AI-generated image

AI-generated image

The smartest way to build wealth lacks the drama of timing the market, picking hot stocks and chasing trends. Instead, you need consistency, clarity and control.

A thoughtfully constructed, low-cost portfolio can help you ride the ups and downs of the market while steadily building wealth. One of the easiest ways to achieve this is through a balanced allocation between large-cap, mid-cap and small-cap mutual funds, with the bulk in index funds.

Here's a simple, effective mix:

- 70 per cent in large-cap index funds for stability and predictability,

- 20 per cent in actively managed mid-cap funds for targeted growth, and

- 10 per cent in actively managed small-cap funds for high-return potential.

This may sound too simple, but that's exactly the point. A low-cost, disciplined strategy like this can help you create real wealth over time without the stress of stock picking or second-guessing fund managers.

Why index funds for large-caps?

The large-cap space is dominated by the biggest companies in the country—think Reliance, Infosys, HDFC Bank, among others. These stocks are heavily tracked and well understood, making it tough for fund managers of active large-cap funds to consistently find an edge over vanilla, passive funds that merely track the large-cap index.

The data backs this up. Based on daily rolling returns over the last decade:

- Only 41 per cent of actively managed large-cap funds beat their category benchmark (Nifty 100 TRI) over five-year periods.

- Extend that to seven-year periods, and the success rate drops further to just 25 per cent.

In short, passive-managed index funds fare better in the large-cap space.

Not only do they fare better, index funds charge lower commissions in the form of expense ratios. Meaning, you end up earning more in the long run.

Why active funds for mid- and small-caps?

While index funds generally outperform funds with active investing strategies in the large-cap world, it's a different story in the mid- and small-cap segments, provided you give them time.

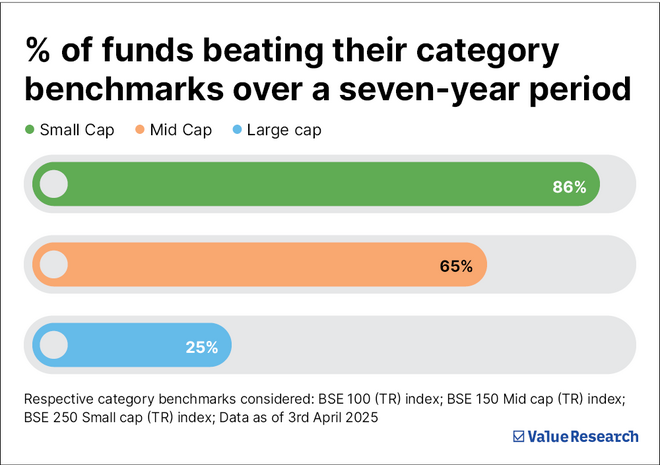

Over seven-year rolling periods:

- 65 per cent of mid-cap funds outperformed the category benchmark (NIFTY Midcap 150 TRI).

- 86 per cent of small-cap funds beat the NIFTY Smallcap 250 TRI.

Why have we looked at a seven-year timeframe? Because when investing in mid- and small-cap funds, a seven-year horizon is the bare minimum one should consider. These segments can be extremely volatile over shorter periods, and only patient investors tend to benefit from the long-term potential they offer.

Think of mid- and small-caps as the spice in your portfolio—not too much, and only if you're ready for the heat.

Is 70/20/10 strategy in a large/mid/small-cap fund effective?

If you had followed this 70-20-10 allocation and invested Rs 10,000 per month over the last 10 years, your portfolio would now be worth approximately Rs 26.1 lakh. That translates to an annualised return of 14.8 per cent—a fantastic result for a hands-off, rule-based strategy.

Here's how the components contributed:

- Rs 7,000 monthly (70 per cent of the Rs 10,000 monthly SIP) in large-cap index funds grew to Rs 17.7 lakh.

- Rs 2,000 in mid-cap active funds became Rs 5.6 lakh.

- Rs 1,000 in small-cap funds rose to Rs 2.8 lakh.

No guesswork. No manager hopping. Just discipline and time.

The bottom line

You don't need a complicated strategy to build wealth. In fact, the simpler and more systematic it is, the more likely you are to stick with it through market ups and downs.

By constructing your portfolio with low-cost large-cap index funds and complementing it with selective, long-term exposure to mid- and small-cap funds, you create a portfolio that's cost-efficient, diversified and built for long-term growth.

All it needs is patience—and a long enough horizon to let the market work in your favour.

As Jack Bogle, the father of index investing, put it: "Don't look for the needle in the haystack, just buy the haystack."

An investor education and awareness initiative of Nippon India Mutual Fund.

Helpful Information for Mutual Fund Investors: All Mutual Fund investors have to go through a one-time KYC (know your Customer) process. Investors should deal only with registered mutual funds, to be verified on SEBI website under 'Intermediaries/Market Infrastructure Institutions'. For redressal of your complaints, you may please visit www.scores.gov.in For more info on KYC, change in various details and redressal of complaints, visit mf.nipponindiaim.com/InvestorEducation/what-to-know-when-investing

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Also read: How to choose the right index fund

This article was originally published on April 15, 2025.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()