I am 33 with a take-home monthly salary of `26,000. My wife and three-year old son are my only dependents. My savings of `60,000 are in my bank while I also have gold ornaments worth `2.5 lakh.

My goal is to have `15,000 a year to pay for my son’s education every year till 2022 and `4 lakh in 2025 for his higher education. I wish to create a monthly income stream of `15,000 for my retirement in 2037. Please advise how I can achieve my goals and whether my investments are good.

-R Siva Prasad

You don’t seem to be in a very good financial shape. The biggest problem with your cash flows is that you seem to be spending much more than what you are earning. Ironically, it is not because you are a spendthrift but simply because you have too many “investments” which are not really productive. However, let’s assume you made a mistake in the numbers but let’s also assume that you do not manage to save at all. Whatever you earn, is spent.

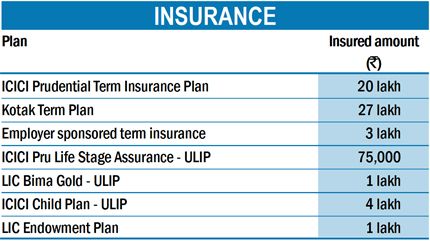

In such a case, any unexpected increase in expenses will leave you in a very tough situation. The good news is that you do not have any loans. You have not mentioned whether or not you have a house of your own and if you do not, do you plan on buying one in the future. So we will keep that issue aside. Also, there is no mention of health insurance, so we are assuming that your employer takes care of that. Hence, we won’t get into that. Take a fresh look at all your insurance plans. You have too many plans and are paying way too much by way of premiums. The term insurance plans are good, the rest are questionable. Also consider discontinuing the chit funds. Your funds are good picks, stick with them.

You do not have any net savings. In fact, your savings are negative which means you are spending more than you are earning. And, this is not even taking into account your premiums for the term insurance policies which you have not mentioned. You probably have made an error in the information submitted.

You have far too many insurance policies, which are a mix of pure risk cover (term insurance) and policies that double up as investment vehicles. You are paying a huge amount every year by way of insurance premiums. Keep your term insurance policies in place. As for the rest, evaluate all of them. Talk to your agent and see what the surrender or termination clauses are. This will free you of future financial commitments and you can safely divert the money towards other forms of investment and savings. We noticed that you do not have a medical insurance police. However, it is probably because your employer provides you with one.

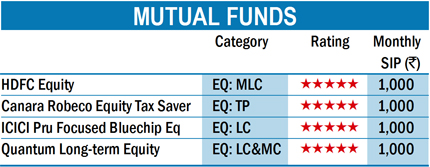

You have picked up some good funds. Your fund portfolio is well diversified across fund houses and categories. Moreover, you have not cluttered your portfolio unnecessarily like so many investors do in their search for diversification. Continue to invest systematically and regularly. In the long run, you will benefit. Review the performance of your funds annually to ensure that you are on track. You can even consider adding a fund that falls in the ‘Equity: Mid & Small Cap’ category if you would like to increase your exposure to mid and small caps. Consider ICICI Prudential Discovery or IDFC Premier Equity if you would like to go with this suggestion.

Your monthly saving in mutual funds should help you meet these goal. Moreover, some of the insurance plans may probably help to some extent, if you do not manage to discontinue them. However, the amounts are not large. *Assuming you will need Rs 15,000 a month for 20 years in retirement, the retirement corpus works to Rs 18 lakh.

Setting financial goals

Saving and investing without purpose is like a treasure hunt without a map. The financial goal to save for your son’s education 13 years from now at `4 lakh and your own retirement income of `15,000 a month 25-years from now is very unrealistic. For instance, the worth of `15,000 25 years from now taking into account 8 per cent inflation works to `1.02 lakh. Likewise, `4 lakh may be sufficient for your son’s education today, but with inflation it will work to `10.87 lakh. These numbers are not to scare you. These are to expose you to reality. You need to take into account inflation when planning future financial goals and you also need to temper your goals depending on your ability to earn as well as invest.

It does not mean that you cannot achieve your goals; to be able to still achieve them you need to invest more and those investments need to definitely earn a lot more than inflation. In the long run, equity is the only inflation beating asset class. The earlier you start taking a higher exposure to equity, the better will it work for you.

You have age on your side and by investing through monthly SIPs in mutual funds, you have set yourself to investing in equity. To benefit the most from the power of equity you need to regularly invest, increase your contributions over time and re-assess your goals and realign if necessary to meet your financial goals.

This article was originally published on July 19, 2012.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()