It has been a good six years since SEBI gave mutual fund investors an option to go direct and skip distributor services in mutual funds. So have you been wondering what difference direct plans, with their lower expense ratios, have made to investor returns? We took stock of the five-year returns on key categories of mutual funds to find out.

When looking at this data, it is important to bear in mind that the last few years have been exceptional, with equity SIPs generating returns that are quite low. Markets behave erratically, and even the best of investments can produce unremarkable returns in the short term. Despite this, the difference between the returns of direct and regular plans has still been around 1 per cent, which is not bad at all. Compounded over time, even this one percent is quite significant, making the decision to go for direct plans worthwhile. The table below captures the difference between the SIP returns of direct and regular plans over the last five years.

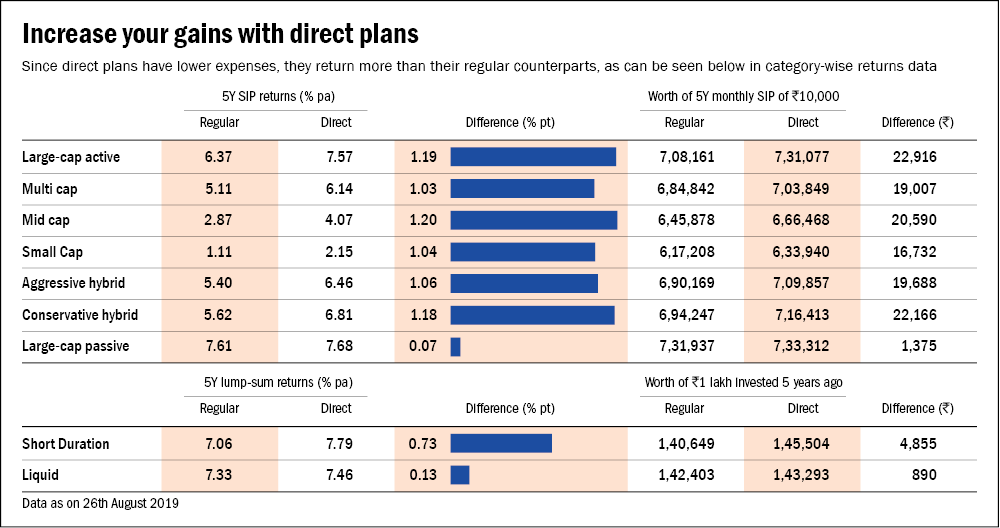

Equity funds

In the equity category, direct investing made the biggest difference to investors in actively managed large-cap funds. SIPs are the preferred mode of investing in equity funds. Comparing SIP returns on direct versus regular plans in actively managed large-cap funds, direct plans averaged an internal rate of return of 7.57 per cent over the last five years (as of August 26, 2019), making for a higher return of 1.19 per cent a year if you went direct.

SIPs in the multi-cap category have had a harder time getting to double digits in the last five years, given the recent correction in mid- and small-cap stocks. The difference in returns between the direct and regular plans in this category averaged 1.03 per cent.

However, the difference between direct and regular plans could be far higher or lower for individual schemes within a category. In multi-cap funds, for instance, in some schemes (such as Invesco Multicap for instance) investors earned 1.78 per cent more by going direct, but in others (such as UTI Equity) the difference was just 0.51 per cent. In the large-cap category, the direct plan of Motilal Oswal Focused 25 made 1.43 per cent more than its regular plans, the difference was just 0.74 per cent for DSP Top 100 Equity. The direct-regular differentials depend a lot on the quantum and structuring of distributor commissions by individual AMCs.

Surprisingly, direct-regular return differences were as high in hybrid category as they were in pure equity funds. SIPs in the direct plans of aggressive hybrid funds beat the regular plans by 1.06 per cent on an average. In conservative hybrid funds, the difference was 1.18 per cent.

Overall, the experience so far suggests that direct plans on an average can bump up investor returns by about 1 percentage point every year in the equity and hybrid categories, which can add up to quite a substantial sum in the long run.

In debt funds, where lump-sum investments are more common, we compared five-year CAGRs on direct versus regular plans. In liquid funds, direct plans earned 0.13 per cent more than regular plans, with their five-year CAGR at 7.46 per cent. In short-duration funds, the direct option earned 0.73 per cent more on an average than the regular option, with five-year returns at 7.79 per cent.

The right choice matters

While evaluating gains from going direct though, it is important to remember that selecting the right schemes makes a far bigger difference to your returns than the direct versus regular choice. This is exemplified by the wide divergence between the best and worst performers in each category. In multi-cap equity, for instance, selecting the top five performers over the last five years would have earned you an SIP return of 10.4-12.4 per cent, but if you were stuck with the bottom five funds you would have made just 2-4 per cent. Ditto with mid-cap funds, where the top five schemes got you to an SIP return of 7-10 per cent, while the bottom five ranged from -1.5 to 0.5. Hence, your decision to go direct should not be based only on saving one per cent in costs each year. The decision needs to be based on your ability to choose good performers (they need not be category toppers) within each category on your own. In the long run, owning the wrong funds can cause far more damage to your returns than you can save by going direct.

Ask Value Research ![]()