In the first part of this series, we explored the usability of the new RBI Retail Direct portal. Here, we will compare it with the alternatives available that can substitute investing in G-secs directly through the RBI Retail Direct portal.

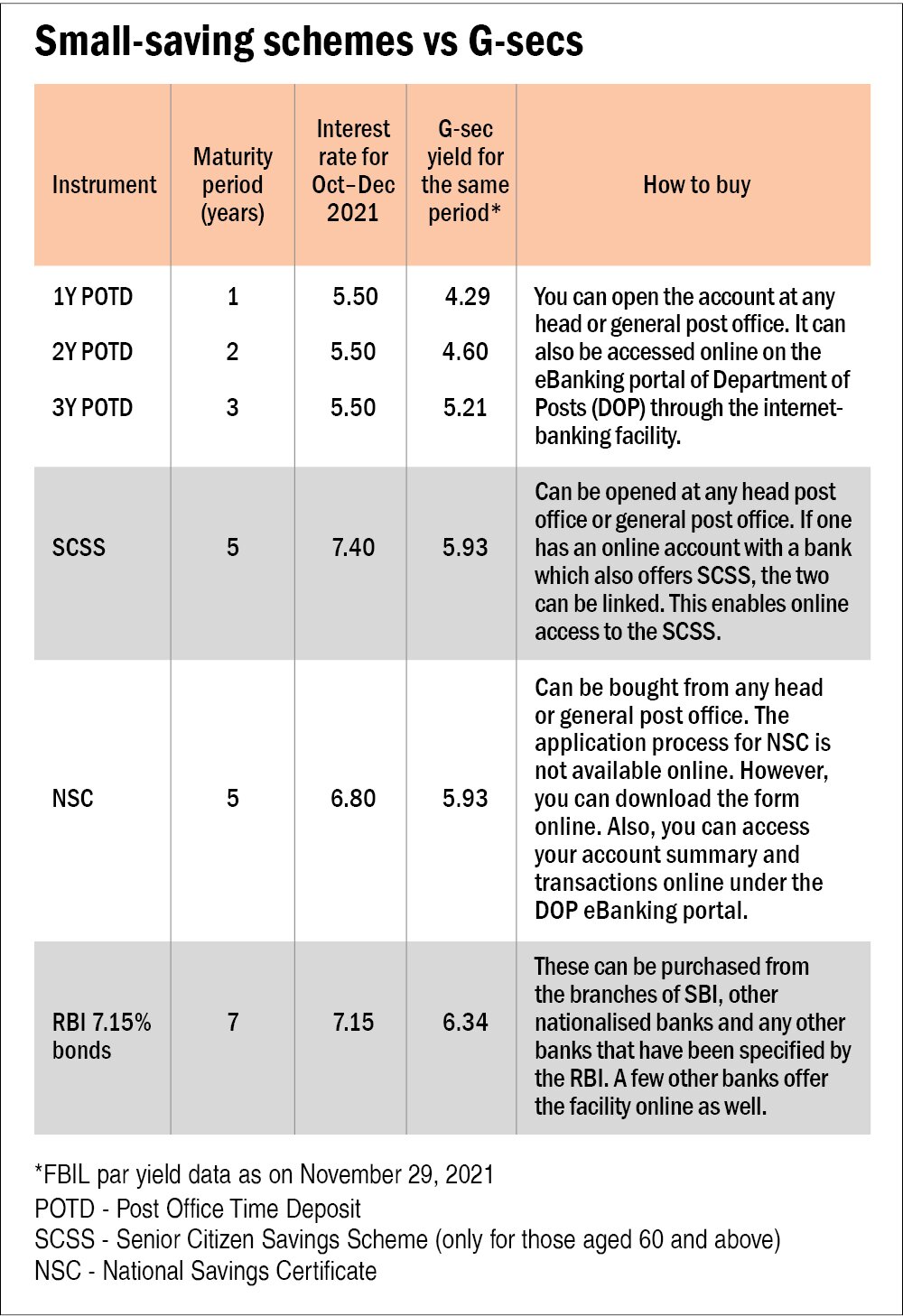

Small-saving schemes

By investing in government bonds, you are effectively lending to the government. The same goes for your investments in small-saving schemes. Given the government backing, both RBI Retail Direct and small-saving schemes are similar on the risk profile. However, the interest rates offered on small-saving schemes are pretty attractive if you look at the overall fixed-income domain. So, if liquidity is not a big concern for you, then these schemes definitely have an upper hand.

The table 'Small-saving schemes vs G-secs' gives a comparison of the interest rates offered by a few of these small saving schemes vs the same tenured government bonds. The table also mentions where you can buy these small-saving schemes.

Gilt funds

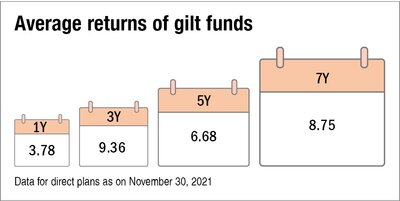

Gilt mutual funds are one of the prominent avenues of investing in G-secs. When you invest in a gilt fund, you need to pay tax only when you sell. Till then, your returns keep accumulating. Now, if you sell a fund after three years, the gains get taxed at 20 per cent post indexation. Indexation, i.e., adjusting your gains against inflation, lowers your tax outgo.

However, in the case of government bonds, interest is added to your income and taxed at your slab. So, for investors who fall under the higher tax brackets, this avenue may be quite inefficient. If the investor sells the bond after one year, it will attract long-term capital-gains tax at the rate of 10 per cent.

So, the tax arbitrage offered by debt funds tilts the scale towards gilt funds compared to directly investing in government bonds. Having said that, one can't ignore the expenses associated with bond funds, more so in a low-interest rate regime.

Also, the returns of gilt funds are not predictable unlike directly holding G-secs. Target-maturity funds overcome these problems.

Target-maturity funds

These are a relatively new type of mutual funds which come with a fixed tenure and at the end of it, the money, along with the accumulated gains, is returned to investors. There is no active management here as the fund manager simply buys and holds securities with maturities similar to the term of the fund. So, here you have an idea of your indicative annualised returns over the entire holding period of the scheme.

These funds appeal to those investors who want to invest for a fixed tenure that matches with that of a fund, with some degree of returns visibility. If you stay put for the entire tenure of a target-maturity fund, the intermittent interest-rate risk gets contained to a large extent. The underlying investments in the current bouquet of target-maturity funds ranges from G-secs, state-development loans and PSU bonds. Thus, the default risk is low here. The net ongoing yields (as of October 31, 2021) of some target maturity funds of residual maturities ranging from 1.5 to 9 years is 4.8-6.8 per cent.

On the taxation front as well, these score over direct ownership of bonds since they are taxed just like regular debt funds. Even their expense ratios are quite low.

Conclusion

While Retail Direct is a great initiative and opens up an interesting avenue for retail investors, it's entirely optional. It also requires a higher degree of digital sophistication. If you are keen on investing in G-secs, you do have other options like small-savings schemes, gilt funds and target-maturity funds. These have their own advantages which are too attractive to ignore.

Ask Value Research ![]()