Adobe Stock

Adobe Stock

Investment management has undergone seismic shifts over the decades. Once dominated by stock-picking fund managers, the industry has moved towards more systematic approaches, leading to passive investing and eventually, smart-beta strategies. This shift reflects a broader pursuit of efficiency and reliable returns.

Today, factor investing, a key pillar of smart-beta investing, reshapes portfolio construction by blending active and passive elements. But how did we get here? The journey from active management to indexing and now to smart beta is a story of financial innovation.

From active to passive to smart beta

1950s-1980s: Rise of active investing: For much of the 20th century, active management was the gold standard in investing. Legendary fund managers like Peter Lynch of Fidelity Magellan Fund and Anthony Bolton of Fidelity Special Situations Fund built their reputations by picking winning stocks.

The appeal of alpha - outperforming the market - made active funds the preferred choice for investors. Yet, this approach came with a major flaw: inconsistency. While some managers delivered a stellar performance, most struggled to beat the market consistently.

1970s-1990s: Move towards passive investing: In 1976, John Bogle revolutionised investing by launching the first index mutual fund (Vanguard 500 Index Fund). His idea: if you can't beat the market, just be the market. Index funds tracked broad market indices like the S&P 500, offering:

- Low costs: Eliminated expensive fund management fees.

- Simplicity: Offered diversified exposure without stock-picking.

- Market-matching returns: Allowed investors to benefit from long-term growth.

By 2024, passive funds comprised 60 per cent of US mutual fund and ETF (exchange-traded funds) assets (Bloomberg). Yet, traditional indexing lacked the ability to target specific factors that enhanced risk-adjusted returns, paving the way for Smart Beta.

1990s-present: Birth of smart beta: As researchers scrutinised market efficiency, they discovered persistent factors that influenced long-term stock returns. Eugene Fama and Kenneth French (1993) introduced the Three-Factor Model, adding size and value to market beta. Later, Mark Carhart (1997) introduced momentum, highlighting that strong past performers often continue outperforming.

This research laid the foundation for smart beta, which blends passive investing's structure with active investing's ability to target inefficiencies. Unlike traditional index funds, smart beta strategies weigh stocks based on factors like quality, momentum, and low volatility rather than market cap.

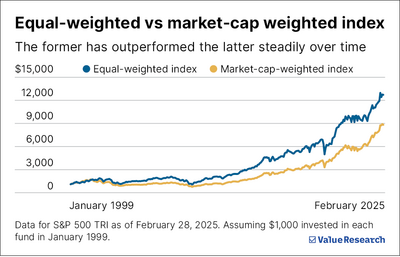

The chart above highlights equal-weighted indices outperforming market-cap-weighted ones, proving that even simple rule-based alterations in portfolio allocations can drive better returns - a key principle behind factor investing.

Smart beta: From theory to practice

For decades, factor investing remained an academic concept, with little real-world adoption. Throughout the 1980s and early 1990s, asset managers were intrigued but cautious - data was scarce, and transaction costs were high.

By the mid-1990s, technology and data analytics advanced, allowing firms like Dimensional Fund Advisors (DFA, led by David Booth and Rex Sinquefield and influenced by Eugene Fama), to pioneer factor-based investing. In 1993, DFA launched the US Small Cap Value Portfolio, among the first to apply size and value factors in practice.

The 2000s saw the rise of factor-based indices, with MSCI, S&P Dow Jones, and FTSE Russell designing benchmarks targeting value, momentum, and low volatility. Institutions like BlackRock and AQR Capital embraced multi-factor investing, refining strategies that combined multiple factors.

By 2014, Vanguard further democratized factor investing, introducing low-cost ETFs such as Vanguard Value ETF (VTV) and Vanguard Small-Cap Value ETF (VBR), making systematic investing more accessible to everyday investors. Factor investing was no longer just an idea - it was a fundamental shift in portfolio management.

Rise of ETFs and smart-beta strategies

The ETF boom has accelerated factor investing, with global ETF assets surpassing $14.8 trillion in 2024 (as per ETFGI, a consultancy firm). Smart beta ETFs now capture a growing share as investors seek rules-based strategies that enhance returns while reducing human bias.

Institutional investors, including pension and sovereign wealth funds, leverage factor investing for diversification and precision. Retail investors also benefit, with Google Trends showing a 10x surge in India's interest in factor investing over the past seven years.

The present and the future

Investors increasingly see factor-based strategies as a superior approach to portfolio management. At NJ AMC, we hold a first-mover advantage with NJ Smart Beta, a cutting-edge platform that enables error-free back-testing and portfolio analysis. Factor investing is no longer theoretical - it's the future. And with pioneers like us leading the way, the shift toward smarter, data-driven investing has just begun.

Nirmay Choksi is the Director and Head of Investment of NJ Asset Management Private Limited. The views expressed above are his own.

Ask Value Research ![]()