Factor investing is no longer the exclusive domain of academics and financial theorists. It has emerged as a sophisticated yet accessible strategy for retail and institutional investors alike. By understanding and applying the principles of factor investing, one can enhance returns, reduce risks and build resilient portfolios. NJ Mutual Fund takes pride in leading this transformative investment strategy with cutting-edge insights and a disciplined approach.

The foundation of factors

At its core, factor investing involves identifying measurable characteristics that drive returns and risks. These characteristics, known as factors, have been rigorously studied and validated over decades. Think of factors as the DNA of investing - the fundamental building blocks that explain why certain securities outperform others. Factors like Quality, Value, Momentum, Size and Low Volatility consistently influence investment outcomes.

Cricket fans can relate to this concept when assembling a dream team — Sachin's precision (Quality), Dhoni's composure (Low Volatility), Sehwag's explosive scoring (Momentum) and Dravid's steadfast defence (Value). Together, they form a winning combination.

What sets factors apart?

Not all investment characteristics qualify as true factors. To be recognised, a factor must meet certain stringent criteria.

- Persistent: Delivers returns consistently over long time horizons and across market cycles.

- Pervasive: Effective across geographies, asset classes and industries.

- Robust: Stable impact when measured through different metrics.

- Intuitive: Backed by sound economic or behavioural rationale.

- Investable: Feasible to implement.

These qualities ensure that factors are enduring principles, not fleeting trends.

The dual dimensions of factors

Factors are broadly categorised into two types:

- Macroeconomic: Reflect broad economic conditions like GDP growth, inflation or interest rates, guiding asset allocation across equities, bonds and commodities.

- Style: Focus on specific attributes within an asset class, such as Quality, Value, Momentum and Low Volatility, used for security selection and portfolio construction.

Style factors respond dynamically to macroeconomic environments. For instance, momentum stocks thrive during economic expansions, while low-volatility stocks outperform during downturns.

Why factors matter: Evidence and insights

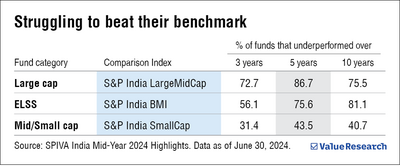

The allure of factor investing lies in its systematic outperformance of traditional strategies. Both theory and evidence highlight its effectiveness. Consider the SPIVA (S&P Indices versus Active) reports, which track the performance of active fund managers. As of June 2024, over 75 per cent of large-cap, mid-cap and small-cap funds in the US underperformed their benchmarks over the past decade. In India, over 75 per cent of large-cap funds lagged behind their benchmarks.

Why does this happen? Active investing often succumbs to human biases and emotional decision-making. Factor investing provides a disciplined alternative, eliminating cognitive errors by adhering to predefined rules.

For example, Quality-focused strategies invest in companies with strong fundamentals, consistent profitability and low debt, offering stability during downturns. Value strategies capitalise on mispriced opportunities, investing in undervalued stocks poised for long-term growth. Momentum strategies ride recent winners, while Low Volatility strategies cater to risk-averse investors by focusing on stable, less volatile stocks.

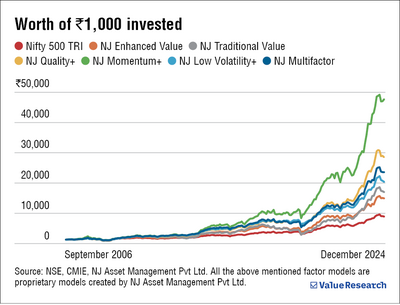

Empirical data reinforces the relevance of factor investing. Backtesting studies reveal that multi-factor portfolios outperform traditional market-cap-weighted indices. This approach is akin to assembling a balanced cricket team where diverse strengths create a resilient, winning combination.

Active vs passive vs factor investing

Factor investing occupies a unique middle ground between active and passive strategies. Active investing relies on fund managers' discretion to outperform benchmarks but is prone to biases. Passive investing merely tracks indices, offering market returns without outperformance potential.

Factor investing marries the best of both worlds. It combines passive strategies' discipline and transparency with active management's alpha-generating potential. By focusing on rules-based selection criteria, it offers a systematic approach to outperforming benchmarks.

The future of factor investing

In the US, equity smart beta AUM has proliferated over the last decade, from nearly $400 billion in 2014 to over $2 trillion in 2024. As the Indian market evolves and data analytics becomes more sophisticated, factor investing is set to play a greater role in portfolio management. NJ Mutual Fund is committed to leading this evolution by providing access to thoughtfully designed, research-backed factor strategies. By embracing technology and empirical research, we empower investors to harness the potential of factor investing.

Whether you're a seasoned investor or just beginning your journey, factor investing provides the tools to achieve financial goals with precision and purpose.

Nirmay Choksi is the Director and Head of Investment of NJ Asset Management Private Limited. The views expressed above are his own.

Ask Value Research ![]()