In the story, An essential guide to National Pension System (NPS), we learnt about the various aspects of NPS. In this story, we will read about some other pension schemes which are backed by government.

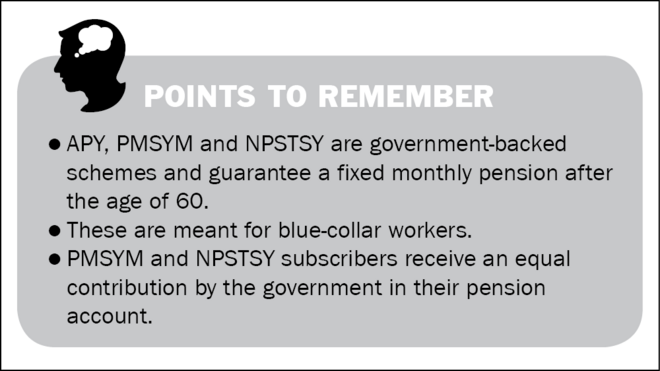

Atal Pension Yojana (APY) and the newly launched Pradhan Mantri Shram Yogi Maan-dhan (PMSYM) and National Pension Scheme for Traders & Self Employed Persons Yojna (NPSTSY) are pension-oriented savings schemes focused on people in the unorganised sector. PMSYM was launched in the Budget 2019-20 (I) followed by NPSTSY (also called Pradhan Mantri Karam Yogi Maan-dhan Scheme) in the second Union Budget 2019-20 after the Lok Sabha elections. On the other hand, APY was launched in 2015. Under all these schemes, people aged 60 or above are eligible for the pension.

Aimed at bringing retail traders, small shopkeepers and self-employed persons under an organised pension system, NPSTSY scheme offers pension benefits to around three crore beneficiaries with an annual turnover of less than Rs 1.5 crore. Apart from the eligibility criteria, both PMSYM and NPSTSY are similar to each other. However, you can take benefit only under one of the two schemes.

Some insights into APY, PMSYM and NPSTSY are as follows:

ATAL PENSION YOJANA

Investment objective and risks

The main objective of APY is to provide a fixed amount of pension to unorganised-sector workers who find no coverage under other social-security schemes.

Capital protection

The benefit of minimum pension is guaranteed by the Government of India.

Entry age

The minimum age of joining APY is 18 and the maximum age is 40.

Liquidity

Voluntary exit before 60 years is permitted under this scheme. However, in the case of a voluntary exit, only the contributions made by the subscriber are returned with an accrued income. All other contributions, comprising the government contributions and the income accrued on it, are withdrawn. However, if the beneficiary dies, the spouse can still continue with the scheme and upon the death of both the contributor and his/her spouse, the nominee will be given the accumulated corpus.

Suitability and alternatives

- Suitable for blue-collar workers looking for a guaranteed pension at a negligible contribution.

- Not suitable for investors with a higher income who can afford to invest a higher amount.

- Alternatives are Pradhan Mantri Shram Yogi Maan-dhan and National Pension Scheme for Traders & Self Employed Persons Yojna.

Guarantees

APY guarantees a minimum fixed pension to the subscriber after the age of 60. This pension amount varies from Rs 1,000 to Rs 5,000, depending on the contribution made by the subscriber. The contribution amount is calculated based on the entry age and the minimum guaranteed pension that the subscriber decides to receive. For example, an 18-year-old choosing to get a minimum pension of Rs 1,000 would have to contribute Rs 42 per month. However, if he joins at the age of 40, he will have to contribute Rs 291 every month to get a guaranteed pension of Rs 1,000 after the age of 60. The government also made a co-contribution of 50 per cent of the total contribution, or Rs 1,000 per annum, whichever is lower, to all eligible subscribers who had joined between June 2015 and December 2015 for a period of five years i.e., for financial years 2015-16 to 2019-20.

How to open the account

Many nationalised and private banks offer the APY. The subscriber needs to have a bank account and an Aadhaar card. Also, the Aadhaar card needs to be linked to the bank account.

PRADHAN MANTRI SHRAM YOGI MAAN-DHAN AND NATIONAL PENSION SCHEME FOR TRADERS & SELF EMPLOYED PERSONS YOJNA

Investment objective and risks

Pradhan Mantri Shram Yogi Maan-dhan (PMSYM) and National Pension Scheme for Traders & Self Employed Persons Yojna (NPSTSY) assures a fixed monthly pension of Rs 3,000 after the age of 60 at a negligible contribution. The main objective of these schemes is to provide guaranteed pension to the workers of the unorganised sector who are not covered by any other social security scheme. However, the PMSYM scheme is available only for those whose monthly salary is not more than Rs 15,000 and the benefit of NPSTSY can be availed only if the annual turnover does not exceed Rs 1.5 crore.

Capital protection

The benefit of a minimum pension is guaranteed by the Government of India.

Entry age

The minimum age of joining PMSYM & NPSTSY is 18 years and the maximum age is 40 years.

Liquidity

Under these schemes, voluntary exit before 60 years is permitted. However, in the case of a voluntary exit within a period of less than ten years from the date of joining the scheme, only the contributions made by the subscriber are returned with the interest equivalent of a savings account. In case the subscriber exits after completion of a period of ten years or more but before his age of sixty years, then his contributions are returned with the interest equivalent of a savings account or accumulated interest thereon as actually earned by the Pension Fund, whichever is higher. All other contributions, including government contributions and the income accrued on it, are withdrawn. If the beneficiary dies during the receipt of the pension, the spouse of the beneficiary shall be entitled to receive 50 per cent of the pension. However, if the beneficiary dies before the age of 60, the spouse can still continue with the scheme.

Suitability and alternatives

- Suitable for blue-collar workers looking for a guaranteed pension at a negligible contribution.

- Not suitable for investors with a higher income who can afford to invest a higher amount.

- Alternative is Atal Pension Yojana.

Guarantees

These schemes guarantee a fixed monthly pension of Rs 3,000 from the age of 60. The monthly contribution would vary from Rs 55 to Rs 200, depending on the entry age to guarantee a pension of Rs 3,000. For example, anyone entering at the age of 18 will have to contribute Rs 55 per month. If he joins at the age of 40, he will have to contribute Rs 200 per month. Under both the schemes, the subscriber also receives a guaranteed contribution of the equal amount by the government. For example, if an 18-year-old subscriber is contributing Rs 55 per month, another Rs 55 will also be contributed to his account by the government.

How to open the account

The beneficiary needs to visit the nearest Customer Service Centre (CSC), along with his Aadhaar card and bank account details. Once the beneficiary is enrolled and the first installment is paid, the monthly contributions can be put on auto-pilot through the ECS mandate.

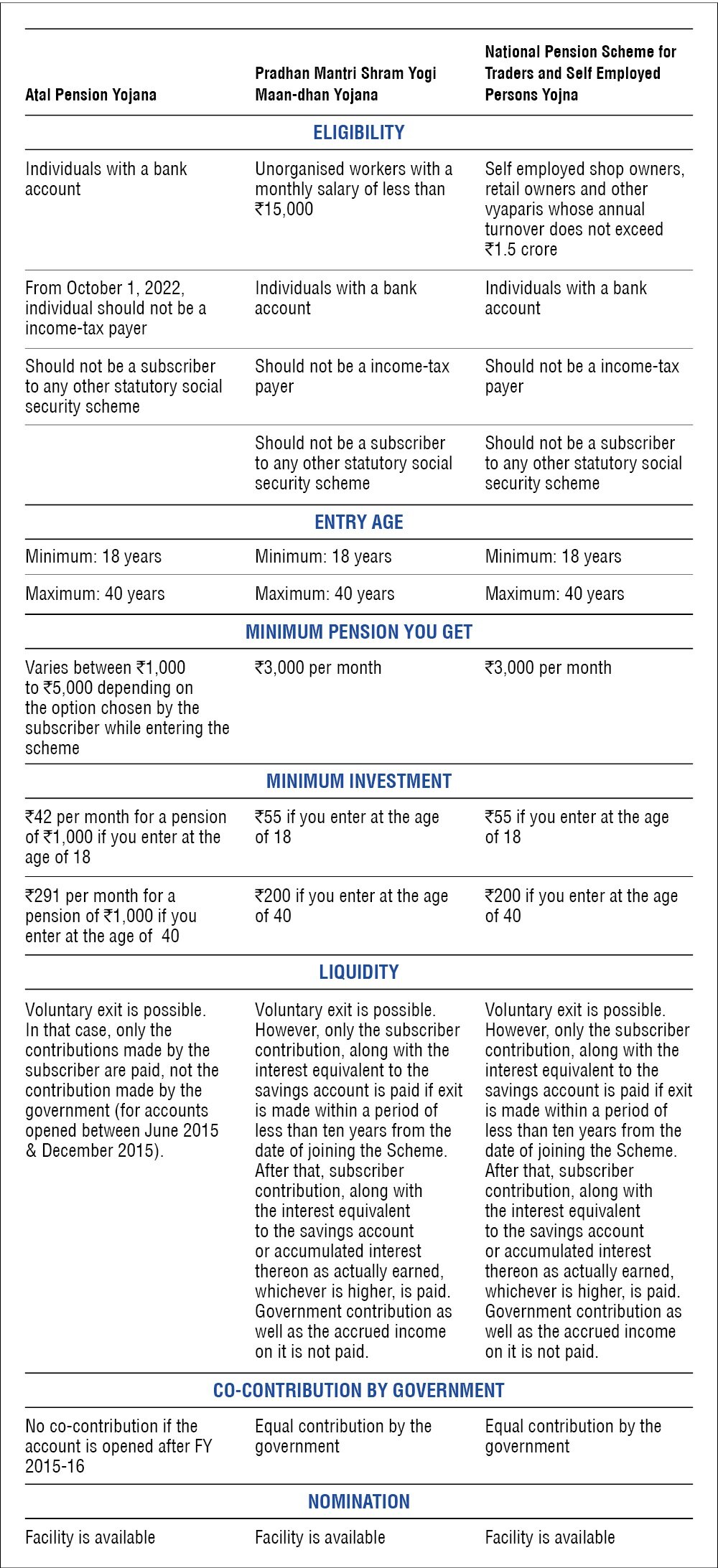

Comparison

The following is a comparison of Atal Pension Yojana, Pradhan Mantri Shram Yogi Maan-dhan and National Pension Scheme for Traders & Self Employed Persons Yojna.

This article was originally published on December 14, 2021, and last updated on October 07, 2022.

Ask Value Research ![]()