Aditya Roy/AI-Generated Image

Aditya Roy/AI-Generated Image

Summary: ETFs may be low cost, but buying them at a premium to NAV can quietly cut your returns. While most domestic ETFs rarely see large price gaps, international ETFs frequently trade at significant premiums or discounts. Checking iNAV and using limit orders can help protect your gains.

It is safe to say that passive investors have found their favourite investing vehicle. Nearly 78 per cent of passive equity AUM now sits in exchange-traded funds or ETFs, with index funds holding the rest. Within ETFs, large-cap funds dominate, accounting for roughly Rs 6.6 lakh crore in assets. The appeal is obvious: ETFs are low cost, transparent and easy to trade.

But there is one cost that does not show up on fact sheets and is often overlooked: the risk of buying ETFs at a premium.

Unlike the expense ratio, this cost is invisible. To see how it creeps in, we need to look at how ETFs are priced in the market. And that in turn depends on one crucial factor: liquidity.

Some ETFs are harder to buy and sell

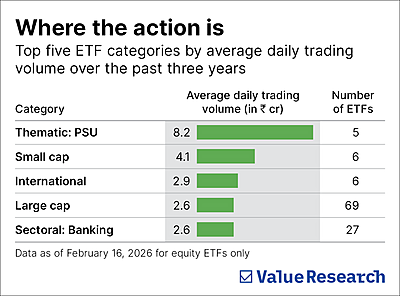

ETFs may dominate passive assets, but trading activity is far from evenly distributed. Some categories see steady buying and selling every day. Others barely trade. The table ‘Where the action is’ shows the five most actively traded ETF categories over the past three years.

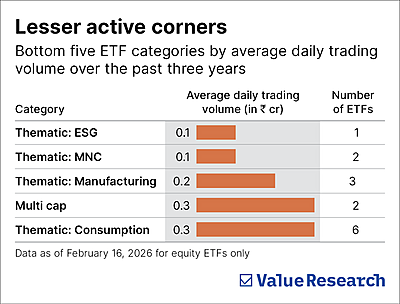

At the other end are quieter corners of the market. And four of the five least active categories are interestingly thematic (see the table ‘Lesser active corners’). They also have fewer ETFs. Thus, they are small, specialised pockets of the market with limited trading interest.

Why does this matter? Because liquidity is what keeps an ETF’s market price anchored to its underlying value. When trading is thin or supply is restricted, prices can drift away from NAV (net asset value). And that is where the hidden cost comes from.

What a price and NAV gap lead to

Every ETF has two numbers. First, the net asset value or NAV, which is the fair value of the underlying asset or index. Second is the market price at which the ETF trades on the exchange.

Ideally, the two should be nearly identical. Market makers and arbitrageurs usually ensure that. But gaps still often emerge.

At times, ETFs trade above their NAV (at a premium) or below it (at a discount). When this gap widens significantly, investors can unknowingly overpay or sell for less than the underlying asset or index is worth. And this directly affects what you earn, especially if one is buying at a premium.

How a premium eats into your return

Suppose an ETF whose NAV is Rs 100, but strong demand has pushed its market price to Rs 105. You buy it at Rs 105, effectively paying a 5 per cent premium.

Over the next year, the underlying index rises 10 per cent. The NAV moves from Rs 100 to Rs 110.

But premiums rarely last forever. In most cases, as trading normalises, the ETF’s market price drifts back towards its NAV.

So, if by the time you sell, the premium fades and the ETF trades close to its NAV, you exit at Rs 110. That is a Rs 5 gain, or roughly a 5 per cent return, while the index delivered a 10 per cent return. You earn only half of that.

That is the hidden cost. It does not look like a fee. But once the premium disappears, the damage to your return is already done. The next natural question then is: Which ETFs tend to see such price gaps most often?

Where premiums and discounts show up the most

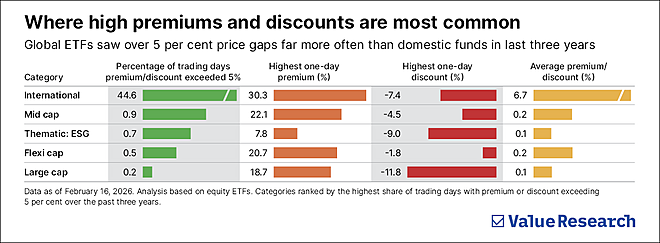

For that, we looked at all equity ETF categories over the past three years and calculated how often the average ETF in each traded at a premium or discount of over 5 per cent, large enough to materially affect returns.

We then identified the categories where such large deviations occurred most frequently.

For most domestic categories, such as large-cap, flexi-cap and mid-cap ETFs, instances where the price moved more than 5 per cent away from NAV were extremely few.

But the average international ETF traded at a premium or discount of over 5 per cent on nearly 45 per cent of trading days (see the table ‘Where high premiums and discounts are most common’).

The reason is the RBI’s overall overseas investment limit of $1 billion in international ETFs. When it is breached, fund houses cannot create fresh units in global ETFs and demand thus outstrips supply, leading to premiums. Discounts emerge when selling pressure outweighs demand, especially in thinly traded ETFs.

In short, for most domestic equity ETFs, large premiums or discounts have been rare. But in international ETFs, they have been frequent enough to warrant caution.

How to avoid paying the wrong price

A few basic checks can keep you from overpaying or exiting below fair value.

- Check the iNAV (indicative net asset value) before placing your order. This gives a live indicative NAV during market hours.

- Avoid market orders in thinly traded ETFs and use limit orders so you control the price you pay.

- Be especially cautious with international ETFs where large deviations are more frequent.

ETFs remain an efficient, low-cost way to gain market exposure. But their low costs cannot compensate for overpaying at entry. Before you click ‘buy’, take a moment to check what you are really paying for.

This article was originally published on March 01, 2026.

Ask Value Research ![]()