A chemical reaction occurs when two or more substances (reactants) are mixed, resulting in one or more new substances. For example, when we combine two atoms of hydrogen with one atom of oxygen, we get H2O, i.e. water. However, if we add one more atom of oxygen, we get H2O2, i.e. hydrogen peroxide (a mild antiseptic used on the skin to prevent infection of minor cuts, scrapes and burns). Adding or subtracting even a small atom can result in completely new substances. To achieve a desired outcome (product), one needs to have a sound understanding of the properties of each atom and how they react when they come together.

Similarly, one should allocate their investment in a combination of various asset classes judiciously. The right mix of these asset classes may help investors achieve an optimal level of risk-adjusted returns.

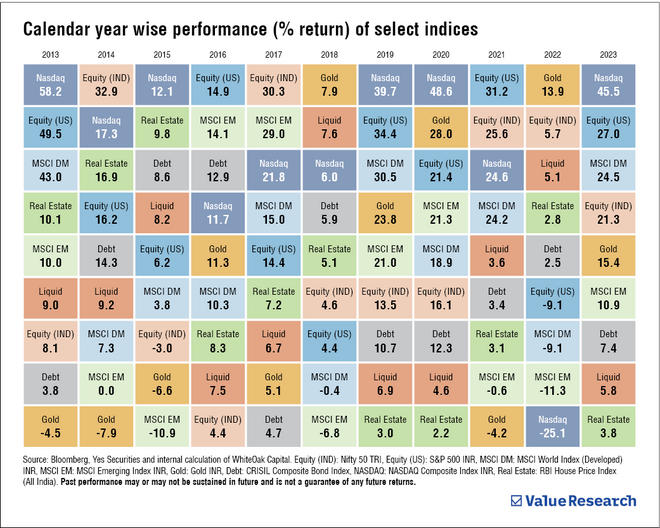

Economic cycles and markets worldwide are very dynamic. Different asset classes tend to perform differently depending on where we are in the economic cycle, geopolitical events, etc. Due to the dynamic nature of international markets and economic cycles, it is not possible to consistently time the winning asset class. Furthermore, there may be a prolonged cycle of outperformance and underperformance of these asset classes.

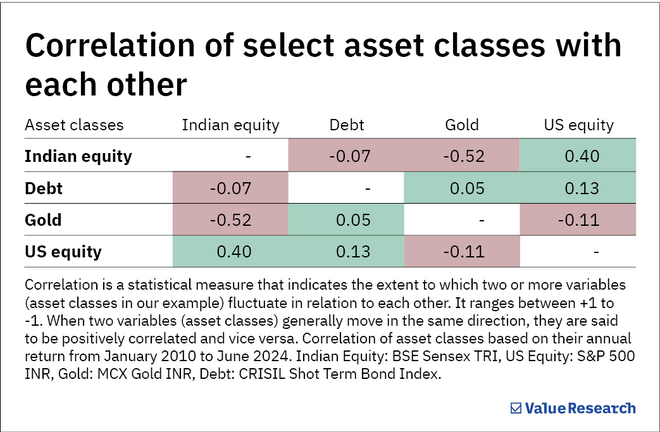

Different asset classes have varied degrees of correlation with each other, and investors can use these correlations to create a portfolio for achieving reasonable returns with moderate volatility from their investment over the long term.

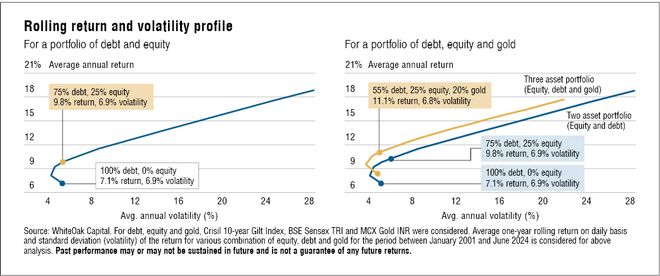

To better understand the parallels between chemistry and investing, one must understand the concept of multi-asset allocation. It is a common perception amongst the investing community that if we add equity to a bond portfolio, we increase the portfolio's risk (volatility). However, this is not true in all cases. As seen in the 'Rolling return and volatility profile' graph, a 100 per cent bond portfolio has delivered an average return of 7.1 per cent with a volatility of 6.9 per cent; by adding 10 per cent equity, volatility reduces to 6 per cent, and the average return improves by 1 per cent.

Notably, a 75 per cent bond and 25 per cent equity combination represents almost similar volatility as a 100 per cent bond portfolio on average, with a 2.7 per cent higher return measured for one year of the average volatility (standard deviation) and average return observations. This means the asset allocation portfolio has delivered better risk-adjusted return than a 100 per cent bond portfolio.

Let's see what happens when we add a third asset class, i.e. gold, to the previously discussed portfolio with two asset classes (debt and equity). Gold, as we know, is negatively correlated with most other asset classes on average. So, when we add 20 per cent gold, the resultant asset allocation becomes 25 per cent equity, 20 per cent gold and 55 per cent debt.

As seen in the 'Rolling return and volatility profile' graph, the return-volatility trendline shifts from right to left, i.e., volatility reduced all three asset combinations (compared to two asset portfolios). The portfolio with 25 per cent equity, 20 per cent gold and 55 per cent bonds has exhibited similar volatility of 6.8 per cent as the 100 per cent bond portfolio along with an average return of 11.1 per cent (i.e., about 4 per cent higher compared to a 7.1 per cent average return from 100 per cent bond portfolio). This clearly shows that adding a judicious combination of low or non-correlated and negatively correlated growing asset classes can achieve a superior risk-adjusted return on the portfolio level.

The irony

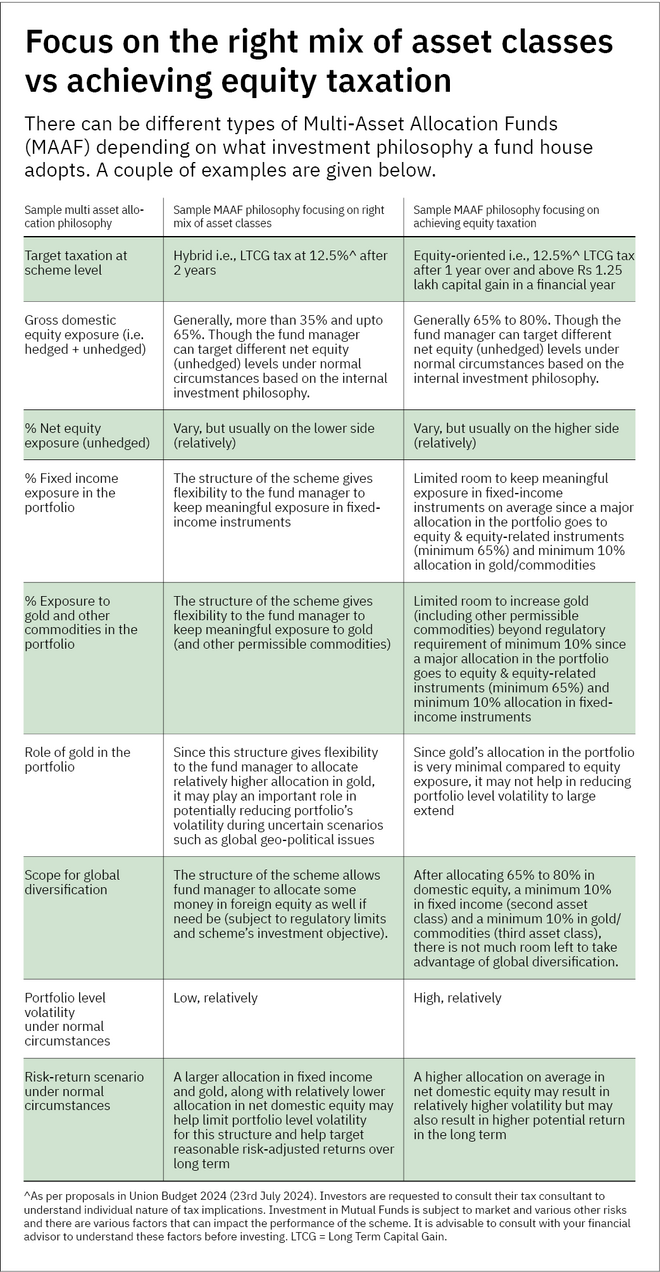

Usually, multi-asset allocation funds have been created with the criteria to qualify for 'equity taxation', i.e., a minimum of 65 per cent equity exposure. This results in the asset classes being combined to look more like 'balanced advantage funds or aggressive hybrid funds with 10 per cent gold/silver'. This requirement of minimising taxation compromises the chemistry of the asset classes to begin with. One cannot create water by insisting it should have a minimum of 80 per cent oxygen.

Summing it up

While the basic characteristics of various multi-asset allocation funds (MAAF) are similar and standardised, the underlying philosophy with which the fund manager manages the scheme portfolio can vary meaningfully from one fund house to another.

We believe that instead of focusing ONLY on optimising for tax, it is better if one (much like a chemical formula) decides to prioritise optimisation for risk-adjusted returns (say, lower volatility and reasonable return over the long term); one can get a totally different suggested mix of asset classes.

The right mix of various asset classes may help investors achieve their long-term financial goals. Hence, it becomes essential for investors to understand the nuance of various philosophies adopted by fund managers and choose an MAAF that matches their long-term financial goals.

Manuj Jain, a CFA charterholder, is an Associate Director and Co-Head of Product and Strategies at WhiteOak Capital Asset Management Company. He has been with the company for over two years and has over 15 years of experience in asset management. Part of the WhiteOak Capital Group, WhiteOak Capital Asset Management Company is the sponsoring entity of WhiteOak Capital Mutual Fund.

Ask Value Research ![]()