Nitin Yadav/AI-Generated Image

Nitin Yadav/AI-Generated Image

Summary: When you invest in active mutual funds, you are also betting on the fund manager. The challenge is that this risk is real but often invisible until outcomes change.

When you invest in an actively managed mutual fund, you are making two bets simultaneously. The first is on the market. The second, less visible and rarely discussed, is on a person.

That person is the fund manager. Unlike market risk, which investors knowingly accept as the price of equity investing, manager risk arrives without warning. Most investors do not realise they are carrying it until something changes, and the fund they thought they owned turns out to be something else entirely.

Performance track records are presented as though they belong to a fund, but they actually belong to the one who ran it. Change that individual, and you may be holding an entirely different investment wearing the same name. Passive investing removes this problem. But to understand how, you first need to see what manager risk actually costs

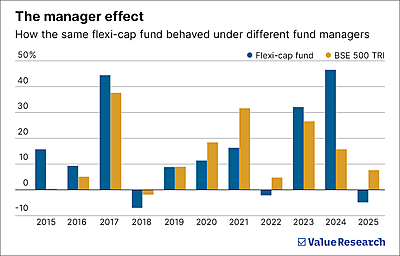

When the manager changes, so does everything

A flexi-cap fund from 2015 to 2017 delivered consistent returns, outpacing the broader market index by a meaningful margin. Investors who entered during that period had reason to feel confident. The fund had built a reputation; the numbers made the case.

In April 2019, the manager changed and what followed was three years of disappointment. From 2019 through 2022, the fund repeatedly trailed its benchmark. Investors who had bought in on the strength of the earlier record now held an underperformer. Not because the market failed them, but because the person calling the shots changed.

Then came another managerial transition in mid-2022, along with a sharp shift in investment strategy. The fund bounced back strongly, outperforming in 2023 and 2024. But the recovery was volatile. By 2025, it had slipped sharply again.

Over a decade, the same fund cycled through outperformance, prolonged underperformance and a volatile revival, with each arc depending on who was driving it.

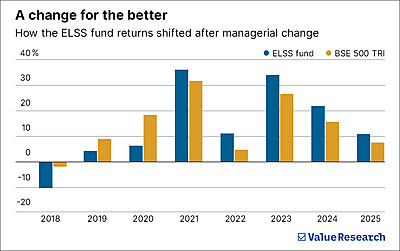

A good outcome is not a known one

A second example is sharper. This is about a tax-saving equity fund, which, by category design, comes with a mandatory three-year lock-in. Between 2018 and 2020, this fund consistently underperformed the benchmark. For investors locked in by regulation, there was no escape route. They could only sit and watch. In January 2021, a new manager took charge. Since then, the fund has done markedly better, outpacing the benchmark with consistency.

For investors who were locked in during the difficult years, the managerial change worked in their favour. But that is not a conclusion you can bank on in advance. A new manager might rescue a struggling fund, as in this case. Or they might inherit a strong one and erode what made it work. History offers both outcomes in equal measure and that uncertainty is precisely the problem.

The unquantifiable risk

This is the uncomfortable truth at the heart of active investing: manager risk exists and yet cannot be quantified. You can measure market volatility. You can model drawdown scenarios. But you cannot assign a probability to the event of your fund manager leaving, changing strategy, or simply losing their edge. And you certainly cannot model how damaging the next manager might turn out to be.

What you can do is monitor. Track managerial changes. Reassess the portfolio when leadership shifts. Evaluate whether the investment philosophy that attracted you in the first place still governs the fund. This is not impossible, but it is effortful and most investors, busy with their daily lives, simply can’t do it consistently enough.

The active investing mandate in effect asks investors to do more than just pick a good fund once. It asks them to watch that fund indefinitely, alert to changes they may not always hear about in time.

The problem that passive investing eliminates

Index funds and ETFs (exchange-traded funds) settle this problem cleanly. The investment process is rule-based. The portfolio mirrors a market index; it changes only when the index changes. The fund manager’s job becomes operational, maintaining efficient tracking rather than deciding what to buy or sell based on personal judgment.

This removes the manager variable entirely. The fund that tracks the Nifty 50 today will follow the same rules five years from now, regardless of who signs off on the trades. No star managers to track. No strategy drift. No personnel announcements to watch for. Passive funds do not promise outperformance. Skilled active managers do beat the market, some for extended periods. But what passive investing offers in place of that possibility is something arguably more valuable for long-term investors: certainty of approach. You know what you own, why you own it, and that it will not change into something different.

Active funds can deliver. But their delivery depends on people. And people leave, change course, underperform, or simply stop being as good as they once were.

Passive investing removes that dependency. It replaces judgment with structure. And for investors who would rather own the market than bet on the person navigating it, that trade-off is not a consolation prize. That is the point.

This article was originally published on April 01, 2026.

Ask Value Research ![]()