Tata Coffee is the subsidiary of Tata Global Beverages, formerly Tata Tea, is a Tata group company which is into tea and coffee plantation. It is also one of the largest integrated coffee player in the world. Located in Karnataka and Tamil Nadu, the company gains from the suitable climatic conditions in South India, which is favourable for coffee cultivation and makes India the 5th largest coffee producer in the world after Brazil, Vietnam, Colombia and Indonesia.

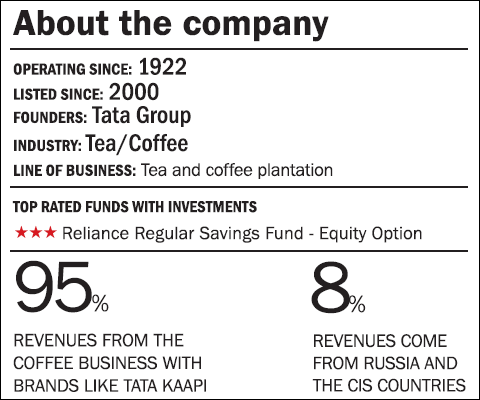

Tata Coffee was founded in 1922 and produces green coffee, instant coffee in both Robust and Arabic form, Tea, Cardamom, Pepper and Palm Oil. The coffee business contributes 95 per cent of the revenues with brands like Tata Kaapi, Tata Cafe, Mr. Bean in India and Eight O'Clock Coffee in the US. More than 60 per cent of Tata Coffee's revenues come from the US markets. It makes 8 per cent from Russia and CIS countries, and the Indian business accounts for 17 per cent as per the FY14 annual report.

Strength

Tata Coffee owns 19 coffee estates spread over 18,244 acres and its tea and other spices' estates spreads over 7,203 acres. Both these make Tata Coffee one of the largest integrated coffee plantation company in the world, and gives it an added margin over other players.

The company has grown its instant coffee business in the last few years despite the recent fall in the overall productivity due to adverse weather. It produced 6,955 MT in the FY14 as compared to 6,639 MT over the previous year.

Tata Coffee has capitalised on the heavy coffee drinkers in the US market ever since it acquired the popular Eight O'Clock brand in 2006, which now contributes heavily to the consolidated revenues of Tata Coffee. Eight O'Clock is the third largest seller of whole bean coffee in the US, which has a positive review in the market.

In recent times, Starbucks which made its India venture has an alliance with the Tata group and has entered into an agreement with Tata Coffee to source its coffee beans. This new alliance gives the company the necessary visibility in the wholesale market and acts as a strong selling point.

Growth Drivers

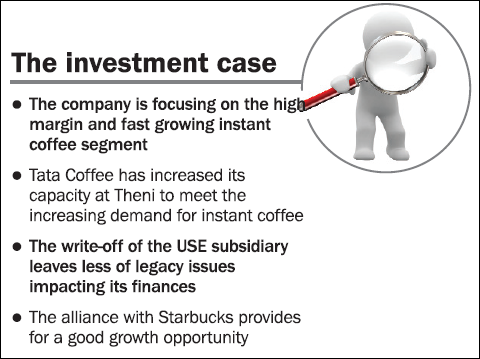

Tata Coffee has started focusing on the high margin and fast growing instant coffee segment. The company is also adding to its existing capacities and focusing on new geographies, especially in the region around Russia and the CIS. The new market will help the company to further push up its volume growth to overcome stagnant demand from Russia. To be geared to meet the increase in demand, the company has completed its Theni unit (in Tamil Nadu) in FY14 in with a capacity of 2,640 MT per annum adding to the existing capacity of 1,650 MT.

The agreement with Starbucks will work as an additional growth driver, as Tata Coffee will exclusively supply roasted coffee to them. Starbucks has been a recent entrant into the Indian market and is likely to expand its Indian footprint. Tata Coffee will be able to ride on the Starbucks growth, which will be setting up its outlets across India. Being the exclusive supplier to Starbucks, Tata Coffee will also grow, for which it has commissioned a coffee roasting facility at Kushalnagar.

The company will also be able to muscle up its capabilities in the long run from this alliance in terms of technology and process know-how. Moreover, this alliance is not limited to the Indian outlets but also extends to new locations overseas. This Starbucks alliance is favourable for Tata Coffee, which has to meet the rising demand from this global coffee chain.

Coffee plantation follows a biennial cycle. What this means is that there are alternate good and bad years. The company faced low productivity in FY13, which was an off year in the cycle, which however, got extended to FY14 as well due to insufficient and untimely rain. The outcome of the low production also resulted in subdued growth in its revenue. This is however, a short term issue. The company should be able to get back on track with good monsoons as it faces a rise in demand for its coffee.

Concerns

FY14 was bad for Tata Coffee in terms of productivity and its overseas operations. Productivity was down because of unfavourable weather conditions, which dragged down the profitability for the company. In FY15, the company expects to do better, however, any prolonged conditions or untimely rains can only be harmful to impact productivity and bring down the margins significantly.

Next, the company' US subsidiary, Consolidated Coffee Inc. faced problems, and despite revival plans and investments it failed. In FY14 the company had to sell this subsidiary and write-off losses in its books. The company has lost hope on the revival, which means it will be hesitant to re-enter the US market and tap the opportunity.

Tata Global Beverages, the promoter company has pledged 29 per cent of its holdings since March 2014. This, however, is not that alarming as the financial strength of Tata Coffee and the parent company are pretty intact.

Financials

Revenues have grown at a dismal rate of 9 per cent CAGR in the last 5 years and the net profit was 20 per cent over the same period. The return on net capital has taken a hit at 11 per cent in FY14 from the 5-year average of 16 per cent. The company had debt of ₹972 crore as on March 31, 2014, with a debt to equity ratio of 1.41. This again is not worrisome because for a capital intensive sector it is much under control.

Valuations

The company stock has been penalised for the fall in its profitability margin due to low productivity and the failure of its US subsidiary. As the markets touch new highs, the Tata Coffee has posted a meagre 2 per cent returns in the last year. We think, productivity is a temporary issue and with losses already written-off, the worst is already behind us. Given the land reserves, brand and future prospects we feel the stock is undervalued. It is strong long term buy.

This article was originally published on November 12, 2014.

Ask Value Research ![]()