Aditya Roy/AI-Generated Image

Aditya Roy/AI-Generated Image

Summary:Taxes impact returns. The same market gain can mean very different post-tax outcomes depending on the wrapper you choose. Before you invest, it helps to know what gets taxed, when and how much. This guide breaks it down in a way that actually makes sense.

Understanding asset taxation does not require memorising every provision of the income tax act. What investors need is a simple framework to classify any investment and determine its post-tax outcome before committing capital. This guide aims to provide that framework.

For each asset class, this guide answers four essential questions:

- What will be taxed? Whether capital gains, interest income, or periodic distributions?

- When will tax apply? On sale, on payouts, or both?

- How long should you hold? Or the minimum period for long-term classification

- What the applicable tax rate is for short-term and long-term gains

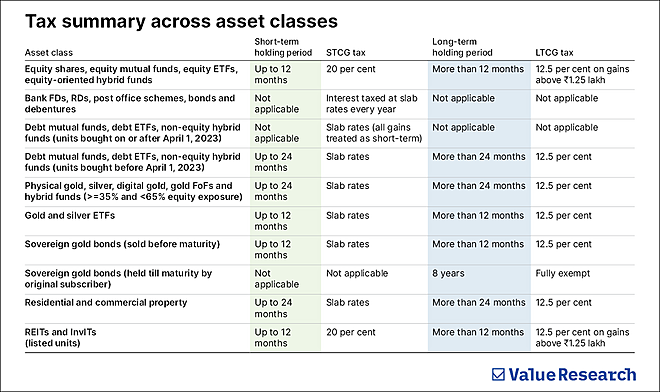

Equity and equity-oriented instruments

Equity investments include listed equity shares, equity-oriented mutual funds (including equity index funds and ETFs), and equity-oriented hybrid funds, which maintain a minimum gross allocation of 65 per cent in domestic equity shares.

Capital gains tax applies only when an investor sells or redeems the investment. Dividends, meanwhile, are taxed separately at the investor’s applicable income tax slab rate. If an equity investment is sold within 12 months of purchase, a short-term capital gains tax of 20 per cent applies. When held for more than 12 months, long-term capital gains tax of 12.5 per cent is levied but only on gains exceeding Rs 1.25 lakh in a financial year.

This tax treatment, however, applies only to domestic equity mutual funds. Mutual funds that invest exclusively in international equities are not classified as domestic equity funds for tax purposes. In such funds, gains are taxed at 12.5 per cent if the units are sold after two years from the date of investment. If the units are sold within two years, the entire gain is added to the investor’s income and taxed according to the applicable slab rate. As with domestic funds, no tax is payable as long as the units continue to be held.

Debt and fixed income instruments

Debt instruments represent the lending side of the capital market. Their taxation reflects two distinct approaches: instruments where returns are driven by interest and taxed as income, and those where returns arise from price appreciation and are taxed as capital gains.

A. Interest-driven fixed income products: Traditional fixed income products generate returns primarily through interest accrual. These instruments are taxed annually on the interest earned rather than on capital appreciation. As a result, the tax liability arises each year regardless of withdrawal.

This category includes bank fixed deposits, recurring deposits, post office savings schemes, corporate bonds, government securities, and debentures, excluding market-linked debentures. Interest income from these instruments is classified as ‘income from other sources’, added to the investor’s total income and taxed at the applicable slab rate, which can range from 5 per cent to 30 per cent depending on overall income. Note that some old government bonds continue to enjoy exemption from tax on interest income until maturity. Separately, banks and companies deduct tax at source (TDS) on interest once it crosses specified thresholds. Any excess TDS deducted can be claimed back while filing the income tax return.

B. Debt mutual funds, debt ETFs, and non-equity hybrid funds: This category includes debt mutual funds, debt exchange-traded funds (ETFs), and hybrid funds with an equity allocation of below 35 per cent. The taxation of debt mutual funds has undergone significant changes following Budget 2023 and Budget 2024, with the removal of preferential long-term capital gains treatment for most investors.

For debt mutual fund units purchased on or after April 1, 2023, all gains are treated as short-term capital gains, irrespective of how long the investment is held. In effect, the holding period no longer matters for tax purposes. The gains are taxed at the investor’s applicable income-tax slab rate, with no long-term tax benefit and no indexation. Debt fund taxation, therefore, now closely mirrors that of fixed deposits. But remember that tax in this case is payable only when the units are sold or redeemed, not on an accrual basis, unlike interest from fixed income products.

The rules, meanwhile, are different for debt fund units purchased before April 1, 2023, which continue to enjoy limited grandfathering benefits. For these older investments, the distinction between short-term and long-term holding still applies. If the units are sold within 24 months, the gains are treated as short-term and taxed at slab rates. If the units are sold after 24 months, the gains qualify as long-term and taxed at 12.5 per cent.

Gold and precious metals

Gold investments span multiple formats, each with distinct tax implications. The choice of wrapper significantly affects tax outcomes despite identical underlying exposure to gold prices.

A. Physical gold, silver and digital gold: Physical gold and silver include jewellery, coins, bars, and digital gold purchased through approved platforms. These are treated as capital assets with taxation arising on both purchase and sale.

At the time of purchase, a goods and services tax (GST) of 3 per cent is levied on the value of gold or silver. In the case of jewellery, making charges also attract GST typically at an effective rate of around 5 per cent.

Capital gains arise when the asset is sold and are taxed based on the holding period. A holding period of up to 24 months is treated as short term, with gains taxed at the investor’s applicable income tax slab rate. Holdings beyond 24 months qualify as long term and are taxed at a flat rate of 12.5 per cent.

In the case of inherited gold or silver, the cost of acquisition and the holding period of the original owner are used for tax computation. No separate inheritance tax on such assets is levied in India.

Note that gold and silver fund-of-funds, as well as hybrid funds with an equity exposure between 35 and 65 per cent, follow the same tax treatment as physical gold or silver. However, unlike physical holdings, no GST is levied on their purchase or sale.

B. Gold and silver ETFs: Gold exchange-traded funds (ETFs) track the price of physical gold and are traded on stock exchanges. For tax purposes, however, gold ETFs are classified as non-equity instruments, despite being market-traded. This category also includes listed silver ETFs.

Capital gains arise only when the units are sold or redeemed. If the holding period is up to 12 months, the gains are treated as short term and taxed at the investor’s applicable income tax slab rate. For holdings beyond 12 months, the gains are taxed at a flat rate of 12.5 per cent. As these ETFs are treated as non-equity instruments, they are not eligible for the Rs 1.25 lakh long-term capital gains exemption that applies to equity investments.

C. Sovereign gold bonds (SGBs): Sovereign gold bonds (SGBs) are government securities denominated in grams of gold, issued by the Reserve Bank of India. They represent government debt backed by gold and carry unique tax benefits unavailable to other gold investment formats. The government stopped issuing new SGBs in February 2024 but existing bonds remain active until maturity. SGBs pay 2.5 per cent annual interest on the issue price, paid semi-annually. This interest income is treated as ‘income from other sources’ and taxed at the investor’s applicable income tax slab rate.

Taxation also applies on redemption. But the treatment depends on how and when the bond is exited. SGBs have a maturity of eight years from the date of issuance, with an option to redeem prematurely from the fifth year onward. Under the new rules notified in Budget 2026, only original subscribers who purchased the bonds at the time of initial issuance are fully exempt from capital gains tax on redemption at maturity. Bonds purchased in the secondary market no longer qualify for this exemption, even if they are held until maturity.

Any SGB sold/redeemed before maturity attracts capital gains tax based on the holding period. A holding period up to 12 months is treated as short term and taxed at applicable slab rates. Long-term holding of beyond 12 months attracts a flat 12.5 per cent tax.

Real estate and property

Taxation of real estate operates on two fronts: rental income earned during the holding period

and capital gains arising on sale or transfer.

A. Land and buildings (residential and commercial): Immovable property includes land, residential houses, apartments, commercial buildings, and industrial structures. Agricultural land in urban areas and vacant land also fall under this category. Taxation applies to both periodic rental income and capital gains on eventual sale.

Rental income is taxed as ‘income from house property’ at slab rates after allowing a standard deduction of 30 per cent for property maintenance.

Interest paid on housing loans is also eligible for deduction only if the old tax regime is opted for.

Capital gains arise at the time of sale or transfer. A holding period of up to 24 months from the date of registration is treated as short term, with gains added to total income and taxed at the applicable slab rates. Holdings beyond 24 months qualify as long term, with gains taxed at a flat 12.5 per cent, without indexation benefit. Note that properties acquired before July 23, 2024, however, are subject to transitional relief. Resident individuals and Hindu Undivided Families (HUFs) can choose between two options: a tax rate of 12.5 per cent without indexation, or 20 per cent with indexation benefits using the Cost Inflation Index. The option that results in a lower tax liability may be selected. For properties purchased on or after July 23, 2024, only the 12.5 per cent rate without indexation applies.

Capital gains exemptions: The Income Tax Act allows investors to avoid or reduce capital gains tax on property sales if the sale proceeds are reinvested in specified assets within prescribed timelines.

If you sell a residential property and use the capital gains to buy another residential house, or construct one within the allowed time, the capital gains tax can be fully or partly avoided. This relief is available if the new house is bought within one year before or two years after the sale, or constructed within three years.

If you sell any long-term asset other than a residential house, such as land or commercial property, and reinvest the sale proceeds in a residential house, similar relief is available, subject to conditions.

Alternatively, capital gains from a property sale can be invested in specified bonds issued by government-backed entities such as the National Highways Authority of India or the Rural Electrification Corporation. The amount invested in these bonds is exempt from capital gains tax, subject to a maximum of Rs 50 lakh, provided the investment is made within six months of sale and held for five years.

These exemptions require careful adherence to prescribed timelines and conditions.

Where only a portion of the sale proceeds are reinvested, the exemption on capital gains is available proportionally.

B. Real estate investment trusts (REITs) and infrastructure investment trusts (InvITs): REITs and InvITs combine features of both equity and debt. While their units are traded like shares, investors also receive periodic cash distributions similar to dividends. As a result, their taxation falls in two dimensions: on distributions received during the holding period and capital gains arising on the sale of units.

Taxation of distributions: REITs and InvITs operate under a pass-through taxation framework, under which income retains its original character as it flows from the trust to the unitholder. Each component of the distribution is therefore taxed differently, depending on its nature.

Interest income distributed by the trust is taxed under the ‘income from other sources’ head and added to the investor’s total income. It is taxed at the applicable slab rate, with tax deducted at source (TDS) at 10 per cent for resident investors.

Dividend income is taxed based on whether the underlying special purpose vehicle (SPV) has opted for the concessional corporate tax regime (which allows companies to pay a lower tax rate if they give up certain deductions and exemptions). If the SPV has opted for this lower tax option, dividends received by unitholders are taxed at their applicable slab rate, with 10 per cent TDS. If the SPV has not opted for this concessional regime, dividends are exempt from tax in the hands of the unitholder.

Return of capital (a payout of your original investment, not income) is not immediately taxable but reduces the cost of acquisition for future capital gains computation.

To enable correct tax reporting, REITs and InvITs provide a detailed break-up of distributions in Form 64B, which investors should rely on for accurate classification.

Taxation of capital gains on unit sale: Capital gains arising from the sale of REIT and InvIT units are taxed separately from distributions. For capital gains purposes, these units are treated as listed securities. A holding period of up to 12 months is considered short term, with gains taxed at a flat rate of 20 per cent. Holdings beyond 12 months qualify as long term. Long-term capital gains are taxed at 12.5 per cent on gains exceeding Rs 1.25 lakh in a financial year, with gains up to Rs 1.25 lakh remaining exempt.

Remember

Taxes don’t just shape returns at the time of exit. They shape outcomes from the moment an investment is chosen. Knowing how different products are taxed helps investors avoid surprises and keep more of what they earn.

Remember that similar investments can be taxed very differently, holding periods are not uniform, and tax rule changes in recent years have reduced or removed long-term tax advantages in several categories.

Factoring in these realities early can lead to better decisions and post-tax returns.

Also read: Budget Roundtable 2026

Ask Value Research ![]()