Nitin Yadav/AI-Generated Image

Nitin Yadav/AI-Generated Image

Summary:Think FDs and debt funds are taxed the same now? Think again. The tax rate may be identical, but the timing isn’t. And that subtle difference could cost you lakhs. Discover how a small shift in strategy can help your money grow smarter. Log in to read the full story.

Fixed deposits feel safe, predictable and reassuring. For many investors, they’re the default option for preserving capital and earning steady interest. But what if your FD is quietly eroding your returns, not because of the bank, but because of the taxman?

Since April 2023, debt mutual funds and FDs are taxed identically, based on your income slab. That wasn’t always the case. Until March 2023, debt funds enjoyed a key advantage: if you held them for over three years, your gains were taxed at just 20 per cent after applying indexation. This significantly reduced the tax bite. But that benefit is now gone. From April 2023 onwards, all gains—whether short or long term—are taxed as per your slab.

So, yes, the tax rates are now the same. But one crucial difference remains: when the tax gets applied.

The hidden difference: When you pay tax

FDs: Taxed every year

Interest from FDs is taxed annually, even if you don’t withdraw it. So, your money gets taxed before it can compound fully. In effect, the taxman takes a cut every year.

Debt funds: Taxed at exit

Debt funds only attract tax when you redeem. Until then, your returns grow uninterrupted. It’s like giving your money a longer runway before the tax drag kicks in.

How much of a difference does it make?

Let’s take a simple case. Say you invest Rs 10 lakh for 5 years, and, both FDs and debt funds deliver 6.5 per cent annually. Here’s how the post-tax value changes across tax slabs.

Tax timing matters more than tax rate

FDs and debt funds with the same return produce different outcomes due to when tax is applied

| Income tax rate (%) | FD value after 5 years (Rs lakh) | Debt fund value after 5 years (Rs lakh) |

|---|---|---|

| 5 | 13.49 | 13.52 |

| 10 | 13.29 | 13.33 |

| 15 | 13.09 | 13.15 |

| 20 | 12.88 | 12.96 |

| 25 | 12.69 | 12.78 |

| 30 | 12.49 | 12.59 |

| The above values are calculated on a post-tax basis and assuming similar return of 6.5 per cent. For FD, interest is assumed to be reinvested at the same rate. | ||

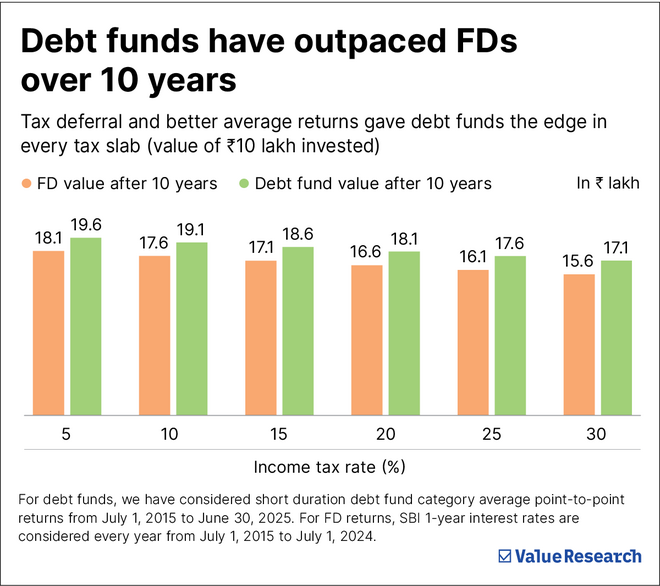

What history tells us: 10-year real-world comparison

To test this theory, we looked at actual returns over the last 10 years.

- Rs 10 lakh in SBI’s 1-year FD (rolled over yearly)

- Rs 10 lakh in a short-duration debt fund

- Timeframe: July 1, 2015 to July 1, 2025

- Post-tax values calculated using applicable slab rates every year

While tax deferral helps, the difference isn’t just about when you pay tax. Over the past decade, short-duration debt funds have also delivered slightly higher pre-tax returns than 1-year FDs, thanks to better yield management and access to corporate debt. Even a 0.5–1 per cent annual edge, compounded over time, adds up. When combined with tax efficiency, the result is a noticeable boost in post-tax wealth.

Strategy spotlight: Planning for lower future tax slabs

Consider this: you’re in the 30 per cent tax slab today and planning to retire in 10 years. You invest Rs 20 lakh today.

With FDs

Every year, you pay 30 per cent tax on interest earned, reducing compounding and giving more to the government.

With debt funds

No tax while you’re invested. When you redeem in retirement, you may fall into a lower slab, say, 10 per cent. That’s a substantial tax saving. More money stays in your hands.

It’s the same tax rule but applied at a more opportune time.

But FDs still have a role

If you’re a senior citizen earning below the taxable limit, or someone who prioritises guaranteed returns over market-linked outcomes, FDs can still serve you well.

Debt funds carry some risk such as interest rate fluctuations, credit events or fund manager missteps. Remember Franklin Templeton’s 2020 credit crisis? While these risks are typically low in short-duration funds, they’re not zero.

So, the right choice depends on your risk tolerance, income profile and investment horizon. Stick to well-rated, short-duration debt funds with limited credit exposure. Avoid chasing yield in exotic categories.

Make your investments work smarter

Don’t let annual taxes eat into your returns year after year. Whether you're building a retirement corpus or parking short-term surplus, how and when you pay tax can shape your final outcome. That’s where a thoughtfully designed investment plan makes a difference.

At Value Research Fund Advisor, we help you craft a smarter investment plan—one that minimises tax drag, optimises returns and quietly builds your wealth. Ready to unlock your money’s full potential?

Ask Value Research ![]()