Introduction

Angel Broking, the fourth largest broking firm in India as per active client accounts on NSE, provides broking and advisory services (75 per cent of the FY20 revenue), margin funding (9.5 per cent), loans against shares and financial products distribution to its clients. The company provides its services through online and digital platforms on the back of a network of more than 11,000 sub-brokers as on June 30, 2020. The company follows a flat fee-based model wherein it charges zero for delivery and Rs 20 per trade for intraday, F&O and commodity trades. It also provides margin funding for up to 79.55 per cent of the purchase value by the client. Margin trade funding is a practice wherein the broker lends to the investor against cash or securities as collateral. The investor is able to take leveraged bets and increase his/her profits using this facility. As on June 30, 2020, its margin trading facility book of Rs 768.70 crore was spread over 143,287 clients.

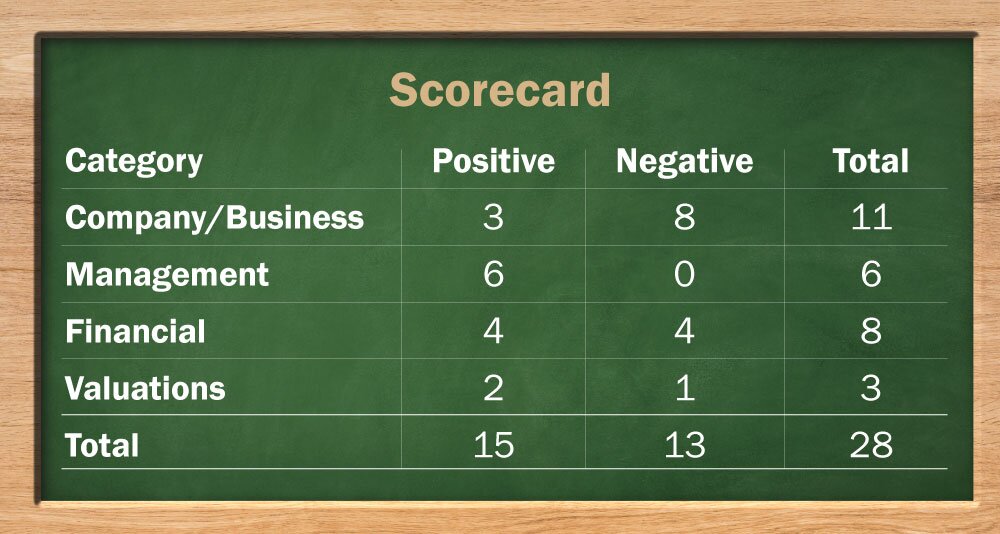

Strengths:

1) Scale and size: The company is the fourth largest retail broking house with around 6.3 per cent of active clients on NSE as of June 2020. With a network of more than 11,000 sub-brokers, along with a digital presence, it is able to reach the length and breadth of the country. Over the past three years until March 2020, Angel Broking managed to acquire more than 80 per cent of its clients from tier-2 and beyond cities. It is a reflection of its scale and size.

2) In-house research: The company also provides advisory services through its in-house research team of 54 members who are conducting both quantitative and qualitative research. Further, under the ARQ advisory, it provides rules-based investment advisory, which is based on the modern portfolio theory.

Weaknesses:

1) Business segment concentration: The company's main revenue source is the broking business, accounting for around 75 per cent of the total revenues. Unlike other brokerage houses that have managed to diversify themselves into wealth management, advisory services and others, Angel Broking hasn't been able to do such diversification.

2) Intense competition in commoditised business: Ever since the business model of broking firms moved towards a flat fee-based model, broking business has become more and more commoditised. Newer companies like Zerodha, Uptsox, Groww, etc., backed by PE firms can easily take away market share from legacy players.

Risks:

1) Regulatory risks: The company is subject to extensive supervision and regulation by various regulatory bodies. Any new change initiated by the regulatory body can materially impact the business. For example, SEBI has recently changed the margin-trading rules wherein a broking firm is now required to collect margin upfront from clients for any sale or purchase in the equity segment.

2) Dependence on macro-economic factors: The brokerage business depends on the number of the order executed and trading volumes, which are significantly affected by external factors like general economic conditions, the performance of capital markets, monetary policies and fluctuations in interest rates.

3) Data privacy issues: Technology-driven broking firms are now embarking on the use of artificial intelligence, machine learning and data analytics to use client data and offer them even more differentiated services. However, stringent data privacy laws can inhibit companies from collecting such client data.

What are the new margin-trading rules?

In view of the Karvy Stock Broking Fiasco last year wherein brokers breached their clients' trust by illegally pooling securities across clients without any authorisation, SEBI has come with new margin-trading rules. As per these rules, a client can individually pledge securities directly to the clearing corporation and the securities will continue to remain in the client's account. Clients will need to authorise a pledge request in favour of their brokers, who will then repledge it with clearing corporations for allowing margin benefits to the clients. Brokers are now mandated to collect upfront margins from their clients when it comes to purchasing and selling transactions. Any failure to comply with it will attract penalties. Until now, the new rule has had a mixed impact. Although the daily cash market turnover has fallen by up to 29 per cent since September 1 over the August level, the daily derivatives turnover has risen by 15 per cent during the same period. Its full impact remains to be seen in the coming time. From the broker's perspective, companies that are relying on legacy IT systems will have to adapt to and upgrade their technology quickly.

How would the IPO proceeds be applied

Fresh issue - Rs 300 crore

Offer for sale - Rs 300 crores

Ashok D. Thakkar(Promoter): Rs 18.34 crore

Sunita A. Magnani(Promoter): Rs 4.5 crore

IFC (International Finance Corporation): Rs 120 crore

Individual selling shareholders: Rs 157.2 crore

What will Fresh issue proceeds be used for

Out of Rs 300 crore from fresh issue, Rs 230 crore to be used for meeting working capital requirement

Additional details

Price Band - Rs 305-306 per share

Total IPO size - Rs 600 crores

Subscription Dates - 22nd to 24th September 2020

ROE (FY 20) - 14.7 per cent

Revenue (FY20) - Rs 730 crores

Post-IPO, promoter holding will fall from 55 per cent to 45 per cent (includes promoter group)

Post IPO valuation - Rs 2500 crores

Equity (Post IPO) - Rs 774 crores

BRLM: ICICI Securities, Edelweiss Financial Services, SBI Capital Markets

Company/Business

1. Are the company's earnings before tax more than Rs 50 cr in the past 12 months?

Yes. The company had profit before tax of Rs 119 crore as of March 2020.

2. Will the company be able to scale up its business?

Yes. The company is primarily in the stockbroking business (around 75 per cent of the FY20 revenue). With the advent of modern platforms (mobile apps, internet trading), brokers can scale up the business and reach newer clients by using the same platform, thereby reducing the need for any capex while catering to the growing number of clients. Moreover, factors like the flat fee-based model, a growing interest in the derivatives market, the use of technology, lower penetration of mutual funds and shares and debentures in household savings and customer acquisition through digital medium enable the company to scale up its business easily. Moreover, during Q1FY21, about 85 per cent of the client acquisition was done digitally. Use of the internet for client acquisition is highly scalable as compared to the person-to-person acquisition.

3. Does the company have a recognisable brand (s), which is truly valued by its customers?

No. Broking business has experienced disruption in the last few years. Upstart like Zerodha, with its no-fee on delivery model, now accounts for around 13 per cent of active clients on NSE. On the other hand, Angel Broking is the fourth biggest brand with a 5.3 per cent share. Low customer stickiness, coupled with rapid technological changes, has taken away the brand power of legacy companies.

4. Does the company have high repeat customer usage?

No. As of June 2020, the company had around 21.5 lakh operational broking accounts out of which, 38 per cent traded on exchanges in the preceding 12 months.

5. Does the company have a credible moat?

No. Ever since mobile and internet stock trading took off, the broking business has become commoditised. Companies mainly compete based on low trading fees. Additionally, a better user interface backed by technology has become more of a norm than the exception. Intense competition from newer players, undifferentiated revenue segments i.e. broking accounts for around 75 per cent of the FY20 revenue and the absence of any network effects as more people join the trading platform render the company without any credible moat.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No. Businesses related to capital markets are highly regulated since these markets are susceptible to manipulation and deal directly with public money. Broking business is subject to extensive supervision by various regulatory bodies, including SEBI. Earlier, a promoter group member was barred from accessing the capital market for two years on the charge of violating SEBI regulations.

7. Is the company's business immune from easy replication by new players?

No. Brokerages act as an intermediary between clients and exchanges and help in the smooth execution of trades. Since this business does not require complex technology and moderate capital, it can easily be replicated by newer players.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes. The company offers broking and advisory services through different digital platforms like mobile app and web. Although the company needs to consistently do technological up-gradation and provide add-on services like automated advisory, Robo advisory and others, the basic nature of trading services cannot be easily substituted or outdated.

9. Are the customers of the company devoid of significant bargaining power?

No. The broking industry has seen a business model shift towards a flat fee-based model. Angel Broking, for example, charges zero for delivery and a flat fee of Rs 20 per trade for other types of transactions. Commoditisation of services, coupled with intense competition from new players (Zerodha, 5paisa others), gives ample choices to customers to start their new broking account with some other brokerage company.

10. Are the suppliers of the company devoid of significant bargaining power?

No. The trading of equities, commodities and other product offerings of the company happen on different exchanges like BSE, NSE, MCX. These exchanges are few in number and are almost a monopoly in their respective financial products.

11. Is the level of competition the company faces relatively low?

No. The level of competition is intense in the brokerage business. For example, Zerodha had a negligible market share five years ago but today, it is the market leader (about 16 per cent share) in terms of active clients on NSE. Moreover, several other technology-based startups like Upstox, Groww, Paytm and others are targeting young clients who are getting first-time exposure to the markets.

Management

12. Does any of the company's founders still hold at least 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes. Post the IPO, the promoter group will own around 44.6 per cent stake in the company.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes. The promoter cum MD of the company has been associated with it since its inception. The CEO has been associated with the company since 2000, while the CFO joined in 2015.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes. There have been no major cases against the management. However, in 1999, one of the members of the promoter group was debarred from accessing capital markets for a period of two years on the charge of violating SEBI regulations. Since then, there have been no further charges of this nature against any promoter or promoter group member.

15. Is the company free of litigation in court or with the regulator that casts doubt on the intention of the management?

Yes. However, since the company deals directly with public money, it is involved in several cases that tune to roughly Rs 66 crore (including subsidiaries).

16. Is the company's accounting policy stable?

Yes. As per the auditor's report, the company's accounting policy has been stable.

17. Is the company free of promoter pledging of its shares?

Yes. None of the promoters' shares are pledged.

Financial

18. Did the company generate current and five-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

No. The last-year average ROE was around 14.5, while the return on capital employed was around 13.7.

19. Was the company's operating cash flow positive during the previous year and at least four out of the last five years?

No. Although the cash flow from operations was positive in March 2020, it was negative for three years out of the last five years. The volatility in cash flow from operations is on account of changes in payables to or receivables from the various exchanges (NSE, BSE, MCX).

20. Did the company increase its revenue by 10 per cent CAGR in the last five years?

Yes. The company managed to increase its revenue by around 10.3 per cent YoY during the last five years until March 2020.

21. Is the company's debt-to-equity ratio less than 1 or is its interest coverage ratio more than 2?

Yes. The company had an interest coverage ratio of around 8.9 as of March 2020, however, it had a debt-to-equity ratio of around 1.01 as on June 30, 2020.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes. Working capital requirements account for less than 1 per cent of sales.

23. Can the company run its business without relying on external funding in the next three years?

Yes. For business expansion, the company would mainly rely on outside factors like the performance of capital markets, penetration of mobile internet, macroeconomic conditions, amongst others. Since the company delivers its services through digital platforms, capex needs for business shouldn't be high.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

No. The company's short-term borrowings have been volatile in the past. It more than halved to around Rs 490 crore in March 2020 from Rs 1,115 crore in March 2018 but has again shot up to Rs 646 crore as of June 2020. Moreover, it remains high at around 1x of equity.

25. Is the company free from meaningful contingent liabilities?

No. Contingent liabilities accounted for around 40 per cent of the equity as of June 2020. A majority (88 per cent) of contingent liability was on account of bank guarantees with exchanges as margin/government authorities.

The Stock/Valuation

26. Does the stock offer operating earnings yield of more than 8 per cent on its enterprise value?

Yes. The company offers an operating earnings yield of around 14 per cent based upon post IPO enterprise value.

27. Is the stock's price-to-earnings less than its peers' median level?

No. The company does not have many peer group companies listed, however, valued at 30x March 2020 earnings, the stock is richly valued against comparable peers.

28. Is the stock's price-to-book value less than its peers' average level?

Yes. Although the company does not have many peer group companies listed, however, valued at 3.2x post IPO book value, the stock is moderately valued against comparable peers.

Disclosure: Author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()