Mutual funds have already gained popularity as a preferred investment avenue in India. Many first-time investors are familiar with mutual funds, thanks to various campaigns and investor education initiatives.

According to a recent report by Computer Age Management Services (CAMS ), young people are increasingly following the mutual fund route. Undoubtedly, this is a positive sign for the Indian mutual fund industry. However, it is essential for all budding investors to understand the basics of mutual funds before they begin investing. Once you understand the meaning of a mutual fund, it will be easier for you to take better care of your investments.

What is a mutual fund?

Mutual funds' meaning is simple. As an investment vehicle, a mutual fund is a pool of funds from investors. They invest this money in different financial instruments, including stocks, bonds, gold, government securities and other asset classes.

Watch the video - What are mutual funds?

Mutual funds are managed by experienced financial professionals, also known as fund managers, who deploy the money across various asset classes in line with the respective investment objectives of these funds. Also, the decisions on when and where to make the investments rest with these fund managers.

How do mutual funds work?

Now, you are aware of what a mutual fund is. But before you know how mutual funds work and the features of mutual funds, you should first understand the NAV or Net Asset Value. You may have come across this term in ads.

What is NAV? Well, NAV per unit refers to the price at which you can buy or redeem your mutual fund investments.

Let us give you an example. Suppose you invest Rs 1000 in a mutual fund scheme where the NAV is Rs 10. Then, you will be allotted (1000/10) or 100 units of the fund.

Remember that a mutual fund's net asset value (NAV) changes daily based on the fund's underlying assets. If the underlying asset of a fund performs well, then the price of its NAV will go up and vice versa.

So, based on the above example, if the NAV of your mutual fund increases to Rs 20, then your 100 units will amount to (100 units x Rs 20) = Rs 2,000. And if you redeem your units, you will receive Rs 2,000 in return for your initial investment of Rs 1,000.

Historically, it has been observed that equity markets have consistently provided inflation-beating returns over the long term.

Unlike some popular investment avenues, such as fixed deposits (FDs), mutual funds have consistently yielded returns between 12 and 15 per cent over the last 10-20 years.

So, if you invest in an equity mutual fund and stay invested for a long time, you can grow your money several times and thus create wealth.

Explore Mutual Fund Calculator

What are the categories of mutual funds?

Mutual funds can be classified in more than one way. For instance, based on whether a mutual fund is managed by a manager, mutual funds can be classified into two broad categories.

- Actively managed funds: These are managed by an experienced fund manager. These managers hold expertise in market analysis and research. They devise the strategy of these funds in a way that helps them outperform certain index returns or benchmarks.

- Passively managed funds: These funds are not managed by a fund manager. Instead, they are designed to follow one or the other index. There are sub-categories, such as Exchange-Traded Funds (ETFs), Index Funds, or Funds of Funds (FOFs).

Similarly, all mutual funds can be broadly divided into two categories based on entry and exit restrictions.

- Open-ended funds: With open-ended funds, you can buy and sell units at any time.

- Closed-ended funds: In closed-ended funds, you can buy units only during the initial launch of these funds. Once you invest in these mutual funds, you can withdraw the amount at the time of their maturity.

What are the types of open-ended mutual funds?

Open-ended mutual funds are again classified based on their investment objectives and the underlying securities they hold. We have listed them below for your reference.

Equity mutual funds

These funds invest around 65 per cent of the assets in stocks of various companies. Given their volatile nature, equity mutual funds are mainly suitable for long-term investments (five years and more). These funds can provide better returns, but at the cost of higher risks.

Furthermore, mutual funds come in various types. The following are some popular types of equity mutual funds.

- Large-cap funds: As the name suggests, these funds invest around 80 per cent of their assets in the stocks of large-cap companies.

- Mid-cap funds: These funds invest around 65 per cent of their assets in mid-cap companies.

- Small-cap funds: They invest around 65 per cent of their assets in small-cap companies.

- Equity-linked Savings Scheme (ELSS): These are tax-saving equity mutual funds and invest around 80 per cent of their assets in stocks. ELSS schemes come with a lock-in period of three years from the date of your investments. Also, remember that with your ELSS investments, you can enjoy tax benefits under Section 80C of the Income Tax Act.

- Multi-cap funds: These funds invest in stocks of any companies, be it large caps, mid caps or small caps.

- Index funds: These types of mutual funds simply invest in all the securities of market indices. For example, you invest in an index fund that tracks the Sensex. Then, the fund will deploy your money to the same companies that are a part of the Sensex and in the same proportion.

These funds try to replicate the returns of their underlying indices closely. Unlike other funds, these funds' operating costs and portfolio turnover are quite low. - International funds: These mutual funds invest in companies listed in other countries to provide geographical diversification to investors.

Debt mutual funds

Debt funds mainly invest in fixed-income instruments, including government securities, debentures, bonds and so on. Unlike their equity counterparts, these funds are not impacted by the volatility of the stock market, and therefore, they provide more stable returns.

Debt mutual funds are classified into different types based on the maturity period of their underlying securities. Here are a few of them.

- Liquid funds: These funds invest in highly liquid instruments, such as certificates of deposits, treasury bills and commercial papers that have a maturity period of less than 91 days. Therefore, these funds are less risky. You can also park your emergency funds in liquid funds.

- Short-duration funds: These mutual funds are mandated to maintain a Macaulay duration of one to three years. Short-duration funds mainly invest in a mix of government and corporate bonds of different varieties.

- Overnight funds: As their name suggests, overnight funds invest in overnight securities or assets that come with a maturity of one day.

Hybrid mutual funds

These mutual funds invest in a mix of equity and debt instruments, based on the investment objectives of each fund. With hybrid funds, you will enjoy diversification across various asset classes. Besides, you will get capital appreciation from the equity side and capital protection from the debt side. In the Indian mutual fund market, you will find various types of hybrid funds, including the following.

- Aggressive hybrid funds: These mutual funds invest 65-80 per cent of their assets in equity and the rest in debt instruments. In addition to the mix of debt and equity, aggressive hybrid funds capitalise on arbitrage opportunities.

- Conservative hybrid funds: Unlike their aggressive counterparts, these funds allocate around 75-90 per cent of their assets to debt securities and the remainder to equity. Hence, conservative hybrid funds are more secure than aggressive hybrid funds.

- Balanced advantage funds: These funds strike a balance between equity and debt in their asset allocation. In a bid to minimise risks while maximising gains, balanced advantage funds keep changing their asset allocation based on market movements.

What are the benefits of investing in mutual funds?

- Diversification: You can bring diversification to your investments at a low cost by investing in mutual funds. For example, even if you invest Rs 500 in one fund, you will still get exposure to at least 30 stocks. Additionally, given the availability of various types of mutual funds in India, you can select products tailored to your individual investment requirements.

- Professional management: Most investors lack in-depth knowledge of the capital market. Hence, it is quite challenging for them to manage their investments independently. For such individuals, mutual funds are a great boon, as all mutual fund schemes are managed by dedicated and expert fund managers who oversee investors' funds.

- Clarity and security: When you follow the mutual fund route, you can easily get updates about the scheme you have invested in. Typically, all asset management companies provide scheme-related details, including past performance, expense ratio, the scheme's performance compared to the benchmark and category average, changes in NAV, and so on. Furthermore, the capital market regulator, the Securities and Exchange Board of India (SEBI), closely regulates mutual fund schemes. So, apart from clarity, there is also a sense of security.

- Liquidity: If you invest in open-ended mutual funds, it will be easier for you to buy and sell mutual fund schemes. However, you should consider the exit load and expense ratio of the fund.

- The power of compounding: Compounding refers to earning interest on the interest earned. For example, you have invested Rs 10 lakh in a mutual fund, which yields an interest rate of 10 per cent in the first year. So, your money would become Rs 11 lakh. In the second year, you will get returns on your initial investment, which is Rs 10 lakh and the additional Rs 1 lakh you earned in the first year.

- Affordability: Mutual funds are an investment vehicle suitable for small investors with limited investment funds.

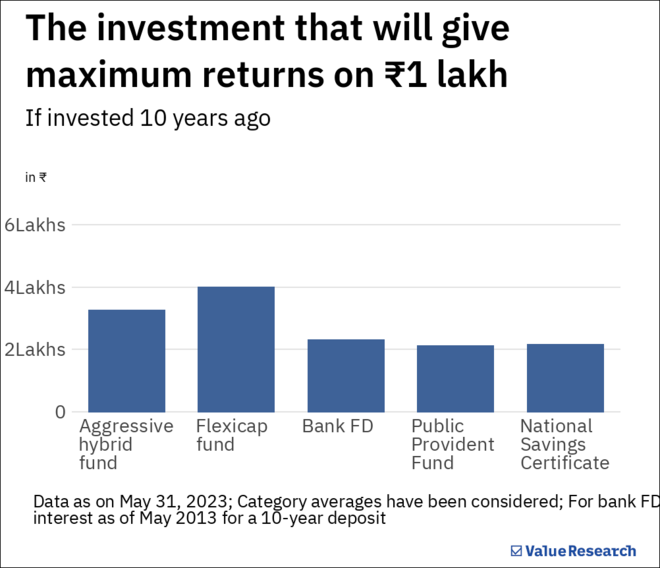

In fact, it is worth noting that among different kinds of investment instruments, two types of mutual funds outperform all other instruments, including but not limited to fixed deposits, Public Provident Funds (PPF), and National Savings Certificates (NSCs). For instance, the graph below shows how your money would have grown if you had invested Rs 1 lakh 10 years ago.

What are the disadvantages of investing in mutual funds?

- Tax for capital gains: When it comes to mutual funds, both long and short-term gains are subject to tax. However, you should be familiar with the concept of indexation to calculate your mutual fund's taxes. You must also know how the new tax regime impacts indexation benefits.

- Lock-in period: Some mutual funds, for example, ELSS, come with a lock-in period. This lock-in period is a big drawback, as you cannot withdraw your money when required before the specified time.

- Varying returns: If you invest in mutual funds, you will not get any fixed returns. Given the market volatility, your investments will be subject to a vast range of price fluctuations, including the depreciation of the value of your investments.

How to invest in mutual funds?

There are various ways through which you can invest in mutual funds. These include:

- You can invest through the website or apps of an AMC. All you have to do is to create an account on the company's website and follow the steps mentioned there.

- Another option to invest in a mutual fund is through a distributor. However, if you follow this route, your expense ratio will be higher, and your returns will be lower.

- You can also invest in mutual funds through Registered Investment Advisors (RIA) and Registrars and Transfer Agents (RTAs).

What is the KYC process in mutual funds?

KYC stands for 'Know Your Customer'. It is mainly a customer identification process conducted when opening an account with a financial entity.

Now you have the Central Know Your Customer (CKYC) facility, initiated by the government of India. This initiative enables you to accomplish the KYC process only once. So, you do not need to complete the documentation process each time you invest in a new fund.

Also, you can do your KYC through the distributor, which would also lead to documentation in CKYC.

Documents required to invest in mutual funds in India (KYC Documents)

If you want to invest in mutual funds online, you need to submit the following documents.

1. Identity proof: To verify your identity, please submit your passport, PAN card, and Aadhaar card to the fund house.

2. Address proof: To verify your address, you can submit your driving license, Aadhar card and voter's ID card to the fund house.

How to transact in mutual funds?

There are various ways to transact in mutual funds.

- SIP: A SIP is the best way to invest in mutual funds, as it allows the magic of compounding to unfold. An SIP or Systematic Investment Plan is an investment mode that allows you to invest a fixed amount periodically.

You can start the SIP with a very small amount. The auto-debit service option offered by your bank will enable you to make your investments automatically each month.

You can select different frequencies for your SIPs. It can be daily, weekly or monthly. Today, technology even enables us to invest money on specific dates of the month, and so on.

The key is to recognise that there is no best date for SIP. Instead, you should align it with your salary or earning cycle and start. You can always streamline it later.

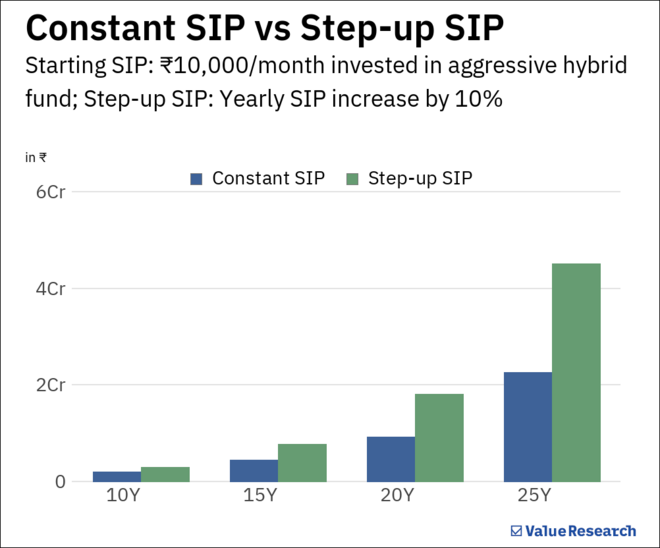

Moreover, if you continue to increase your SIP gradually as your income rises, your wealth will also start showing a significant increase over time. Let's show you what happens if you invest in an average aggressive-hybrid fund and start an SIP of Rs 10,000, increasing it by 10% every year.

- Lumpsum: It is a one-time investment where you make the entire investment in one go. This is usually not recommended for investment in equity funds. However, if you're looking to invest in debt funds for a short duration, this is not a bad investment method.

- STP: You can opt for a systematic transfer plan (STP) when you have a lump sum to invest in mutual funds and want to invest for a longer time horizon. Under an STP, you can make a lump-sum investment in one scheme (a debt scheme mainly) and transfer a specific amount regularly from this scheme to another scheme (mostly equity).

- SWP: An SWP or systematic withdrawal plan enables you to withdraw a fixed amount of money from your mutual funds at regular intervals. This mode is particularly suitable for retirees seeking a steady income stream.

What are the various mutual fund fees and charges?

- Expense ratio: For a fund's management, the fund house charges an annual maintenance fee, known as the expense ratio. This ratio varies from one fund to another. However, the market regulator has set a maximum limit to this fee.

- Entry load: This fee is charged when you initially invest in a mutual fund scheme. The amount will be deducted from the Net Asset Value (NAV).

- Transaction charge: This is a one-time token amount levied on you throughout your entire investment period. Fund houses can charge a transaction fee of Rs 100 for their existing investors and a transaction fee of Rs 150 for new investors if the worth of the investment is Rs 10,000 and above. Nevertheless, you will not be charged any transaction fee if the value of your investment is less than Rs 10,000.

- Exit load: If you exit a mutual fund scheme within a short time, then you will be charged an exit load. Exit loads are also referred to as redemption fees. An exit load is charged to discourage you from withdrawing your funds prematurely. This fee enables fund houses to minimise the volume of withdrawals.

Some common terms related to mutual funds

- NAV - Net Asset Value: It denotes the total sum of the market value of all the shares in a portfolio. So, we can say that NAV is the 'book value' of a unit.

- AMC - Asset Management Company: An Asset Management Company (AMC) indicates a fund house that collects funds from individual investors and invests it in different asset classes, including debt, equity, cash and so on.

- AUM - Asset Under Management: It refers to the total market value of all the assets, comprising bonds, securities and stocks, managed by a fund house on behalf of their investors.

- NFO - New Fund Offer: The NFO is a subscription offer provided by the AMC to start a new fund category.

- ETF - Exchange Traded Fund: An ETF is an open-ended mutual fund scheme that tracks and follows its underlying index's performance.

- ELSS - Equity-Linked Savings Schemes: ELSS funds, a type of mutual fund, are the ones that are eligible for tax deductions under Section 80C of the Income Tax Act.

- RTA - Registrar and Transfer Agents: They help mutual fund companies maintain records. They provide investors with a one-stop reference for all information related to their investments in mutual funds.

- SIP - Systematic Investment Plan: As mentioned above, this investment mode enables investors to invest a fixed amount regularly at a fixed frequency.

- STP - Systematic Transfer Plan: As already discussed, under the STP, you can transfer a specific amount regularly from one scheme (where you have made a lumpsum investment) to another scheme.

- SWP - Systematic Withdrawal Plan: You can withdraw a fixed amount of money from your mutual funds at regular intervals by opting for the SWP mode.

FAQs:

Q. Do you need different bank accounts to invest in different mutual funds?

A. You do not need to have several accounts to be able to make investments in different mutual funds. With only one bank account, you will be able to invest in and redeem from different mutual funds.

Q. What details do scheme-related documents provide?

A. You must have come across the disclaimer that reads the scheme-related documents carefully before investing in mutual funds. The main objective of this message is to inform investors about their mutual fund investments. And this much-needed information comes from the scheme-related documents orthe SID of every mutual fund scheme. These documents provide all the details about the scheme, including its investment objective, asset allocation, risks associated with the particular scheme, investment style, and more.

Q. What happens if one misses the SIP payment in between?

A. As we have discussed earlier, mutual funds are a long-term investment avenue. Given this, it is fine if you miss a SIP instalment. You will not be penalised for that. However, remember that if you miss your SIP payments for three consecutive months, your SIP in that mutual fund scheme will be cancelled automatically.

Q. How to invest in mutual funds based on individual goals?

A. Various categories of mutual funds are meant for different investment goals and time horizons. For example, if you want to plan a foreign trip with your family in 2024, it will be your short-term goal. On the other hand, if you want to save for your retirement, which is 15 years away, then it would be your long-term goal.

Pick a mutual fund based on your goal. For your short-term goals, you can invest in debt funds. However, if your goals are at least five years away, opt for equity or equity-oriented mutual funds.

Q. What are the differences between growth vs dividend mutual funds?

A. You will get two options while investing in mutual funds. In the first option, a portion of your mutual fund gains will be given to you at regular intervals. In the second option, all your investment gains will be reinvested in the scheme.

The first option is known as 'Income Distribution cum Capital Withdrawal (IDCW)/ plans, while the second one is known as growth plans. Growth plans are considered better than IDCW plans, as they will allow your investments to grow further and at a faster pace.

Q. What is the difference between active and passive mutual funds?

A. Actively managed funds intend to outperform their respective benchmark indices with the help of their expert fund managers. On the other hand, passive funds aim to replicate the performance of an index.

Expense ratios of passive funds tend to be lower than their active counterparts. The reason is simple. They have lower costs, with passive funds requiring less management, trading, and results.

Q. What are the taxation rules in mutual funds?

A. Like any other type of income, your mutual fund gains are also subject to tax. However, in the case of mutual funds, three factors determine how much tax you need to pay. These include:

- The type of mutual fund you have invested in: When it comes to mutual funds in India, equity-oriented funds and non-equity-oriented funds are taxed differently.

- The holding period of your investments: Your holding period can be long-term or short-term. If you invest in an equity-oriented fund and hold it for more than a year, then your gains will be considered long-term capital gains. On the other hand, if you hold it for less than a year, then it will be considered as short-term capital gains.

- In the case of non-equity-oriented funds, if you invest in such a fund and hold it for more than three years, then your gains will be considered long-term capital gains. But if you hold it for less than three years, it will be considered short-term capital gains.

- Your tax slab: If you invest in a non-equity fund or opt for IDCW plans of mutual funds, then your tax slab will be considered.

Q. What happens to mutual fund investments after the death of the unit holder?

A. Several provisions ensure that a nominee (s) can claim the mutual fund units of the deceased investor. Three kinds of claimants can be eligible for the units of the deceased.

1. Joint account holders

2. Legal heirs

3. Nominees

When transferring units of the deceased investor to the claimant, the procedure is nearly identical. However, based on the types of claimants and mutual fund holdings, there may be some differences in the process and documentation.

Q. Who regulates mutual funds in India?

A. The Securities and Exchange Board of India (SEBI) regulates all mutual funds in India. Before investing in any mutual fund scheme, it is essential to check the rules and regulations set by SEBI.

Suggested read: What are mutual funds?

This article was originally published on September 13, 2023.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()