A forty-five-year-old homemaker in Pune ordered a Biba dress online. Seventeen hundred rupees. Cash-on-delivery.

The next day, a man called. Company employee, he said. Your address is showing as Nashik. Can’t deliver. He sent a QR code for online payment. She paid.

Fifteen minutes later, he called again. Wrong amount. Should have been seventeen hundred and fifty. She paid again. Then another call. Another account. Then another.

Between December 25 and 26, 2025, she made ten UPI transactions. Total: Rs 6,82,000. Five transactions exceeded Rs 90,000 each. When the caller asked for an additional two lakh, she told her husband. He recognised the scam immediately.

People laugh when they hear this. Or shake their heads. How could someone be so naive?

Ask a different question, and the laughter dies. Why had this woman never handled a UPI transaction before? Why didn’t she know what a QR code does? Why did she have a bank account with lakhs in it but no understanding of how digital money works?

She didn’t lack intelligence. She lacked literacy. Not the ability to read words. The ability to read financial systems.

The problem with ‘financial literacy’

The phrase “financial literacy” gets used so often that it’s become meaningless.

Governments run campaigns. Banks hold workshops. AMCs sponsor events. After years of this, only 21 per cent of Indian women can answer basic financial questions correctly.

Here’s why: most financial literacy is taught as abstract concepts. What is compound interest? What is inflation? What is diversification? These are fine questions for an economics textbook. They are useless when an insurance agent tells you a ULIP gives “insurance plus investment plus tax benefit.”

They are useless when your mutual fund statement shows a negative return, and you don’t know whether to panic. They are useless when someone sends a QR code, and you can’t tell sending or requesting.

What women need is not literacy. It’s fluency. The ability to read a mutual fund fact sheet. To look at an insurance policy and understand what’s covered. To hear an advisor’s recommendation and ask: why this fund? What’s your commission? Show me the alternatives.

The industry’s own jargon problem

Let’s be honest about something. A big part of the “confidence gap” in investing is manufactured.

NAV. AUM. Expense ratio. CAGR. XIRR. Alpha. Beta. Sharpe ratio. Large-cap, mid-cap, flexi-cap, multi-cap, ELSS, ETF, STP, SWP. You encounter more acronyms on a mutual fund website in five minutes than most people use in a year.

Jargon creates a priesthood. A class of people who “understand” finance. And everyone else who doesn’t.

But consider this. The women of SEWA — 93 per cent illiterate, 97 per cent living in slums — built a bank with a 96 per cent repayment rate. Manipur’s Ima Keithel vendors have operated a credit system for 500 years. Stalls passed mother to daughter. These women didn’t know what CAGR means. They knew how their money worked. Because they had access and practice.

The confidence gap is not a character flaw in women. It is a design flaw in the system.

The digital shift

Something remarkable happened in five years. Fifty-five per cent of women investors now use fintech platforms. Up from 14 per cent. That’s not a trend. That’s a revolution.

Why? Digital platforms did what traditional finance never bothered to. They made the first step easy. No bank manager appointment. No form-filling in triplicate. No advisor talking over you. Just a screen, a few taps, and you’re in.

But digital access without digital literacy is dangerous. The Pune homemaker proves it. The phone was new. The vulnerability was ancient. Giving someone a UPI app without teaching them what a QR code does is giving someone a car without teaching them to brake.

From literacy to fluency

Forget definitions. Here’s what financial fluency looks like in practice.

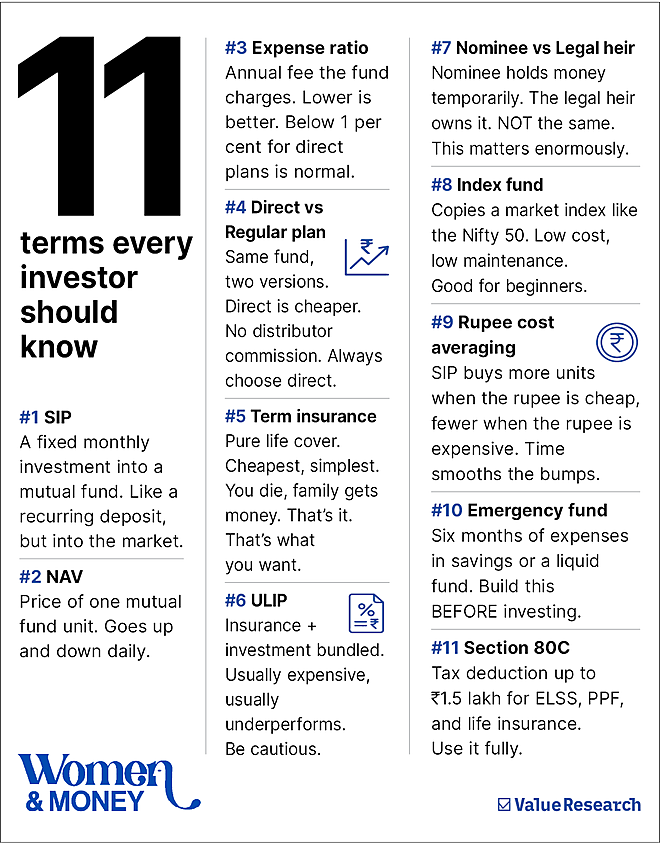

It’s knowing that when your insurance agent says, “you’ll get everything back at the end,” the policy has a maturity benefit. And that this almost certainly means an expensive product, poor returns. Better: a simple term plan plus a mutual fund.

It’s knowing that the “nominee” on your husband’s investment is not the legal heir. If he hasn’t written a will, the nominee holds money in trust, not in ownership.

It’s knowing that an expense ratio of 2.25 per cent is too high. Direct plans of the same fund are cheaper.

It’s knowing that when a stock tip arrives on WhatsApp, the sender has already bought.

None of this requires a finance degree. All of it requires someone to explain it once, clearly, without condescension.

The Chettinad women of Tamil Nadu managed enormous family wealth for generations. The Aachi — the matriarch — controlled the household treasury while her husband traded across Southeast Asia. This community founded the Indian Overseas Bank, the Indian Bank, and the Bank of Madura. These women didn’t attend a workshop. They managed real money in real time. The confidence came from the competence.

Financial fluency isn’t a certificate. It’s a muscle. You build it by reading one statement. Asking one question. Making one decision at a time.

Start with one term from that list. Learn it today. Use it this week. That’s not literacy. That’s fluency.

Her Money, Her Future • A 5-part Women’s Day special by Value Research

Next: Investing with confidence in a ‘male domain’

Ruchira Sharma, Senior Editor, Narrative & Long-form | Value Research

She writes about money the way it actually lives in Indian families, tangled with culture, silence, gold, and love. At Value Research, she anchors Investors' Hangout and Fund Manager Interviews, narrates Dhirendra Kumar's First Page, and leads the audio-visual team. Her Money, Her Future brings together her two crafts: the journalist's instinct for the untold story and the financial editor's demand for evidence in every sentence. Previously, 14 years at India Today: scripting, production, and long-form storytelling.

This article was originally published on March 06, 2026.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()