Promoted by KDDL (a manufacturer of watch components), Ethos is one of India's largest luxury and premium watch retailers. The company retails 50 premium and luxury watch brands, including Omega, Rolex, Panerai, Bvlgari, Rado, Longines, and Tissot. The company also undertakes retail of certified pre-owned luxury watches. It has 50 retail stores in 17 cities across the country. It also retails actively through its website. Ethos also has a loyalty programme called Club Echo, with over 2.8 lakh registered members as of March 2022.

The premium and luxury watch market comprises the segments High Luxury (Rs 10 lakh and above), Luxury (Rs 2.5 to Rs 10 lakh), Bridge to Luxury (Rs 1 to Rs 2.5 lakh), and Premium watches (Rs 25,000 to Rs 1 lakh). In FY21, the company generated 39 per cent, 19 per cent, 18.8 per cent, 17.6 per cent and 5.6 per cent of revenue from Luxury, High Luxury, Bridge to Luxury, Premium and Fashion segments, respectively. The company's 50 stores are categorised into 14 Ethos Summit stores (flagship stores) and one Airport store, 14 multi-brand outlets and 10 Ethos Boutiques (partnerships with prominent brands).

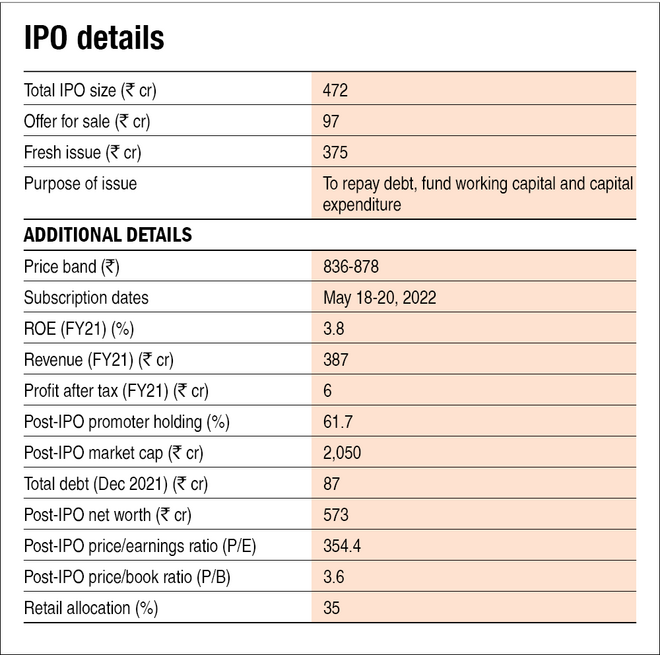

Ethos has one of the largest store networks and the highest number of premium and luxury brands available on its website. Also, it offers the highest number of stock-keeping units across all three luxury segments. The company has undertaken a pre-IPO placement of Rs 25 crore for Rs 826 per share. As a result, the size of the fresh issue has been reduced from Rs 400 crore to Rs 375 crore. The luxury and premium segment of the watch market was valued at around Rs 6,610 crore in FY20 and is expected to grow at a CAGR of 12.5 per cent to Rs 11,890 crore by FY25.

Strengths

1. Leading market share among vertical specialist MBOs: As of FY20, Ethos had a 13 per cent market share of the total retail sales in the premium and luxury watch segment. However, in the luxury segment alone, the company had a market share of 20 per cent. This makes it the largest retailer in premium and luxury watch retail in India. The company also leads the luxury omnichannel market in India, with a wide omnichannel presence and focus. In FY21, 37.6 per cent of Ethos' revenue came from digitally-enabled sales.

2. Access to a large customer base: As of March 2022, the company had access to an HNI customer base of over 2.8 lakh through its loyalty programme, Club Echo. Around 35 per cent of annual business comes from repeat buyers enrolled in the loyalty programme. As the company's products are highly discretionary, the demand is directly proportional to the number of HNI customers.

3. Long-standing relationships with luxury watch brands: Ethos has had business partnerships with some brands for more than a decade. Watch brands control distribution through strict agreements. They control and closely monitor which products are sold and how they are presented. Moreover, to preserve the exclusivity of luxury watches and avoid excess supply, watch brands don't simply give away the business to other players. These relationships take many years to develop, and Ethos has benefitted from its promotor, KDDL's relationships with these luxury brands.

Risks/weaknesses

1. High working capital requirements: The company funds most of its working capital requirements through borrowing and internal accruals. As part of the company's business, it is required to buy watches and pay lease rent for stores. Moreover, with the proposed increase in the number of stores, the company will need more inventory. Therefore, the working capital required to conduct the business would increase. By the company's estimation, its working capital will increase by 62 per cent from FY21 to FY22, 60 per cent in FY23 and 38 per cent in FY24.

2. Lease renewals and foreign exchange risks: All 50 retail stores of the company are taken on lease or contractual agreements with either third parties or promoters. Any failure to renew these leases on competitive terms would adversely impact the company's operations. Ethos deals in Swiss Franc, US dollar, British Pound and other foreign currencies. It does not enter into any hedging arrangements and could be exposed to foreign exchange risks.

3. Increase in import duties: Ethos' business is dependent on its ability to source imported products from its suppliers. Therefore, any increase in import duties would negatively impact the company's margins.

Also read Ethos IPO: How good is it? to learn how we evaluate the company on various metrics.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()