AI-generated image

AI-generated image

Initially written off, but later celebrated. There's no dearth of such success stories in the Indian markets. Take, for instance, the current star performers like real estate, steel, oil, and coal that were prophesied as bad investments until a few years ago. But their investors are now having the last laugh. A key commonality shared by these industries is their cyclicality. As their cycle turned, so did their fortunes. A similar story is perhaps in the works in the tea plantation sector that has been sentenced into oblivion and for good reasons, too. But what if it has reached its nadir and cannot fall any further?

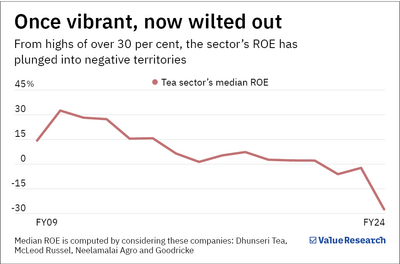

Leaving a bad taste

Tea plantation companies have remained laggards for the past many years. They have generated a median return of -30 per cent since 2018. Mcleod Russel, for instance, has slumped over 87 per cent during this period, primarily because of the company's mismanagement, but also due to sectoral headwinds.

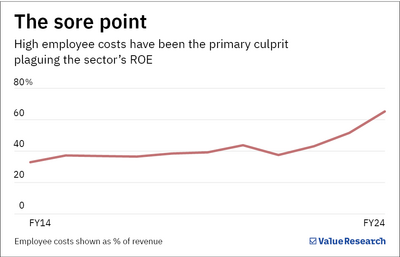

What plagued the sector?

Global tea prices have been stagnant in the last ten years due to oversupply from Africa. To no one's surprise, this hit India hard, which is a key exporter. Further, India's production yields remained lacklustre while the industry's costs increased, eroding their margins. The costs primarily mean employee costs that have remained elevated and are still on a rise due to government regulations, dragging the industry's profitability.

Is the worst over?

Factors to consider to answer the question:

- In the dumps but..

The tea industry is marred with an oversupply problem, which has kept prices suppressed. In case of commodity businesses, economic non-viability leads to many players exiting the industry, effectively restoring the supply-demand gap. This is already being seen in the tea industry where many tea estates and processing facilities have winded down in the past few years. - Hopes of supply disruption

Supply disruption in the industry can be a game-changer that can lift prices and help companies recover their high costs. One such disruption was on account of unfavourable climatic changes that shot up prices recently. Kolkata auction tea prices, widely tracked globally, have doubled in the past three months, from $1.6 per kg in March 2024 to over $3 per kg in May 2024, owing to bad weather conditions in key tea-producing states of Assam and West Bengal. The ongoing logistics issues in the Red Sea have also aided this trend. In fact, the prices of Assam CTC tea, which is the most widely consumed tea in the world, fetched their highest price in the auctions recently. - Solid on consumption

While demand relative to the market supply has been a sore point, global tea consumption is yet to see any signs of decline. The commodity's consumption growth is unlikely to slow down, rather it will likely remain stable in line with the past trends of 3-4 per cent. So, it is only the supply glut that needs repair. - Valuations

The ideal time to invest in cyclical businesses is when they are either trading at high P/E ratios due to low earnings, or when there are no P/E ratios due to losses. Simply put, you gotta catch them before their earnings bottom out. This is the case for all tea stocks at present, which are valued even below their net assets. Take the case of Dhunseri Tea and Industries. It is currently valued at less than half of its book value given its unimpressive financials.

Our view

There is extreme pessimism in the sector given the dwindling profitability and exits of many players. But historically, such conditions have also preceded the turnaround in many commodity and cyclical businesses. Let's circle back to the examples of the oil and coal industries. They were the least favourites in the market due to increasing preference for renewable sources until the Russia-Ukraine war brought the focus back to energy security, helping the duo turn the corner.

That said, before approaching the tea plantation industry as a contrarian play, remember that any recovery largely hinges on a reduction in the overflowing global supply. Moreover, among companies, investors should look out for players that are keenly prioritising improving their operational efficiency.

This story is not a recommendation. Investors must do their own due diligence before making any investment decision.

Also read: Can fertiliser companies keep their heads above water?

Ask Value Research ![]()