Sansera Engineering came out with its IPO five months ago. You can read our detailed analysis about the issue here. In this update, we will look at the company's market performance and business performance post-IPO.

Our analysis of the IPO

Sansera Engineering is involved in the business of manufacturing complex and critical precision engineering components. These components are used in both automotive and non-automotive industries. For the automotive segment, the company manufactures connecting rod, which generates 39.6 per cent of revenue, rocker arm, which generates 19.5 per cent of revenue, the gear shifter, which generates 6.6 per cent of revenue, and stem comp and aluminium forged parts which generate 3.8 per cent of revenue. In the non-automotive segment, they manufacture precision components for aerospace, off-road, agriculture, etc. As of FY21, the automotive segment contributes 88 per cent of revenue (83 per cent from Auto-ICE and 5 per cent from auto-tech agnostic & EV), and the non-automotive segment contributes 12 per cent of revenue.

Based on Sansera Engineering's long-standing relationship with customers, leadership in manufacturing connecting rods and integrated operations, we gave it a rating of 17 out of 27. Some of our major concerns regarding the issue were its customer and product concentration. It derives 45 per cent of revenue from the top three customers, and the connecting rod generates around 40 per cent of revenue. Any change in contract or demand for components may hurt the company.

Our rating of the company was based on the following factors:

- Out of 10 business metrics, the company did well only on five.

- Sansera Engineering did well on all six management-related metrics.

- Out of eight financial metrics, the company did well on four.

- Out of three valuation-related metrics, it did well on two.

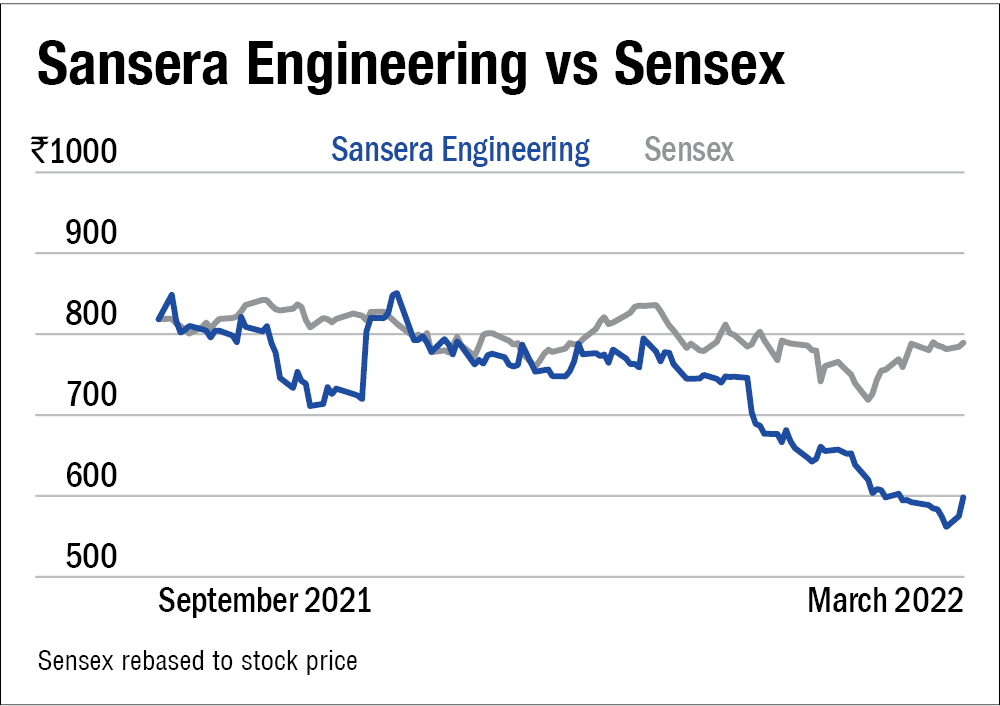

Stock performance since listing

Sansera Engineering received a good reception from investors, especially from institutions. The issue was subscribed 11.5 times in total. The institutional portion was subscribed 26.5 times, the high net worth individuals portion was subscribed 11.4 times, and the retail portion was subscribed 3.2 times.

Thanks to a decent reception from investors, the shares listed at Rs 811, 11 per cent above the issue price. But after the first three weeks of listing, the gains were wiped out as the stock started to fall. At present, the stock trades at Rs 630, 22 per cent down from its list price, and poor Q3 results only accelerated the fall.

Business performance

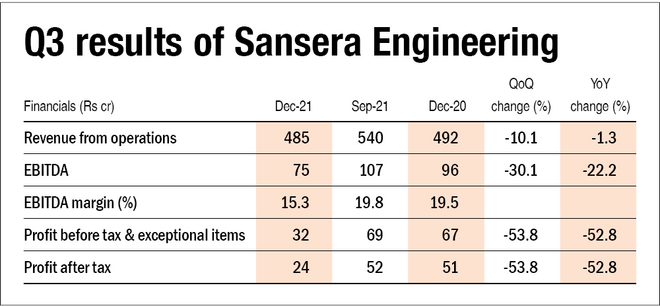

The company posted rather unimpressive Q3FY22 results. Its revenue from operations, EBITDA and profits decreased by 1, 22, and 53 per cent YoY, respectively. This was mainly led by increased employee cost, interest expense, depreciation and inventory. But on a nine-month basis, the company has performed well as their revenue, EBITDA and profits increased by 33, 34 and 51 per cent, respectively.

Despite its poor performance, the management is optimistic about the future. The company acquired several customers and actively set up a dedicated facility for manufacturing hybrid and electric components within its existing Bangalore plant. Preetham, Sansera Engineering's CEO, has said that they want to expand and diversify the revenue base. In the long term, the company aims to achieve 60 per cent from auto ICE, 15 per cent from auto-tech agnostic & EV, and 15 per cent from the non-auto segment.

What to do now?

One of the reasons why investors and analysts were interested in this company was not only because of its leadership in various auto components but also its customer relationship. The company has been associated with Bajaj for 25 years, Honda and Yamaha for 20 years, and Maruti Suzuki for 30 years. It proves their expertise and experience, which is needed in this industry.

Sansera Engineering currently trades at a price to earnings of 30.2 times and a price to book of 3.4 times, which is less than many of its peers and even its own listing valuation. Although the current price level seems attractive, recent business performance has not been encouraging. Investors can closely watch this company's near future performance and do their due diligence before considering investing.

Disclaimer: This analysis is not meant to serve as a recommendation. Do your research before investing in the company. If you are interested in our stock recommendations, please visit Value Research Stock Advisor.

Also read:

Sansera Engineering IPO: Information analysis

Our other recent IPO updates:

LatentView Analytics - IPO update

One97 Communications (Paytm) - IPO update

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()