII)?

Yes. Although the financials available for a three-year time period is too less to draw a meaningful correlation, the company keeps a margin (around 30-40 bps) over the weighted average cost of capital while performing lending operations. Keeping the margin same, an increase in the loan book will directly translate into an increase in net interest income.

6. Is the company's capital adequacy ratio more than 15 per cent? (The capital adequacy ratio (CAR) is a measure of a banks' capital. It is expressed as a percentage of a banks' risk-weighted credit exposures).

Yes. Since the company mainly lends to Indian Railways which is backed by the Indian Government, the credit risk is low. That's why, the capital adequacy ratio as of September 2020 stood at 433.9 per cent.

7. Can the company run its business without relying on external funding in the next three years?

No. The company's business directly depends on the planned capital expenditure by MOR based on which, it raises funds through various sources, including bonds, term loans, external commercial borrowings, etc. A jump in planned capex by MOR can lead to an increase in the company's external funding needs.

8. Did the company generate an average NIM of more than 3 per cent in the last three years? (Net interest margin or NIM denotes the difference between the interest income earned and the interest paid by a bank or financial institution relative to its interest-earning assets like cash).

No. The company's three-year average NIM till March 2020 stood at around 1.6 per cent.

9. Is the Average Gross NPA Ratio (Gross NPAs/Total Advances) over the last three years less than 1 per cent and the Net NPA Ratio (Net NPAs/Total Advances) less than 0.5 per cent?

Yes. The company did not have any NPA for the last three years.

10. Does the company have a cost-income ratio of less than 50 per cent?

Yes. Since the company services only one client i.e Indian Railways and that too mainly in leasing services, its costs like employee wages, rent, etc., are negligible. As of March 2020, the cost-to-income ratio stood at 1.97 per cent.

Growth and business

1. Will the company be able to scale up its business?

No. The company is the market-borrowing arm of Indian Railways. Since it provides leasing services for rolling stock and project assets only to one client and works as a PSU, its scale of the business largely depends upon the growth of Indian Railways.

2. Does the company have a loan book of more than Rs 100,000 crore?

Yes. As of September 2020, the company had a total AUM consisting of lease receivables, loan assets and advance against railway infra assets worth Rs 2,78,007.6 crore.

3. Does the company have a recognisable brand truly valued by its customers?

Not applicable. The concept of brand isn't really meaningful for a company like IRFC. Such companies are established by the government to fulfil a specific role and most of the time, their customers don't have a choice to move to another company/brand.

4. Does the company have a credible moat?

Yes. The company is the sole financing arm of Indian Railways and in FY20, the company financed around 45 per cent of the capital outlay. Historically, this figure hovered around 30 per cent.

5. Is the level of competition faced by the company relatively low?

Yes. The company is the sole financing arm of Indian Railways when it comes to financing their rolling-asset needs. Though there isn't any obligation on MOR side to raise capital only through IRFC, a strong relationship, a deep understanding of the railway business and government ownership provides IRFC with an advantage over any other prospective competitor.

Valuation

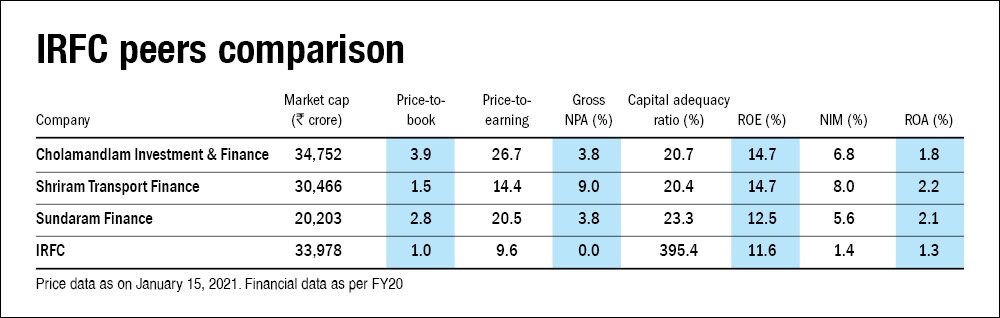

1. Is the company's price-to-earnings ratio less than its peer median level?

Yes. Based on post-IPO outstanding shares and TTM earnings till September 2020, IRFC will trade at a P/E of 9.6, which is lower than the P/E of 20, the median of its peers.

2. Is the company's price-to-book value less than its peer median level?

Yes. Based on post-IPO outstanding equity, IRFC will trade at a P/B of 0.98, which is lower than the P/B of 2.8, the median of its peers.

3. Is the company's PEG ratio less than one? (The price/earnings to growth ratio (PEG ratio) is a stock's price-to-earnings (P/E) ratio divided by the growth rate of its earnings for a specified time period).

No. Based on two-year earnings per share (EPS) growth rate till March 2020 and P/E based on March 2020 EPS, the PEG ratio stands at 1.46.

Disclosure: Author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()