Income seekers usually prefer the dividend option of debt-oriented funds as it gives them the psychological comfort of getting an 'income' without eating into the capital. However, this comfort comes at the cost of a higher tax outgo, thereby reducing the very income they are seeking.

The table below mentions the tax treatment of your investments in debt-oriented funds. As you can see, while you don't have to pay any tax on the dividend income, what you receive in the form of dividends is already after deducting the dividend distribution tax (DDT). Including the cess and surcharge, this tax aggregates to a hefty 29.12 per cent of the dividend declared. This works out to be much more than the capital gains tax you pay in case of a growth option, even at the highest tax bracket of 30 per cent. Let's understand this with an illustration.

Taxation of debt-oriented mutual funds

| Capital Gains | ||

| Dividend income | Short term (Up to 3 yrs) | Long term (More than 3 yrs) |

| Dividend distribution tax of 25% (plus surcharge and cess) to be deducted and paid by the AMC | Gains are taxed at 5%, 10% or 20% (plus surcharge and cess as applicable), depending upon which slab the investor falls in | Gains are taxed at 20% after providing the indexation benefit |

Dividend vs Growth

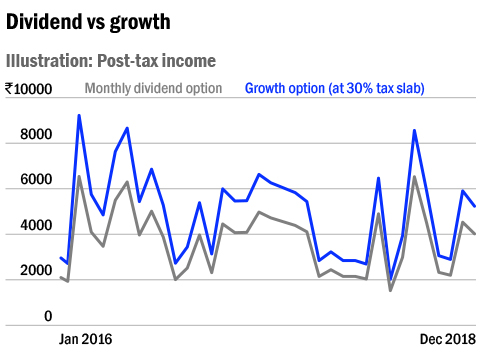

Suppose you invest Rs 10 lakh each in the monthly dividend and growth options of ICICI Prudential Regular Savings Fund at the start of 2016. This fund has a regular dividend paying history in the last three years and therefore lends itself well for this example.

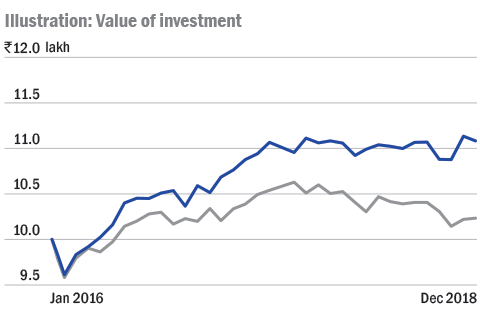

For the growth option, you create a monthly income stream by redeeming exactly the same amount as the gross dividend declared under the monthly dividend option. This basically means that their pre-tax monthly payouts are exactly similar. As the first chart shows, the growth option provides higher post-tax payouts even at the highest tax slab of 30 per cent. That's because in the growth option, tax is applicable only on the gains and not the entire redemption proceeds. On the other hand, in the dividend option, DDT is applicable on the entire dividend amount. Not only that, the value of investment is also higher in the growth option (see the second chart and table - Value of Investment).

| Monthly | Dividend option | Growth option |

| Amount invested at the start of 2016 | Rs 10 lakh | Rs 10 lakh |

| Pre-tax income (2016-2018) | Rs 1.8 lakh | Rs 1.8 lakh |

| Post-tax income (2016-2018) | Rs 1.3 lakh | Rs 1.7 lakh* |

| Fund value at the end of 2018 | Rs 10.2 lakh | Rs 11.1 lakh |

| *Assuming a 30% tax bracket | ||

Even a regular income seeker should invest in the growth option and periodically withdraw a part of his investment to derive income. This can be put on auto-pilot with a systematic withdrawal plan (SWP). But before you rush to exit from the dividend option of your funds, do consider the exit-load implications and time your redemption to avoid any extra costs.

Ask Value Research ![]()