A common query that many people have is why they shouldn't be investing a lumpsum in equities. The question is quite pertinent specifically for self-employed individuals. Unlike salaried, they don't have a fixed and known stream of money coming in every month. That's one reason why many of them usually prefer investing a lumpsum as and when they have a surplus instead of committing a fixed amount through an SIP.

But that's certainly not the recommended way. Even if you are not willing to make a commitment, stagger your lumpsum over a period of time through a systematic transfer plan (STP). You can also put the lumpsum in a bank account and initiate only as many SIPs as are sufficient to invest that lumpsum amount of money over a period of time.

When we invest in a staggered manner, we average the cost of purchase and reduce the risk of investing at a market high. Moreover, equities are unpredictable and extremely volatile over the short-term. If the market crashes soon after making a lumpsum investment, it can make you anxious and you might redeem your money out of panic, making the losses permanent.

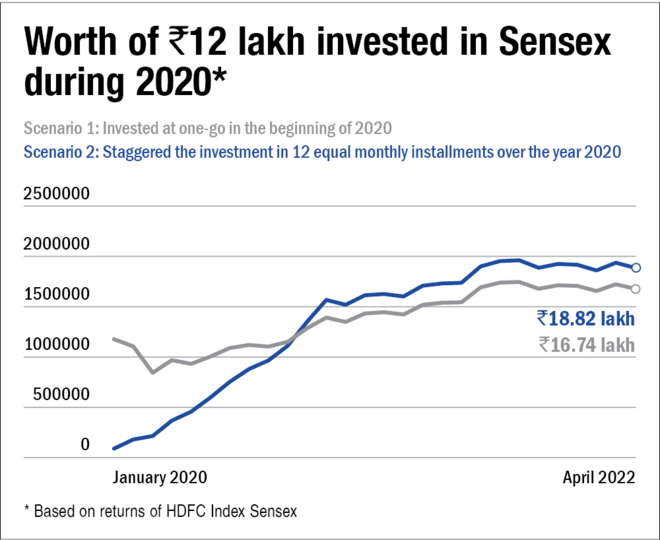

Let us look at an example. Let's say you had a lumpsum of Rs 12 lakh at the beginning of 2020 and chose to invest it at one go in an index fund tracking the Sensex. Just a couple of months after, in March, the market crashed due to COVID. The worth of your investment would have fallen to Rs 8.56 lakh. That is a loss of about Rs 3.44 lakh in three months. A very disheartening number and one is bound to panic and get anxious in such a scenario. Investors usually redeem their money at this stage with the intent of saving whatever is left, making their losses permanent.

Now let's consider another scenario, where you chose to break this money into 12 equal monthly installments through an SIP or an STP. By the end of March, you would have invested only Rs 3 lakh and may not have been as anxious about the market crash. Further, since now you would be investing in a fallen market, you would be buying cheap and likely to get a higher benefit over the longer-term. Watch Lumpsum vs SIP.

Even if someone, after investing a lumpsum in January, would have stayed invested throughout the market crash, he would be having a lesser corpus right now in comparison to someone who would have chosen the staggered approach. By the end of April 2022, the worth of his 12 lakh would have appreciated to Rs 18.82 lakh in comparison to Rs 16.74 lakh of the person who would have invested at one go. That's because by staggering the investment, he was able to buy cheap during the market crash and reduce his cost of purchase by averaging.

Suggested read: Why SIPs score over lump sum investments

This article was originally published on May 09, 2022.

Ask Value Research ![]()