Much of the science of investing revolves around the holy grail of portfolio-building. A balanced investment portfolio can go a long way in obviating several worries that are normally associated with investing. For instance, consider the diversification aspect. A well-diversified portfolio can mitigate risk and reduce volatility, thus helping you sleep easy. However, the numerous emails and questions that we receive on portfolio problems suggest that for many of us the skill of portfolio-building remains elusive.

At Value Research, over the years, we have analysed countless investment portfolios. Two problems generally plague most: a large number of funds and the randomness of the collection, which seems to suggest that little thought has gone into selecting those funds. The reasons are not hard to understand. People begin with a few funds. Over a period of time, some of those funds do well and some don't, nudging investors to look for alternatives. Along the way, investors get fascinated by some hot theme or whatever is pitched to them by their distributor with a great story.

Another reason for a large number of funds is the flawed idea of diversification that many investors harbour. Equating fund investing with stock investing, they end up investing in several funds in order to diversify better. Since each fund itself is a cluster of several stocks, in reality, they end up owning many more stocks indirectly than one would expect to see in a stock portfolio. Virtually, they end up owning an index. With an 'index-like' portfolio, you can't expect index-beating returns.

Coupled with this is the problem of managing so many funds in terms of keeping a tab on their performance and developments, such as fund-manager change or change in the key objective.

It's teamwork after all

The funds in your portfolio should have a clear role to play just like the players in a sports team. Consider cricket. In a cricket team, there is a balance between batsmen and bowlers. There is a captain and a wicket-keeper. There are all-rounders and so on. What if there were all batsmen or bowlers? The outcome is anybody's guess. In a similar way, your portfolio must have the right balance. Its various components should play a complementary role.

Don't lose sight of your goal while building a portfolio. A well-designed portfolio doesn't just give better returns across cycles on average, it also helps contain volatility. It shouldn't give you negative surprises. Above all, it should help you achieve the goals for which you designed it in the first place.

Let's see how you can go about building a meaningful portfolio that is optimised as per your needs.

Narrowing down your options

In order to pick a cricket team, the board of selectors begins with a much larger set. The selectors then start removing the undesirable or undeserving names. Eventually, they have just 15 players, out of whom 11 actually play.

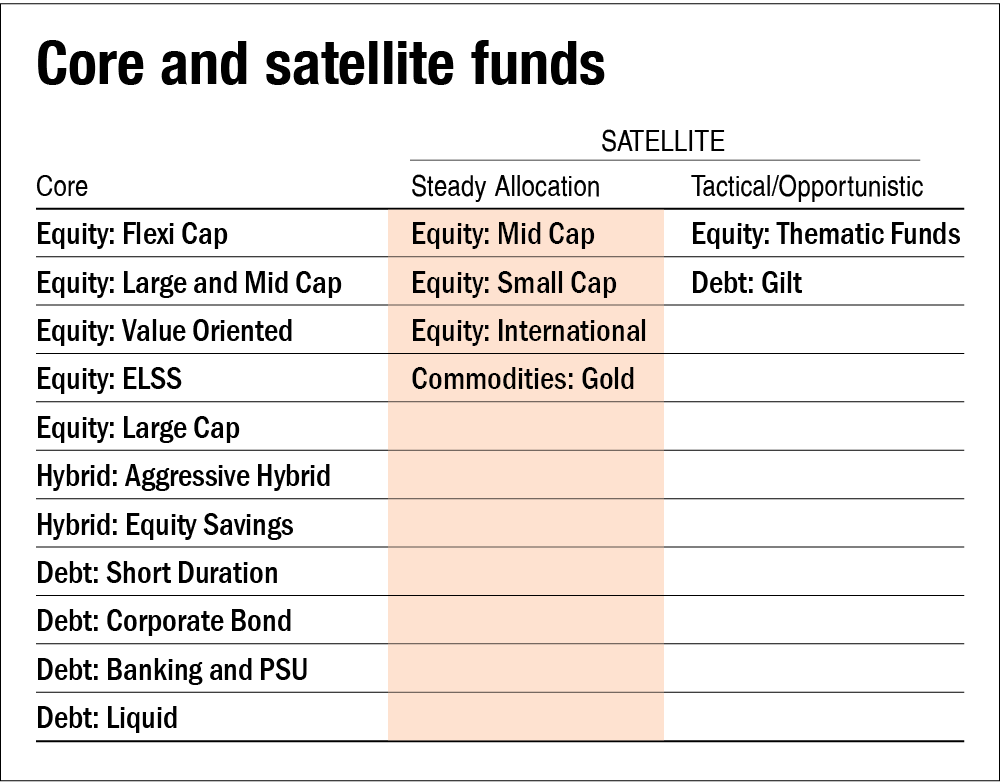

As a mutual fund investor, your set is the 36 mutual fund categories as per SEBI's classification. Not all of them are meant for you. So, the first step would be to narrow down this list. See the table 'Core and satellite funds'. It mentions those categories which are useful for retail investors. The rest can be discarded. Just because we discard some categories doesn't mean that there is something inherently bad with them. It's just that they are not suitable for most retail investors and hence would unnecessarily complicate making a choice.

Building a winning team

In a cricket team, there are a few core members who are almost always there and then there are another handful who play the supporting role and may change depending upon playing conditions, opponents, etc. Similarly, a portfolio should have a few funds at its core and then there could be some that are supplementary. The table mentions the categories that qualify as core and supplementary or satellite. Identify which ones are appropriate for you. For instance, flexi-cap funds should be the core of your equity portfolio as they can invest across companies of all sizes and hence provide you a balanced exposure. Those who want some extra mid- and small-cap exposure for a kicker to their returns can add one or two mid- and small-cap funds.

Classifying your options as core or satellite would ensure that you never go overboard on categories which are unfit to be in a dominant role. You often find that some or the other supplementary category small-cap, gold, gilt, etc.) is doing very well and one can get tempted to invest heavily in it. So, being clear about its role should act as a deterrent. Satellite categories can add a particular flavour to your portfolio but going overboard on them can give you negative surprises. For instance, in the example above, if your portfolio has a large exposure to small-cap funds, it will likely be more volatile and can give you the jitters amid a market slump.

Those who would like to keep things simple can just stick to core holdings and give the satellite allocations a complete miss. With core holdings alone, you can accumulate the corpus required for your goal.

Your core holdings

Core holdings are at the heart of your portfolio and constitute a dominant share of your total corpus. What makes a category a core holding? There are two requirements. First, a core category should be versatile, providing the flexibility to the fund manager to invest where he sees the maximum benefit. These funds should not be too restrictive in their investment mandate and be able to adapt their portfolios depending upon the situation. Second, a core category should take a balanced approach to risk and rewards. It should not be tilted towards a particular extreme.

In equity, flexi-cap funds fit these requirements as they can invest in companies of all sizes in any proportion without any restrictions on allocation to any market-cap segments.

In debt on the other hand, short-duration funds that maintain a portfolio with high-quality holdings help investors fulfil the need for steady returns with the safety of capital. Given their mandate to invest predominantly in securities that have maturities between one year and three years, they also have limited duration risk.

For first-time investors, aggressive hybrid funds can be a good choice. With their debt allocation of 20-35 per cent, they help contain volatility and thus allow new investors to accustom themselves to market volatility before they can take a plunge into pure-equity funds.

As far as the number of funds for your core holdings is concerned, two to three funds at a point in time are enough to provide proper diversification.

Your satellite holdings

Satellite or supplementary holdings are meant to play three roles: boost returns (example, small-cap funds), add stability (example, fixed-income allocation in an equity portfolio) or add diversification (example, gold, international equity). Further, there are supplementary funds which are meant to have a steady allocation over the long term, such as small/mid-cap funds or international equity. And then, there are others which are more opportunistic, where one needs to time the entry and exit well to make any meaningful gains, such as gilt funds or certain thematic funds.

For instance, an aggressive investor may want to allocate 25 per cent of his portfolio separately to mid- and small-cap funds and keep it that way for the long term. Another investor may want a component of international equity for better diversification and hence allocates about 25 per cent to it. He then keeps it this way for the long term, rebalancing his portfolio yearly. Many investors find gold as a good diversification tool and may want to allocate 5-10 per cent of their corpus to it.

On the other hand, some savvy investors may want an extra exposure to a particular category based on their judgement of market moves. Such an allocation is more opportunistic in nature and can be altered or liquidated as the prevailing trend subsides. For instance, someone who wants to have extra exposure to pharma stocks may want to add a pharma fund to his portfolio. He may later exit it as he realises that this theme has weakened or become overheated. A debt investor may add a gilt fund to profit from a cut in interest rates.

If you find adding satellite funds too much work, it's perfectly fine to give them a miss and keep things simple. Your goals won't be derailed in the absence of these. Such funds are meant for the more enterprising investor who doesn't mind taking extra risk to boost his returns or who is willing to go the extra mile to diversify his portfolio.

In fact, in some cases, it is very much advisable to keep it simple. For example, a first-time investor should just pick a couple of good aggressive hybrid funds and get going. Likewise, small investors looking to make humble monthly investments should stick to one or two good flexi-cap funds. Doing so will help prevent unnecessary confusion and complication that such investors may not be ready for. Remember starting early and investing consistently are more important than aiming for a perfect portfolio.

But there can be exceptions

What is described above is suitable for most investors. However, there can be exceptions based on your particular needs. For instance, consider a retiree's portfolio. It would be comprised majorly of safe avenues for a regular income, such as Senior Citizens Savings Scheme and short-duration funds. But in order to provide inflation protection, one-third of the portfolio can also be parked in flexi-cap funds. Similarly, a conservative equity investor may have a higher portion of debt in his asset allocation, say, 40 per cent.

So, what matters more than the guidelines above is to understand the spirit of these guidelines and adapt them as per your needs. If you need more help, soon you can use the Portfolio Planner tool on the Value Research website. This tool is a part of the Premium account.

Ask Value Research ![]()