The IPO season has picked up in Dalal street, once again. Following the successful listing of Chalet Hotels and the recent closing of Metropolis Healthcare, the latest entrant to the party is Polycab Wires & Cables. Incorporated in 1996, this Mumbai-based company is involved in manufacturing and selling cables & wires and fast-moving electronic goods (FMEG), comprising electric fans, LED lightings and luminaries and switch gears, under the brand name 'POLYCAB'. In the country's Rs 52,500-crore cables and wires industry, the company has already made a name for itself, with a market share of 12%.

At present, POLYCAB has 24 manufacturing facilities located across three states and one union territory. It enjoys a pan-India presence on the back of a network of 2,800 authorised dealers, who enable the company to reach out to almost 100,000 retail outlets. In addition to having an installed capacity of 35 lac km for cable and wire production, the company entered into a tie-up with Techno in 2017 to manufacture LED lighting products. In 2016, it formed a 50:50 partnership with Trafigura, a commodity trading company, to set up a production facility of copper wire rods in Gujarat.

At present, POLYCAB has 24 manufacturing facilities located across three states and one union territory. It enjoys a pan-India presence on the back of a network of 2,800 authorised dealers, who enable the company to reach out to almost 100,000 retail outlets. In addition to having an installed capacity of 35 lac km for cable and wire production, the company entered into a tie-up with Techno in 2017 to manufacture LED lighting products. In 2016, it formed a 50:50 partnership with Trafigura, a commodity trading company, to set up a production facility of copper wire rods in Gujarat.

In 2009, the company undertook an EPC in power distribution and rural electrification. However, this business is no longer its focus area because of unstable margins. In FY18, its cable and wires business accounted for around 89 per cent of the total revenue, while its growth-driver, FMEG segment, contributed around 7 per cent.

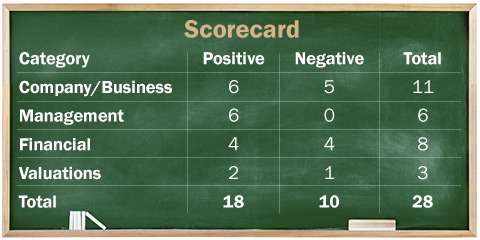

Strengths

- Superior dealer network: With a pan India dealer network of 2,800 dealers and 20 warehouses, the company is able to sell its products in 100,000 retail outlets. It helps POLYCAB maintain its dominant market share in the cable and wires industry and cross-sell FMEG products.

- Backward integration: The company is moving ahead with a backward integration by doing a 50:50 tie-up with Trafigura to set up a 225,000-MT manufacturing facility with the intent to produce copper wire rods. As revealed by its management (source: Wire & Cable India), this plant would exceed the company's requirement for copper and leave around 1,00,000 MT/year rods available for the rest of the market.

- Brand recognition: As a well-known cable and wires brand, POLYCAB has maintained its brand name over the years. Recently, it has roped in famous actor Paresh Rawal to promote its energy and money-saving green cable & wires and other products through an innovative ad campaign. The ad is being telecast during Indian Premier League matches.

Weakness

- High dependence on key raw materials: The company's realisation and profitability in the cable and wires business are highly dependent on copper and aluminium commodity prices, which together account for roughly 75 per cent of its total raw material costs and are denominated in dollars.

- High working capital requirements: The company is reliant on short-term borrowings to run its operations smoothly. As of FY18, the working capital requirement as a percentage of sales stood at 16 per cent, which was quite high and could lead to negative impacts.

- Concentrated suppliers: The company procures almost 50 per cent of its raw material costs from the top four suppliers. So, any disruption at the suppliers' end can affect the company adversely.

Risks and Concerns

The company is at substantial risk of price fluctuations, as its key raw materials like copper, aluminium and PVC are denominated in US dollars. Since its cable and wire division contributes roughly 87 per cent to its total revenue, any disruption in this business segment can adversely affect the company's financials. POLYCAB has entered into two strategic partnerships to produce LED lightings and manufacture copper wire rods. So, if any of these partnership comes under strain, it will leave a negative impact on the business.

Total IPO size: Rs 1,337-1,346 crore

Fresh Issue: Rs 400 crore

Repayment of certain borrowings: Rs 80 crore

Funding incremental working capital requirement: Rs 240 crore

General corporate purpose: Rs 80 crore

Offer for Sale: Rs 946 crore

IFC: Rs 380 crore

Promoters: Rs 504 crore

Additional details

Price Band: Rs 533-538

Subscription Dates: 5-9 April

ROE (FY 2018): 17.2 %

Revenue (FY 2018): Rs 6,779 crore

Post-IPO, promoter holding: 68.7 per cent (including Promoter group)

Post IPO valuation: Rs 7,926-7,997 crore

Total debt (Pre IPO): Rs 800 crore as of FY18

Total debt (Post IPO): Rs 540 crore

Equity (Post IPO): Rs 3,129 crore

Net debt to equity (Post - IPO): 0.17 times

Company / Business

1. Are the company's earnings before tax more than Rs 50 cr in the past twelve months?

Yes, the company's profit before tax for FY18 was Rs 576.5 Crore.

2. Will the company be able to scale up its business?

Yes, the environment is favourable for the company. The government's continued focus and investments in power & infrastructure and rural electrification, a revival of the housing sector on the back of the 'Housing for All' initiative, growing popularity of energy-efficient products and higher discretionary income have ultimately paved the way for the company to scale up its business. Also, most of the manufacturing facilities are currently operating at less than 80 per cent utilization, leaving them with the opportunity to scale up.

3. Does the company have a recognisable brand (s), which is truly valued by its customers?

Yes, the company has a dominant market share of almost 12 per cent of the cables and wires industry. It is mainly a fragmented industry, with the organised players accounting for roughly 66 per cent of the total market. To increase its brand recognition, the company roped in ace actor Paresh Rawal for promoting the brand. Further, it has been a sponsor for the Indian Premier league since 2017.

4. Does the company have high repeat customer usage?

No, the nature of its products, comprising cables, wires, LED lighting and Electric fans, is such that their life cycle is long and hence, it takes years to replace these products.

5. Does the company have a credible moat?

Yes, the company has a pan-India presence through a strong dealership network and the largest market share in the cable and wires industry. It serves key institutional and government clients, including L&T Construction and Konkan Railways.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the company is dependent on the supply of raw materials like copper, aluminium and PVC, which are denominated in foreign currency and form a huge part, around 90 per cent, of the total cost of its raw materials. Hence, the company is prone to external currency shocks because of global uncertainties. The company is also exposed to regulatory changes related to the safety and quality of its products.

7. Is the business of the company immune from easy replication by new players?

No. The modest capital requirement for setting up a manufacturing facility, low technical expertise and the option of outsourcing manufacturing to third parties can lead to an easy replication of its business by new players.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes, the company's main products are cable and wires, which are basically utility products and relatively resistant to technological disruptions.

9. Are the customers of the company devoid of significant bargaining power?

Yes, the company categorises its customers as dealers, distributors and direct customers who belong to a diverse range of industries. For FY18, none of its customers contributed more than 5 per cent to the company's total revenue.

10. Are the suppliers of the company devoid of significant bargaining power?

No, the company is a price taker as it relies on its suppliers for key raw materials like copper, aluminium, PVC and steel. Further, its top four suppliers account for around 50 per cent of the total raw material costs. However, the company is all set to start manufacturing copper wire rod, which is likely to strengthen its position in the coming time

11. Is the level of competition the company faces relatively low?

No, as the cable and wire industry is a fragmented industry with an unorganised market share of 12. Its newly incorporated FMEG business (7 per cent of the total revenues) also faces stiff competition from both domestic and foreign players.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters hold more than 25 per cent stake in the company?

Yes, the promoter holding post IPO will be more than 50 per cent. Also, each of the four promoters will hold more than 5 per cent post IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes, Promoter and Managing Director of the company, Inder Jaisinghani, has been associated with the company since its inception. Chief executive officer, Ramakrishnan, joined the company in 2012, while Chief Financial Officer, Shyam Lal Bajaj, joined the company in 2016 as a full-time director and became the CFO in 2018.

14. Is the management trustworthy? Is it transparent in its disclosures in line with Sebi guidelines?

Yes. However, the company is currently facing action from the RBI, as it made remittance amounting to Euro 478,276 to its subsidiary Poly cab Italy from 2012 to 2016. Consequently, these loans were written off from the financials of Poly cab Italy. The matter is currently pending as the company seeks RBI directions for the treatment of this remittance on the company's financials.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

Yes. However, the company is facing a case filed by Sam Business Continuity Services over non-payment of consultancy fees amounting to Rs 4.8 crore, along with 18 per cent interest per annum.

16. Is the company's accounting policy stable?

Yes. However, the auditor gave a qualified opinion for FY17 related to deficiency in the internal controls of revenue recognition by the company.

17. Is the company free of promoter pledging of its shares?

Yes, none of the promoter shares was pledged as of FY18.

Financial

18. Did the company generate the current and five-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

No, the company's five-year average return on equity and return on capital stood at 11.3 per cent and 16.9 per cent, respectively. As of FY18, return on equity stood at 17.2 per cent and the return on capital stood at 22.3 per cent.

19. Was the company's operating cash flow positive during the previous year and at least four out of the last five years?

Yes, the company reported positive cash flow from operations in each of the past five years.

20. Did the company increase its revenue by 10 per cent CAGR in the last four years?

Yes, the company was able to increase its net sales by 14 per cent CAGR in the last four years.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest coverage ratio more than 2?

Yes, the company's pre-IPO net debt to equity stood at 0.3 times as of FY18 and has been less than 1 in the last five years. Post IPO, the net debt to equity is expected to reduce to 0.17 times, as the company will pay off certain borrowings from the IPO proceeds.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

No, the company operates in a highly working capital intensive industry. However, as a percentage of sales, the working capital requirement has remained stable in the past five years.

23. Can the company run its business without relying on external funding in the next three years?

No, the company is in constant need of short-term borrowings to finance its working capital requirements. A substantial part of the current IPO proceeds will also be utilised for financing working capital requirements.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15%)?

Yes, although the company's short-term borrowings are high, they have remained stable as a percentage of revenue in the last five years.

25. Is the company free from meaningful contingent liabilities?

No, the company has contingent liabilities of almost Rs 703 crore, which accounts for 26 per cent of the total net worth as of December'18.

Valuation

26. Does the stock offer operating earnings yield of more than 8 per cent on its enterprise value?

No, post IPO, the stock offers an earnings yield at almost 7.8 per cent.

27. Is the stock's price to earnings less than its peers' median level?

Yes, post IPO the stock will be priced attractively at 21 times its FY18 earnings, as compared to the median price to earnings of its peer group at 53 times.

28. Is the stock's price to book value less than its peers' average level?

Yes, the stock post IPO is reasonably priced at a price to book value of 2.5 times as per FY18 financials as compared to a median price to book of industry peers at 9.4 times.

The book running lead managers- Kotak Investment Banking, Axis Capital, Citi, Edelweiss, IIFL and Yes Securities.

* The lower the score you find here, the riskier the stock

Disclosure: Author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()