Reliance AMC has 26 schemes, of which 14 are equity and 12 are debt, besides 3 ETFs and 6 other sector and thematic funds. The equity schemes are managed considering not just the market capitalisation of a stock, but by delving into its market dynamics and the liquidity it offers before considering it to be a large-cap grade stock. Similarly, the fund managers stick to the core philosophy of the scheme irrespective of the market conditions. So, a stock's market capitalisation may go up, but it may still not provide liquidity that large-caps are known for and hence it would not be classified large-cap.

In the case of equity funds, cash is not a driver of performance and returns. The AMC uses it as a portfolio tool, depending on specific schemes. For instance, every scheme filed after 2006-07 follows a maximum cash allocation up to 20 per cent, unlike an earlier 25-25 per cent. The fund has changed the approach to cash by maintaining cash allocation to 3-4 per cent, with the intention of staying fully invested.

Although there are several overlaps in the orientation of fund schemes based on our classification, the AMC claims a distinct investment mandate, a unique identity and a legitimate presence in its portfolio for each.

In case of debt funds, the schemes are segregated based on the degree of the credit and duration risks that each scheme can be exposed to, leaving it for the investor to choose as per his risk appetite and asset allocation. This approach is adopted to check dilution in the investment mandate for a scheme. For instance, there are instances when a short-term fund could become an income fund and vice-versa in certain market conditions. However, this may not be the objective with which an investor has invested. To check such aberrations, the debt fund universe is positioned across the yield curve and also in terms of credit exposure. This helps investors with understanding potential returns and risks before investing.

The fund house plays a big role in the sector and thematic fund universe, where it has some dominant schemes which manage assets that are bigger than several diversified schemes.Best and worst performers

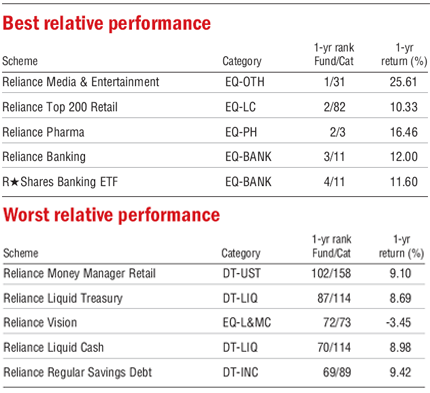

For an AMC with over 185 fund schemes across categories, it is natural to have funds with varied performance. A bulk of its debt funds have performed better than the median. However, the same cannot be said for the equity funds, even though Reliance Top 200 and Reliance Equity Opportunities are strong contenders in the broad diversified equity category among the top performers.

The fund house has robustly-performing sector and thematic funds, with some of them being dominant players in the niches that they operate in. Some of the dominant offerings such as Reliance Natural Resources fund mopped up Rs 5,660 crore in its NFO in 2008; and has regularly posted negative returns. On the other hand, Reliance Diversified Power Sector fund, which was launched in 2004 was one of the best-performing funds for several years before the theme lost its steam and sank to the bottom of the table. The poorest performers from the AMC are its infrastructure funds, which are the worst in the category. Among the broad diversified equity schemes, Reliance Vision, one of the oldest offering, is one of the worst performers among large- and mid-cap funds.

Read part I of the article here

This article was originally published on April 18, 2013.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()