We, as Indians, love our fixed deposit (FD) investments as they are safe and offer steady returns. Even for the more adventurous investors, there are times when the safety of capital takes priority. Looming retirement, economic uncertainty or even recession fears are some such instances. But what if I told you there is a better and safer option than an FD?

Say hello to government securities.

They are safer because countries guarantee interest and repayment of the original investment. A whole country would have to crumble for you not to receive your investment!

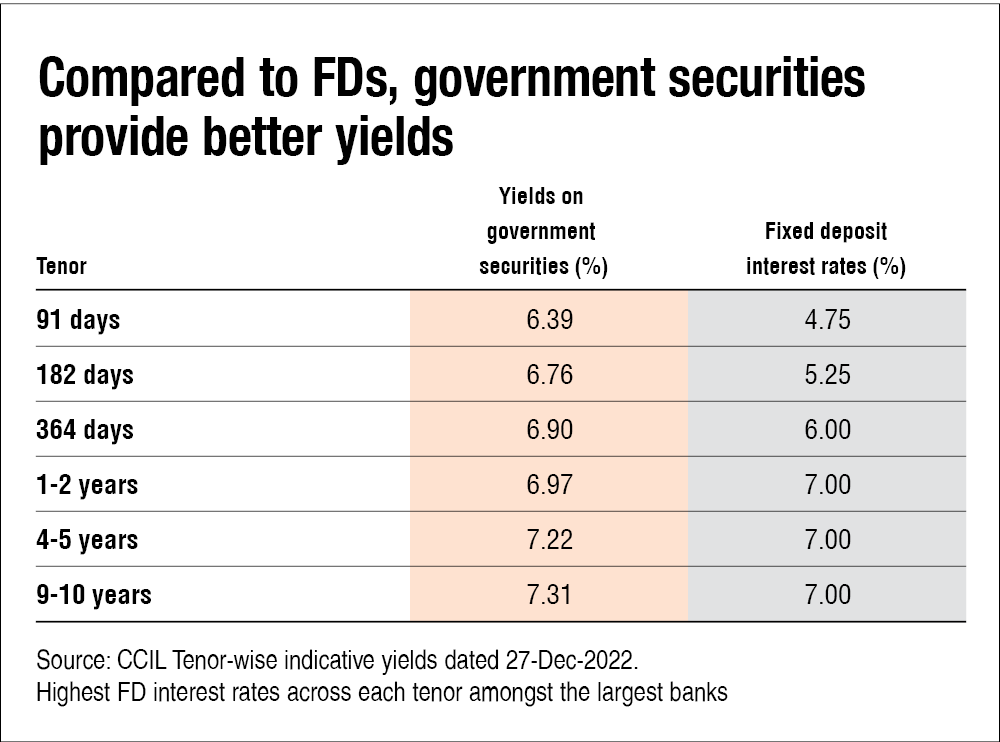

They are better than FDs because they offer higher yields (returns), as shown in the table below.

Clearly, government securities have the edge over FDs.

How to invest in government securities

Liquid and short-duration mutual funds do invest in government securities. You can check the 'Analysts' Choice' section to get a list of the best liquid and short-duration funds.

But if you want to play it very safe and want a higher allocation in government securities, you have three options:

Gilt funds

Yield-to-maturity (Expected returns if you invest now and hold it till maturity)

6.09 per cent - 7.68 per cent

- These funds are yielding as high as 7.68 per cent at the moment. But this can be viewed as a negative because even though you are investing for a longer duration, the returns are similar to that of a short-duration fund. (Ideally, you should receive a higher yield if you stay invested for a longer period).

- The average maturity of these funds range from 1.84 to 10.34 years. This is the length of time after which you are paid back your principal amount (the original investment).

- These funds are also volatile. A bit like equities. You can read more about it here.

- They charge a high expense ratio. Some funds charge as much as 1 per cent, and the average is 0.5 per cent. This means your overall returns will be below or barely at par with FDs.

- They don't provide any clear tax advantage. You need to pay capital gains tax on exiting the investment.

RBI Retail Direct

Yield-to-maturity (Expected returns if you invest now and hold it till maturity)

6.39 per cent - 7.69 per cent

- The average maturity of the securities available on this platform range between 91 days and 30 years. This is the length of time after which you are paid back your principal amount (the original investment).

- The RBI Retail Direct platform allows retail investors to directly invest in government securities. This way, you can avoid the cost of paying an intermediary/distributor/middleperson.

- While they are cost-efficient, you should take this route only if you know which government securities to pick.

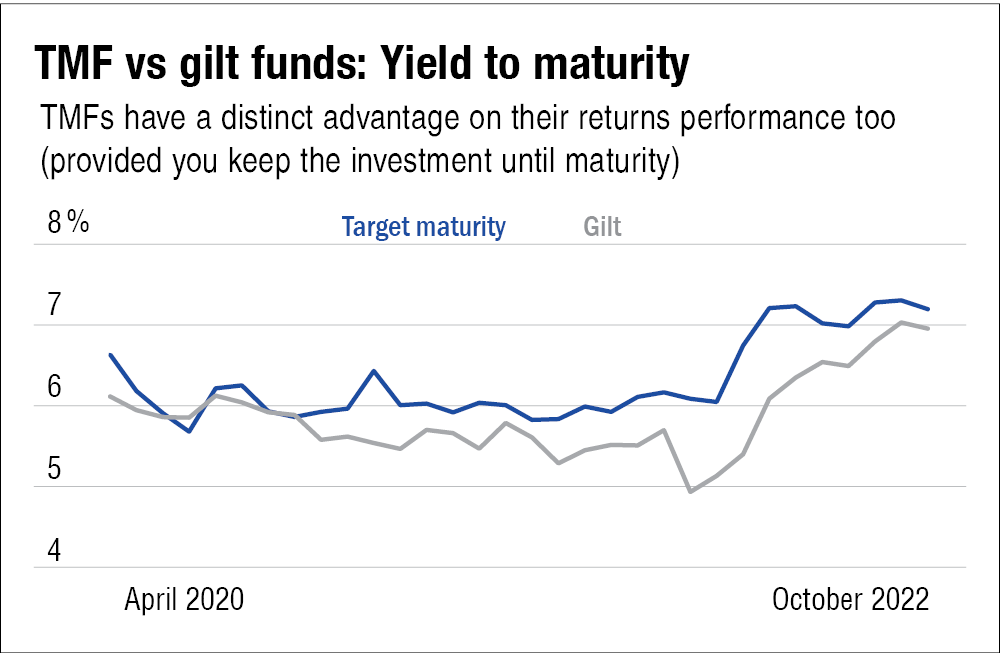

Target-maturity funds (TMF)

Yield-to-maturity (Expected returns if you invest now and hold it till maturity)

7.01 per cent - 7.7 per cent

What they are

These funds buy and hold securities with maturities similar to the tenure of the fund. So, if one of these funds has a seven-year maturity, it would invest in securities that also mature in and around the seven-year mark.

These funds also give certain predictability of returns if you hold the fund until maturity. So, if a TMF says it will provide 8 per cent returns after seven years, you can expect to get that percentage of returns if you hold the investment for seven years.

- These funds invest in government securities and bonds with the highest credibility.

- The average maturity period is between 0.34 and 13.6 years. This is the length of time after which you are paid back your principal amount (the original investment).

- These are passive funds, meaning they have a lower expense ratio than gilt funds.

Average expense ratio of gilt funds: 0.29 per cent - 1.08 per cent

Average expense ratio of TMF: 0.04 per cent - 0.23 per cent - Performance-wise, TMFs have their noses ahead of gilt funds, and are also more predictable.

What you should do

- Target-maturity funds and RBI Retail Direct are better investment options than gilts.

- Choose the RBI Retail Direct option if you know which securities to invest in. If not, go for target-maturity funds.

- Above all, they are a better and safer option than FDs.

Suggested read: Gold burns bright

Ask Value Research ![]()