It is widely believed that by taking bets on a particular factor (such as a theme or investment styles like value, growth, quality, etc.), one can deliver strong performance over time. Often, 'concentrated bets' are associated with 'high conviction,' which is further believed necessary for better performance. However, in reality, this may not be the case.

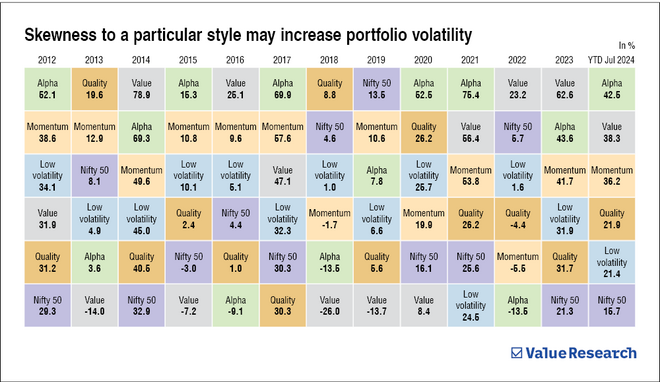

Investors need to remind themselves that "winners rotate." Today's best-performing segment of the market may or may not do well in the future, and vice versa. No particular style performs consistently every year. Likewise, sector and market-cap performance keeps rotating year on year.

Before the comeback in 2021, for three consecutive calendar years (2018, 2019, 2020), value style underperformed most of the other styles of fund management. Quality style worked well in 2018 and 2020 but did poorly in 2017 and 2019.

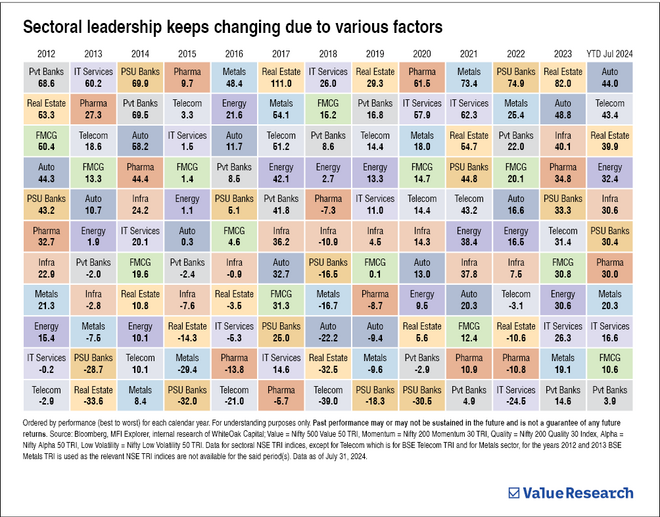

Sectors like IT services and pharma were among the worst-performing in 2016 and 2017 compared to the broader market. Subsequently, IT services outperformed most other sectors in 2018, 2020 and 2021, and pharma outperformed in 2020. Some defensive sectors did well in 2020, but in 2021, many cyclical sectors performed relatively better than the broader market, and defensive sectors were among the laggards.

So, what is the solution to this problem? Let's first discuss a few basic concepts regarding portfolio construction.

Active share vs active risk

Active share is a measure of the percentage of security holdings in a manager's portfolio that differs from the benchmark index. It tracks the disparity between a portfolio manager's holdings and its benchmark index. A low active share score indicates that a portfolio manager is closely replicating the target index (benchmark) and engaging in a passive investment strategy.

A high active share score indicates that a portfolio's holdings diverge from the target index (benchmark), and the portfolio manager is actively managing the portfolio. Managers with reasonably high active share have the potential to outperform their benchmark indices.

Active risk, on the other hand, is a measure of the risk in a portfolio that is due to active management decisions made by the portfolio manager. Higher active share may also introduce active risk if the portfolio is constructed based on any narrow strategy like any factor or combination of factors.

A factor-based investment strategy involves tilting investment portfolios towards and away from specific factors (such as growth, value, low volatility, quality, momentum, small cap, or any other such parameters) in an attempt to generate long-term investment returns in excess of benchmarks. It is essential to create a portfolio in a more scientific way that balances out all such risks and ensures that alpha generation is a function of stock selection (bottom-up). This is called "balancing out the factor risk".

For a better investing experience, the portfolio construction goal should be to achieve 'high active share' with relatively 'low active risk'.

To sum up

A high active share is one of the necessary ingredients for generating potential alpha over the benchmark. Additionally, a factor-diversified balanced portfolio is crucial for a better investing experience with lower alpha volatility.

As seen in the graph, when creating active share with concentrated bets, managers may unconsciously or consciously expose the portfolio or create a tilt toward specific factor risks. This can lead to exaggerated cycles of outperformance and underperformance. Narrow strategies may result in allocational biases, as well as style, sector, or market cap preferences, which can cause the portfolio's performance to experience a high degree of volatility depending on macroeconomic conditions. This is why it is often said that "winners rotate," as the strategies that perform well tend to change every year or two, only to be replaced by another strategy. Conversely, a factor-diversified balanced portfolio helps achieve the desired active share while keeping active risk low due to the balance of these factors.

Hence, when creating an equity portfolio, it is essential for investors to either choose a factor-diversified portfolio or diversify their equity investments across various schemes with different styles and factor tilts to ultimately create a factor-diversified portfolio. This approach should help improve the investing experience over time.

Manuj Jain, a CFA charterholder, is an Associate Director and Co-Head of Product and Strategies at WhiteOak Capital Asset Management Company. He has been with the company for over two years and has over 16 years of experience in asset management. Part of the WhiteOak Capital Group, WhiteOak Capital Asset Management Company is the sponsoring entity of WhiteOak Capital Mutual Fund.

Also read: Achieve your goals with 'chemistry of investing'

Ask Value Research ![]()