The Indian cement sector is witnessing an IPO after a gap of nearly a decade and a half. Nuvoco Vistas is the fifth largest producer in the country and is the largest player in the fast-growing geography of eastern India. It is promoted by the Nirma group (run by Dr Karsanbhai K Patel). The group is a diversified conglomerate with business interests in chemicals, detergents, healthcare and real estate.

Starting its journey with a plant having the capacity of 2 million tonnes per annum (MTPA) in Rajasthan in 2014, the company has been on an expansion spree through acquisitions. Two of its notable acquisitions include LafargeHolcim in 2016 (11 MTPA) and Emami Cement in 2020 (8.3 MTPA). At present, its total capacity is pegged at 22.3 MTPA, spreading across 11 cement plants, along with 105 megawatts of captive power plants.

The company broadly operates in three segments: cement, modern building materials and ready-mix concrete (RMX). While brands such as Concreto, Duraguard and Artiste are part of its cement and RMX portfolios, modern building materials (which include products such as construction chemicals, tile adhesives, wall putty, etc.) are sold under the 'Zero M' and 'Instamix' brands.

Strengths

Favourable geography: With eight out of 11 plants located in East India, the company has a strong presence in this region. This part of the country witnessed a demand growth of 9-10 per cent during 2015-20 as compared to the growth of 3-5 per cent in the rest of the country. This region is also expected to continue to have above-average growth rates for the next five years.

Strong distribution facility: The company has a large sales and marketing network, comprising more than 16,0000 dealers and 244 clearing and forwarding agents. It has developed strong relationships with its channel partners and plans to leverage its loyal base of customers to increase the sales of its portfolio comprising over 50 products.

Research & development: The company has a dedicated R&D centre in Mumbai through which it develops innovative products, such as quick-setting cement, ready-to-use wet micro concrete and fast-bonding adhesives for tile fixing. It has a patent for one product and has filed applications for three more products.

Risks

Regulatory risk: The company is mired in a huge number of legal proceedings ranging from issues such as environmental pollution to criminal negligence. While the cases are generally in the nature of the regular operational litigation, the sheer number (277 criminal, 139 material civil cases, 421 actions by statutory/regulatory authorities and 210 tax proceedings) is a cause of concern.

Mining concern: The liberalisation of the mining sector through the Mines and Minerals (Development and Regulation) Amendment Act, 2021 is likely to result in the lapsing of the company's vested rights in seven limestone mines. The company's operations are heavily dependent on its ability to procure a sufficient amount of limestone and any difficulty getting raw materials will have an adverse impact on its operations.

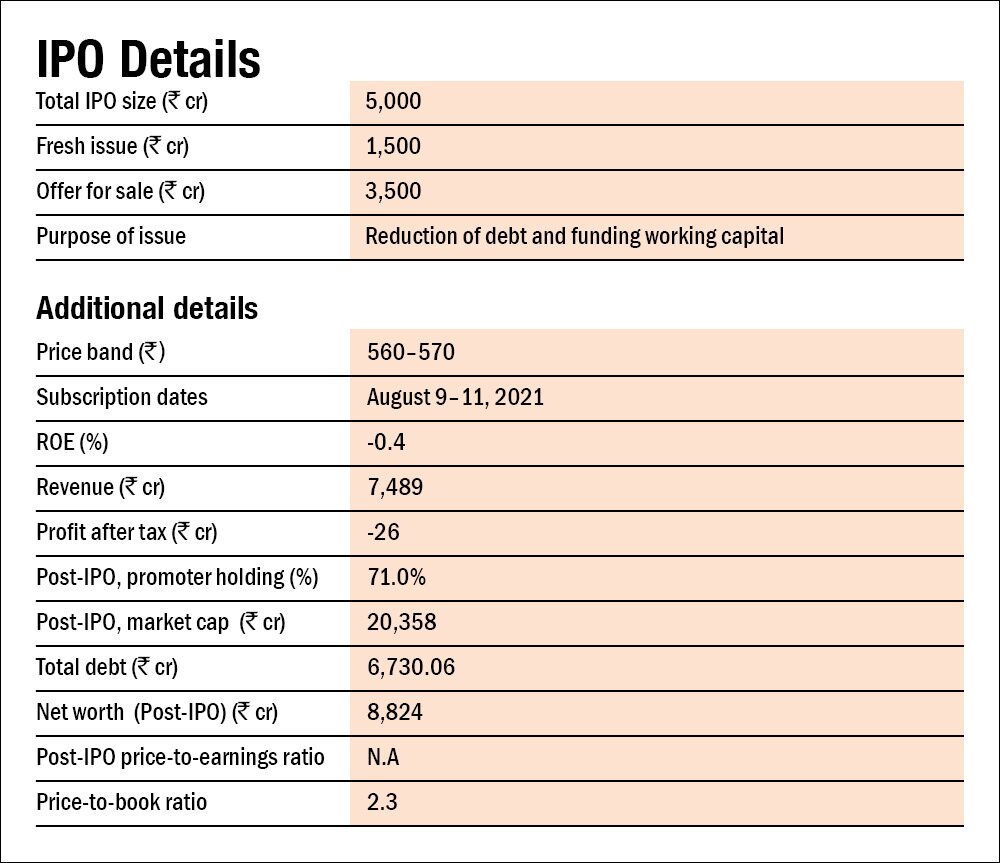

Poor financials: The company has a stretched balance sheet, with borrowings of Rs 7,130 crore as on June 30, 2021. Besides, the company reported a loss of Rs 26 crore in FY21. Although the loss could be attributed to the muted performance during the pandemic period, the fact remains that the cement industry is capital intensive and is generally not known for its high margins.

IPO questions

The company/business

1. Are the company's earnings before tax more than Rs 50 crore in the last twelve months?

No. The company's profit before tax in FY21 stood at Rs 36.5 crore.

2. Will the company be able to scale up its business?

No. The cement business is a very capital-intensive business and it requires a lot of lead time to establish a new plant. With the existing plant utilisation at a high level and a stretched balance sheet, it is not going to be easy for the company to scale up.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes. The company has a wide brand portfolio of more than 50 products that are valued by its customers.

4. Does the company have high repeat customer usage?

No. With construction activities being not a regular occurrence, there is no such high repeat customer usage.

5. Does the company have a credible moat?

No, although the company has many brands and has even obtained patents for its product, cement is ultimately a highly commoditised product and there are many competitors in the sector. There is no specific moat that is enjoyed by the company.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the total number of regulatory actions and litigations involving the company are extremely high. Besides, the risk of losing mining rights makes the company vulnerable.

7. Is the business of the company immune from easy replication by new players?

Yes, although the industry is fragmented, its capital-intensive nature prevents easy replication by new players.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes. As of now, there is no substitute for cement and other building materials. And it is not very likely that these products will get outdated.

9. Are the customers of the company devoid of significant bargaining power?

No, the company's customers have plenty of options to choose from when they want to buy cement, as there are other well-renowned brands available.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes, the company is still the fifth-largest player in the industry and its raw materials are also primarily commodities. Owing to these two factors, the company's suppliers do not have significant bargaining power.

11. Is the level of competition the company faces relatively low?

No, the cement industry is a commoditised and fragmented industry and therefore, the company faces a lot of competition from other players in the market.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than a 25 per cent stake in the company?

Yes. The promoter will continue to hold around 71 per cent of the company post IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

No, the chairman, managing director and CFO together have less than 15 years of leadership experience at this company.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

No, the company has an extremely high number of cases. This is a cause of concern.

16. Is the company's accounting policy stable?

Yes, we have no reasons to believe otherwise.

17. Is the company free of promoter pledging of its shares?

Yes. While none of the shares are currently pledged, there is a 'springing pledge agreement' whereby the promoters are obligated to create a pledge if certain borrowings are not repaid within a certain period.

Financials

18. Did the company generate the current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

No. While the current ROE is around -0.4 per cent, the three-year average ROE is 1.3 per cent. Similarly, while the current ROCE is nearly 4.2 per cent, the three-year average ROCE is 5.4 per cent.

19. Was the company's operating cash flow positive during the previous three years?

Yes, the company's cash flow from operations was positive in the previous three financial years.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

No, the company's revenue increased by only 6 per cent CAGR in the last three years.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

Yes, the company's net debt-to-equity ratio was 0.9 and its interest-coverage ratio was around 2.2 times as of FY21.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

No, the company has receivables worth Rs 454 crore in FY21. The cement business generally requires a high amount of working capital.

23. Can the company run its business without relying on external funding in the next three years?

Yes. Since the company plans to utilise the proceeds from the IPO for reducing its debt, it should be able to run its existing business without any further external funding. But if it wants to carry out any further expansions, it would be difficult to do so without external funding.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes, the company's short-term borrowings decreased from Rs 661 crore in FY20 to Rs 198 crore in FY21.

25. Is the company free from meaningful contingent liabilities?

No. The company had contingent liabilities worth more than Rs 500 crore and certain unquantifiable contingent liabilities. All these factors could dent its profitability significantly.

The stock/valuations

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No, the company's stock will offer an operating-earnings yield of 2.6 per cent on its enterprise value.

27. Is the stock's price-to-earnings less than its peers' median level?

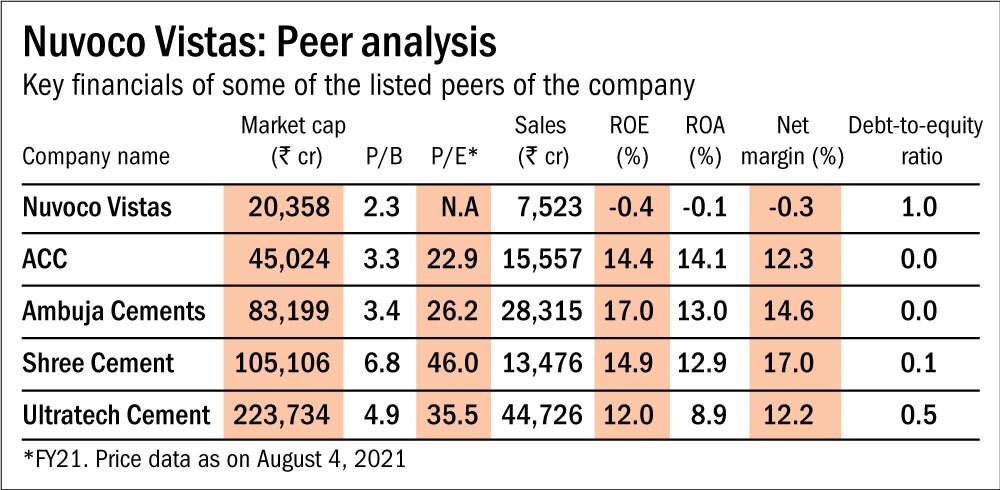

N.A. The stock's price-to-earnings ratio cannot be calculated as it made losses in FY21.

28. Is the stock's price-to-book value less than its peers' average level?

Yes, the stock's price-to-book value of 2.3 is less than its peers' average level of 4.6.

Disclaimer: The authors may be an applicant in this Initial Public Offering.

Ask Value Research ![]()