"Can I invest a lump sum of Rs 10 lakh in an aggressive hybrid fund since it is not a pure equity fund?", asked one of our readers.

Investors often ask this question because they consider SIPs essential only for equity funds and assume that the benefit of rupee-cost averaging applies only to these funds. However, it is crucial to understand that SIPs are important for equity funds and equity-oriented funds. To understand why, let us quickly look at how aggressive hybrid funds work in the first place.

Aggressive hybrid funds or equity-oriented hybrid mutual funds

An aggressive hybrid fund invests in both equity and debt securities. However, their allocation in equity and related instruments is higher (65-80 per cent) than in debt instruments. In other words, they come under the category of equity-oriented funds.

While the equity-debt mix helps them bring high returns and stability, the reality is that they are subject to market risks as well.

Understanding the impact of the market on aggressive hybrid funds

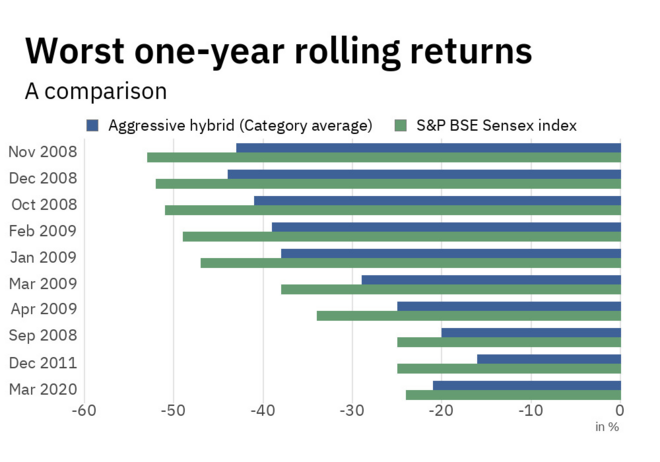

For instance, this graph illustrates the 10 worst one-year rolling returns of the Sensex vs aggressive hybrid funds. There are two things to notice here.

Firstly, it is evident that these funds, despite being equity-oriented, have weathered the equity market downturn better due to their debt component. This aspect provides a cushion, resulting in smaller losses than pure equity funds, like the Sensex index fund.

More importantly, this graph indicates how you can experience huge losses if you time your lump sum wrong. In this scenario, if you had invested a lump sum of Rs 1 lakh just a year before March 2020, you would have suffered a 21 per cent loss over the year, leaving you with just Rs 79,000. This is why investing the entire sum at once rarely makes sense.

What's the alternative?

This is where SIP investing steps in.

They can shield your investments from short-term market fluctuations and thus protect you from risk. SIPs ensure that you do not invest a significant sum during a market high and then suffer from a subsequent fall.

Investing through an SIP allows you to invest only a portion of your money, albeit regularly, irrespective of the market conditions. As a result, when market prices are high, fewer units are purchased, and when prices are low, more units are bought.

In the longer run, your investment ends up with an average purchase cost, thus reaping the benefits of a disciplined approach to investing. This is commonly known as 'rupee cost averaging'.

The timeline

Now you know you shouldn't invest a large sum of money all at once. Instead, you should opt for an SIP.

The only question is - how much time should you take to invest this money?

An efficient way of calculating your investment timeline is to calculate the time it took you to accumulate these funds. Ideally, you should invest this money in half that time. However, it is recommended that you invest this money in not more than three years. Three years is a good time to go through an entire market cycle and capture both the market rise and fall.

Beyond this timeline, there isn't any real advantage to staggering your investment. In fact, a major downside to a longer timeline is that you may be tempted to spend this money.

Our take

Do not invest a large sum all at once. Instead, always plan an SIP.

To calculate the timeline for your SIPs, consider the following:

- How large is this sum?

- How important and valuable is this money for you?

- How much time, effort, and energy went into accumulating it?

- Invest the money over a shorter duration if you have a higher income.

- Or, if your risk appetite is low, invest this money over a slightly extended period.

Do not take more than three years to invest your lump sum.

The key to your wealth, dear reader, is always in disciplined investing!

Suggested watch: SIP vs lump sum investing in mutual funds

Also read: Why SIPs score over lump sum investments

This article was originally published on June 09, 2023, and last updated on October 08, 2024.

Ask Value Research ![]()