It is mandatory for subscribers of the National Pension System (NPS) to buy an annuity plan with at least 40 per cent of their corpus at the time of exit on attaining the age of 60 unless the total corpus does not exceed Rs 5 lakh. The remaining 60 per cent of the corpus can be withdrawn as a lump sum and is tax-free. However, if a subscriber opts to exit prematurely before the age of 60, he needs to utilise at least 80 per cent of the corpus to buy an annuity plan and only 20 per cent of the corpus can be withdrawn as a lump sum.

Buying an annuity plan means that you will be investing the money with a company, usually an insurance company and in return, the company promises to pay you a certain amount every month or at the chosen frequency to ensure that the subscriber continues to get some sort of regular income after his retirement. Needless to say, the insurance company adds some amount to the corpus invested with the company as a return for our investments with it.

Some people tend to misuse the huge corpus that they get on retirement and often end up spending more in initial years. As a result, their later years of retirement are exposed to old-age poverty. This is one reason why NPS has made it mandatory for subscribers to utilise a part of the corpus to buy an annuity plan during the exit so that the subscriber gets only a certain amount every month to spend. The main objective of NPS is to secure the golden years of life financially. However, whether or not buying an annuity product is the most suitable way of deriving regular income is the subject of a separate discussion that we will do some other day.

Although annuity plans are sold by many insurance companies, an NPS subscriber can buy it only through one of the 12 companies empanelled with the Pension Fund Regulatory & Development Authority (PFRDA). The following is the list of Annuity Service Providers (ASPs) that are currently empanelled with PFRDA.

| S. No | Insurance companies empanelled with PFRDA as ASPs |

| 1 | SBI Life Insurance Co. Ltd |

| 2 | Life Insurance Corporation of India |

| 3 | Star Union Dai-ichi Life Insurance Co. Ltd |

| 4 | ICICI Prudential Life Insurance Co. Ltd |

| 5 | HDFC Life Insurance Co Ltd. |

| 6 | IndiaFirst Life Insurance Co Ltd |

| 7 | Edelweiss Tokio Life Insurance Co. Ltd (Annuity product is not yet operational) |

| 8 | Bajaj Allianz Life Insurance Co Ltd. |

| 9 | Canara HSBC Oriental Bank of Commerce Life Insurance co Ltd. |

| 10 | Kotak Mahindra Life Insurance Co Ltd. |

| 11 | Tata AIA Life Insurance Company Limited |

| 12 | Max Life Insurance Company Limited |

In addition to choosing the insurance company to buy their annuity plans, NPS subscribers need to decide the type of annuity they want to purchase at the time of exit. Different types of annuities are available, with some providing a fixed amount every month throughout your life, while some providing the said income to the subscriber's spouse after the subscriber's death. The following are the major types of annuity plans available for NPS subscribers.

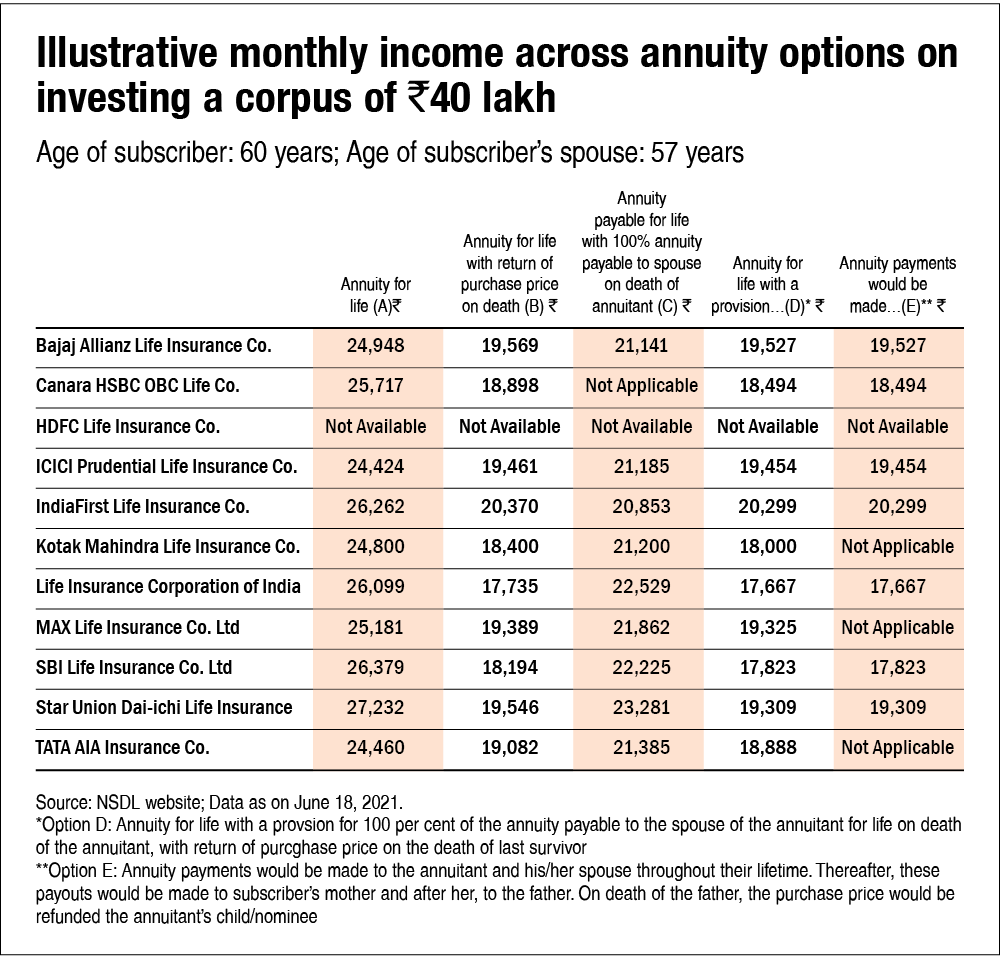

- Annuity for life: A fixed amount is paid every month to the subscriber throughout his life.

- Annuity for life with return of purchase price on death: Besides a fixed amount that is paid to the subscriber every month, an amount equivalent to the original investment is paid to the nominee on the death of the subscriber. However, under this plan, the amount of monthly income is usually comparatively less.

- Annuity payable for life with 100 per cent annuity payable to the spouse on the death of annuitant: As the name suggests, the monthly income continues to be paid to the spouse after the death of the subscriber.

- Annuity for life with a provision for 100 per cent of the annuity payable to the spouse of the annuitant for life on the death of the annuitant, with the return of purchase price on the death of the last survivor: This is precisely a combination of the second and third options mentioned above. Besides the continuation of the fixed monthly annuity that is payable to the spouse on the death of the subscriber, an amount equivalent to the original investment is paid to the nominee after the death of the last survivor.

- Annuity is payable to self, spouse, parents and then nominee: Annuity payments would be made to the annuitant and his/her spouse throughout their lifetime. Thereafter, these payouts would be made to the subscriber's mother and after her, to the father. On the death of the father, the purchase price would be refunded to the annuitant's child/nominee.

Wondering how much monthly income would you get under each option? Look at the following table which has been sourced from the NSDL website for a 60-year old who has decided to buy an annuity with Rs 40 lakh. NSDL is the Central Record Keeping Agency (CRA) for NPS. We have assumed the age of the spouse to be 57. The same link can be used to know how much pension one would get under various options on investing a different amount.

This article was originally published on August 27, 2021.

Ask Value Research ![]()