Company / Business

In terms of expansion and growth, the company intends to increase the capacity of its Rajasthan plant to 17,021 TPA by December 2019 from the current 6,221 TPA. It is also planning a 51,943-TPA greenfield project in Telangana by using the proceeds from fresh issue. At present, it is coming out with a total IPO size of Rs 500 crore- Rs 250 fresh issue and Rs 250 crore offer for sale. It also raised Rs 106 crore in pre-IPO placement, at Rs 178 per share, from South Asia Growth Fund. While the promoters will use a substantial portion of proceeds from the offer to pay off the promoter-level debt, proceeds from the fresh issue and pre-IPO raise will be utilised for part debt repayment, greenfield expansion, upgrade existing plants and general corporate purpose.

Strengths

Superior Distribution network: The company has strengthened its distribution network from 766 distributors in March 2017 to 1,408 in October 2019. The network is spread across all parts of the country, with a major presence in North and South India.

Comprehensive product portfolio: The company is present across a range of plastic polymer pipes, including the high margin CPVC pipes. With a product portfolio of 7,167 stock keeping units (SKUs), the company can service varied applications in the fields of plumbing, irrigation and water management.

Technical collaboration: Prince Pipes has a technical collaboration with Wavin, a Netherland-based company. Wavin provides technical know-how in the product manufacturing. As a result of this collaboration, the company has seen a significant improvement in the production processes at two of its facilities.

Weakness

Low brand power: Although the company has been in the business for the last 30 years, its market share stands at around five per cent. The pipes and fitting industry is highly competitive, with the top player holding around 10 per cent of the market.

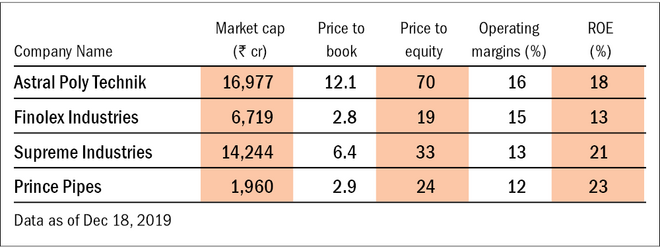

Presence in the low margin business: Around 71 per cent of FY19 sales came from UPVC pipes. This product comes under a low-margin segment. Although around 20 per cent of sales came from high-margin CPVC pipes, it will be difficult to scale up in that business owing to the presence of established players like Astral, Finolex and others.

Low pricing power: The fluctuation of raw material prices in accordance with crude oil prices, the presence of only a few suppliers and an intensive industry competition limit the pricing power of the company, thereby resulting in volatile operating margins. Despite having a larger reach and distribution it has not been able achieve a larger scale compared to Finolex or Astral Polytechnik.

Risks and Concerns:

The company faces substantial risk of fluctuation in the prices of raw material, as they are dependent on crude oil prices. Also, the promoters are required to repay Rs 192 crore against bonds issued by promoter-owned entity, Express Infra. Failure to repay this amount will create a 35 per cent pledge on their holding in the company (on a total diluted basis). The promoters intend to repay this amount by using proceeds from the offer for sale.

Total IPO size: Rs 500 crore

Fresh Issue: Rs 250 crore

Repayment of certain borrowings: Rs 48 crore

Funding of greenfield injection moulding plant at Telangana : Rs 184 crore

Upgrade existing Plants: 82 crore

Balance for general corporate purpose

Offer for Sale: Rs 250 crore

Promoters: Rs 250 crore

Additional details

Price Band: Rs 177-178

Subscription Dates - Dec 18, 2019 - Dec 20, 2019

ROE (FY 2019)- 23.2%

Revenue (FY 2019) - Rs 1,572 crore

Post-IPO, promoter holding- 65.8 per cent (including Promoter group)

Post IPO valuation- Rs 1,960 crore

Total debt (Pre IPO) - Rs 297 crore as of June 2019

Total debt (Post IPO)- Rs 249 crore

Equity (Post IPO) - Rs 678 crore

Net debt to equity (Post - IPO): 0.35 times

Company/Business:

1. Are the company's earnings before tax more than Rs 50 cr in the past twelve months?

Yes, the company's earnings before tax stood at Rs 111.5 crore in FY19.

2. Will the company be able to scale up its business?

Yes, the plastic pipes and fittings industry is expected to grow to Rs 500-550 Bn in 2024 from the current Rs 290-300 Bn, driven by several factors, including changing consumer preferences for plastic pipes and government-led schemes like 'Housing for All,' Nal se Jal and others. Around 60-65 per cent of the industry is organised and reforms like GST are expected to push this share upwards, thereby empowering the company to scale up its business.

3. Does the company have a recognisable brand (s), which is truly valued by its customers?

No. Although the company increased its ad and sales promotion expenses from 1.1 per cent in March 2016 to 2.7 per cent of its total revenue in March 2019, the low market share of five per cent in a highly competitive industry depicts low brand power. Moreover, the company's revenue growth of 13 per cent over the last three years is near 10-12 per cent of the industry growth.

4. Does the company have high repeat customer usage?

No. Since pipes and fittings have extended life cycles that go up to decades, the product replacement takes years.

5. Does the company have a credible moat?

No, although the company's distribution network increased from 766 in March 2017 to 1408 in October 2019 and it had six manufacturing facilities across the country, such competitive advantage has not translated into numbers. The inventory days increased to 52 days in March 2019 from 36 days in March 2016, depicting a low inventory churn. Besides, the company also has lower operating margins as compared to its prominent peers, which depicts mediocre operational efficiency.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, raw material costs account for 65-70 per cent of the operating income. The price of raw material is dependent on crude oil prices, which can be affected by regulatory or geopolitical risks. Besides, the company doesn't have any long-term supply contract for the raw material. The company is also prone to factors like depreciation of the rupee and import duties imposed.

7. Is the company's business immune from easy replication by new players?

No, around 71 per cent of the company's sales (FY19) were derived from the pipes made of unplasticised polyvinyl chloride (uPVC). This chemical compound requires low technical know-how and can be replicated by new players easily.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes, more than 70 per cent of sales come from irrigation and plumbing purposes under which, mainly UPVC and CPVC pipes are used. Not many substitutes are available for such sort of pipes.

9. Are the customers of the company devoid of significant bargaining power?

No, the company sells Prince piping products to distributors, who then resell the products to wholesalers, retailers, and plumbers. Whereas, its Trubore products are directly sold to wholesalers and retailers. The pipes and fitting industry is a highly competitive industry, with several players operating in it. Although the organised segment accounts for 60-65 per cent of the total industry, the top player accounts for around 10 per cent of the total industry. Customers have a range of options to choose from.

10. Are the suppliers of the company devoid of significant bargaining power?

No, the supply of key raw materials for the company is met through a mix of domestic procurement and imports. In India, the production is dominated by a few big players. Moreover, the price of raw material is dependent on crude oil prices.

11. Is the level of competition the company faces relatively low?

No, the pipes and fitting industry is highly competitive with almost 60-65 per cent of the market dominated by organised players. Also, the largest player in the industry is Supreme Industries Ltd, which commands a market share of around 11 per cent.

Management

12. Does any of the company's founders still hold at least a five per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, Post IPO, the promoters will hold around 65.8 per cent of the company.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes, Jayant Shamji Chheda, Chairman and Managing director, has been associated with the company since its inception.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, although promoters are required to repay Rs 192 crore against bond issued by a promoter-owned entity, Express Infra. Failure to repay this amount will create 35 per cent pledge on their holding in the company (on a total diluted basis) and provide for a non-disposal undertaking on 16 per cent equity shares. Also, another promoter group entity, Arena Enterprises, has Rs 146 crore loan from Standard Chartered Bank guaranteed by the promoters.

15. Is the company free of litigation in court or with the regulator that casts doubt on the intention of the management?

Yes. However, the promoters have a case filed against them involving the promoter group company and a claim of Rs 905 crore.

16. Is the company's accounting policy stable?

Yes, we have no information which suggests otherwise.

17. Is the company free of promoter pledging of its shares?

Yes. However as mentioned in Point 14, the failure to repay the outstanding bond amount may invoke 35 per cent pledge of promoter holding.

Financial

18. Did the company generate current and five-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

Yes, the company's last five-year average ROE and ROCE stood at 22.3 per cent and 19.0 per cent, respectively as of March 2019. While the current ROE and ROCE stood at xxx and xxxx as of xxxxx.

19. Was the company's operating cash flow-positive during the previous year and at least four out of the last five years?

Yes, the company had cash flow from operations of Rs 220 crore for FY19. Also, they were positive for all the last five years till March 2019.

20. Did the company increase its revenue by 10 per cent CAGR in the last five years?

No, the company's sales increased by just 7.7 per cent in the last five years ending March 2019.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest coverage ratio more than 2?

Yes, post IPO the company will have a net debt (Debt excluding cash) to equity of 0.35 times.

22. Is the company free from reliance on huge working capital for day to day affairs?

Yes, the company in the last few years has consistently been able to decrease its working capital requirements as a percentage of sales from 23 per cent in March 2016 to 15 per cent in March 2019. While at the same time it has also reduced its reliance on short term borrowings.

23. Can the company run its business without relying on external funding in the next three years?

Yes, though the company has planned to do a greenfield expansion in Telangana which will be entirely funded from IPO proceeds and will increase the capacity by 21 per cent. This step will provide the company with scope of expansion in future with minimal capital requirement. Moreover, in each of the last five years till March 2019 the company has generated positive free cash.

24. Have the company's short term borrowings remained stable or declined (not increased by greater than 15%)?

Yes, the short term borrowings have decreased from Rs 186 crore in March 2016 to Rs 146 crore in March 2019.

25. Is the company free from meaningful contingent liabilities?

No, the company has total contingent liabilities worth Rs 72 crore which form around 11 per cent of the total post IPO equity.

The Stock/Valuation

26. Does the stock offer operating earnings yield of more than 8 per cent on its enterprise value?

No, the operating earnings yield for the company stood at 6.6 per cent based upon at an upper price band of Rs 178 per share and FY19 net profit.

27. Is the stock's price to earnings less than its peers' median level?

Yes, the stock on the basis of post IPO basis is priced at 23.5 times its FY19 earnings, as compared to the median price to earnings of its peer group at 33 times.

28. Is the stock's price to book value less than its peers' average level?

Yes, the stock post IPO is reasonably priced at a price to book value of 2.9 times as per FY19 financials, compared to a median price to book of industry peers at 3.4 times.

Book running lead managers- JM Financial, Edelweiss.

* The lower the score you find here, the riskier the stock

Disclosure: Author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()