Aditya Roy/AI-Generated Image

Aditya Roy/AI-Generated Image

91 per cent of traders in equity derivatives lost money in FY25—an average of over Rs 1 lakh gone. But if that same amount had simply been parked in a plain-vanilla ETF, the outcome would’ve looked very different. In this story, we explore how a quiet, no-drama investing strategy using ETFs could have delivered steady, long-term gains. So, let’s look at the numbers.

In a sobering reality check, a SEBI report recently revealed that 91 per cent of individual traders in equity derivatives lost money in FY25. The average loss? A staggering Rs 1.1 lakh per trader. Just 9 per cent managed to eke out a profit.

This statistic reveals a harsh truth: the vast majority of retail traders are not making money from the market. And yet, the allure of fast profits from options, futures and intraday trades continues to seduce lakhs of investors. What few realise is that success in the market doesn’t come from trying to outsmart it every day. It comes from choosing a strategy that works with time and patience.

What if that Rs 1 lakh was invested in a boring ETF?

Had you invested that Rs 1 lakh, lost to derivatives, in a simple Nifty 50 ETF, you’d have had an 85 per cent chance of making a profit within a year. Compare that with dabbling in F&O trades, where only one in 10 people manage to walk away with gains.

The data is clear. Even being conservative and sticking to India’s largest, most stable companies makes it far more likely to earn profits than chasing short-term trades, where most lose money. And that’s just the short term.

It is always ideal to invest with a long horizon of at least three to five years. That Rs 1 lakh in a Nifty 50 ETF five years ago would have nearly tripled to Rs 2.7 lakh today—thanks to a 20.1 per cent annual return, partly from the post-Covid rebound. But even if you remove the once-in-a-generation Covid bump, a large-cap ETF still typically delivers around 12–14 per cent annually.

Staying invested for the long term further increases your odds against losses. As our rolling return analysis for the last decade shows, an investor who had stayed invested in the Nifty 50 for five years would have almost never lost money.

Therefore, just sticking to the market benchmark and giving it time offers far more chances of making gains.

Longer the horizon, higher the odds in your favour

| Time period | % of times returns were positive | Worst return | Best return | Average return |

|---|---|---|---|---|

| 1 year | 85.3% | -32.7% | 96.33 | 13.7% |

| 3 years | 99.2% | -4.5% | 32.28 | 13.4% |

| 5 years | 99.9% | -1.2% | 26.17 | 12.9% |

| Nifty 50 TRI returns are calculated on a daily rolling basis over the last 10 years | ||||

And when it comes to large caps, passive investing often outperforms the active route over time because most fund managers struggle to consistently beat their benchmarks.

So, when long-term investing in the index compounds your money reliably without complexity, the next question is: what’s the best way to do it?

ETFs offer a clean, efficient answer.

Why choose ETFs for index investing?

- Low cost: The average expense ratio for large-cap ETFs is just 0.16 per cent, far lower than the 0.85 per cent charged by active large-cap mutual funds.

- No fund manager risk: ETFs follow a rule-based, passive structure, removing human discretion, biases and the risk of underperformance from active calls.

- Easy diversification: A single ETF gives you exposure to dozens of top companies, automatically spreading your risk.

- Suitable for traders: If you are a demat account holder and know how to trade a stock, you already know how to buy an ETF, avoiding complexity or cost drag.

A simple ETF portfolio that works

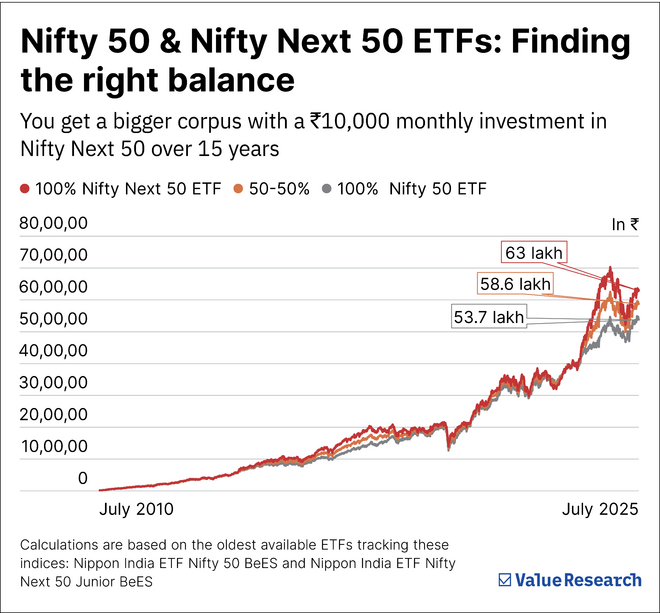

How would a long-term investment strategy in ETFs fare? Let’s say you invested Rs 10,000 monthly over the past 15 years in:

- Only a Nifty 50 ETF

- A Nifty 50 and a Nifty Next 50 ETF split equally

- Only a Nifty Next 50 ETF

The Nifty Next 50 ETF would have built the largest corpus, thanks to its higher historical returns—14.6 per cent average five-year rolling return vs 12.9 per cent for the Nifty 50 in the last 10 years.

But note that the Nifty Next 50, which offers exposure to emerging large caps, also tends to be more volatile. For instance, in the latest correction, it fell 24.6 per cent versus the Nifty 50’s 15.4 per cent drop. In three of the five major market declines over the last 15 years, the Nifty Next 50 also fell an average of 2.8 percentage points more than the Nifty 50.

That’s why investors can tailor their ETF mix based on their risk appetite. Want stability? Stick with the Nifty 50. Want a little extra growth? Add some exposure to Nifty Next 50. Either way, you’re still ahead of the trader chasing short-term highs and long-term regrets.

Skip the noise. Stay the course. Let it work.

ETFs aren’t flashy. They don’t promise overnight riches. But over time, they quietly outperform most investors trying to outguess the market. So if you're serious about building wealth, stop chasing trades and start holding what matters. Because the most profitable call isn’t deciding when and how to trade. It’s knowing when to stop.

Want to invest Rs 5,000+ SIP in ETFs?

Let us help you do it the right way. With Value Research Fund Advisor, you get handpicked ETF recommendations, built for long-term wealth creation—not market noise. Whether you're starting fresh or shifting from trading losses, our guidance keeps it simple, low-cost, and effective. No hype. Just strategies that work. Join Fund Advisor and start your ETF investment with confidence.

An investor education and awareness initiative of Nippon India Mutual Fund.

Helpful Information for Mutual Fund Investors: All Mutual Fund investors have to go through a one-time KYC (know your Customer) process. Investors should deal only with registered mutual funds, to be verified on SEBI website under 'Intermediaries/Market Infrastructure Institutions'. For redressal of your complaints, you may please visit www.scores.gov.in. For more info on KYC, change in various details and redressal of complaints, visit mf.nipponindiaim.com/InvestorEducation/what-to-know-when-investing.

Also read: The average trader lost ₹1.1 lakh in F&O in FY25. Here's why

This article was originally published on July 17, 2025.

Ask Value Research ![]()