The term 'ELSS' stands for Equity-Linked Savings Scheme. The terminology may be old-fashioned but the idea is very straightforward. Mutual fund companies in India operate a set of mutual funds that qualify as ELSS funds as defined by the government. When you invest in these funds, your investment amount can be deducted from your taxable income. This lowers the amount of tax you need to pay.

While there is no limit on the amount you can invest in ELSS funds, the tax exempted amount is capped at Rs 1.5 lakh in a financial year. Effectively, this means that if you are in the highest tax bracket, then you will pay Rs 46,800 less tax than you would otherwise have done. Keep in mind though that this Rs 1.5 lakh limit is not limited to ELSS funds alone, but is the combined limit under Section 80C of the Income Tax Act. There are a number of other investments that are clubbed under Section 80C, including EPF (Employees Provident Fund) and PPF (Public Provident Fund). So before investing in ELSS, take into consideration what other 80C investments you have already made so that you don't unnecessarily exceed the limit.

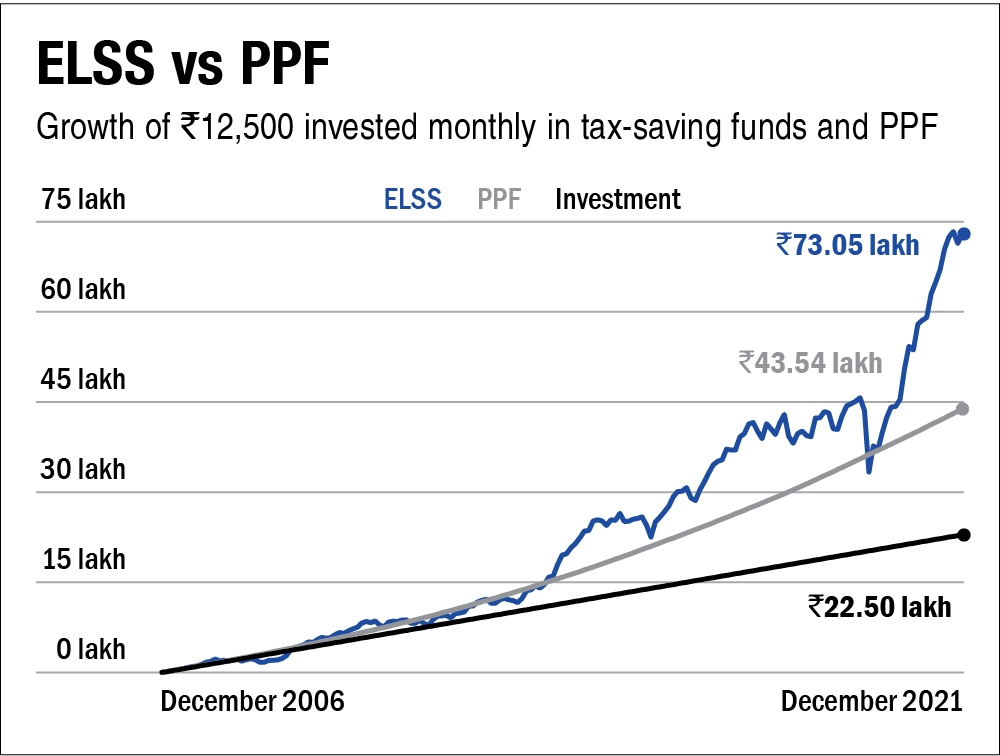

ELSS funds are uniquely advantageous compared to the other tax saving investments available to you. There are two reasons for this. The first is that ELSS funds are unique in being the only viable tax-saving investment within this Rs 1.5 lakh limit that brings the benefits of equity returns. Sure, there are two other options that give equity-linked returns - Unit Linked Insurance Plans (ULIPS) and the National Pension System (NPS). However, ULIPs have a lock-in of at least five years coupled with high costs and poor transparency. The NPS for its part is a great product but it's a retirement solution rather than a savings one. It has only partial exposure to equity in addition to a very long lock-in period that effectively extends till retirement age. In contrast, ELSS funds have the best combination of a much lower cost than ULIPs, 100 per cent equity, and a reasonable lock-in period of just three years.

Besides this, ELSS funds have another hidden benefit. It makes for an excellent gateway product for beginner investors, giving them their first taste of equity investing and of mutual funds. You end up investing in these funds because the tax-savings attracts you and it has the shortest lock-in. However, the three year lock-in ensures (most of the time) that investors get good returns even if their timing and choice of funds is less than optimal. This experience converts a certain proportion of these investors to lifelong investors in equity mutual funds over and above their tax-saving needs. Once you have a taste of long-term equity returns, then you feel inclined to giving other types of equity investments a go as well.

However, to choose ELSS funds, one should plan ahead and not wake up to tax-saving investments late in the year. For a variety of reasons, savers tend to make hasty and poor decisions while choosing their tax-saving investments. For one, many of those who wait till the end of the year are those who don't make any discretionary investments other than tax-savings. They are inexperienced in this whole activity and emerge to invest only once a year, generally to fall prey to the first salesman who comes along. As long as an investment saves tax, they feel that the immediate job is done.

However, this approach is a waste of money. A good tax-saving investment must be an investment first and a tax-saver later. For most people the investment that would make the most sense is in an ELSS fund. This is because salary earners generally already have some of the permitted amount going into fixed income through PF deductions and to balance that, equity is best.

This article was originally published on July 30, 2021.

Ask Value Research ![]()