A retail investor's core debt portfolio must be able to tick the boxes of safety, reasonable returns, a broad investment universe, and low risk and volatility. In the debt-fund domain, the short-duration category is one which seems to fulfil all these criteria. With an AUM of over Rs 1.42 lakh crore as of May 2021, this category currently ranks fourth across all debt funds (after liquid, corporate bond and low duration funds), highlighting the kind of investor interest it holds.

These are challenging times for debt investors given the low yields on their debt investments. The environment is challenging for investment managers as well. What are the challenges, you ask?

Possibly the biggest one is the ultra-low interest rate environment. A reflection of which can be seen in current returns of funds that are in stark contrast to the returns of last one- and one-and-a-half year.

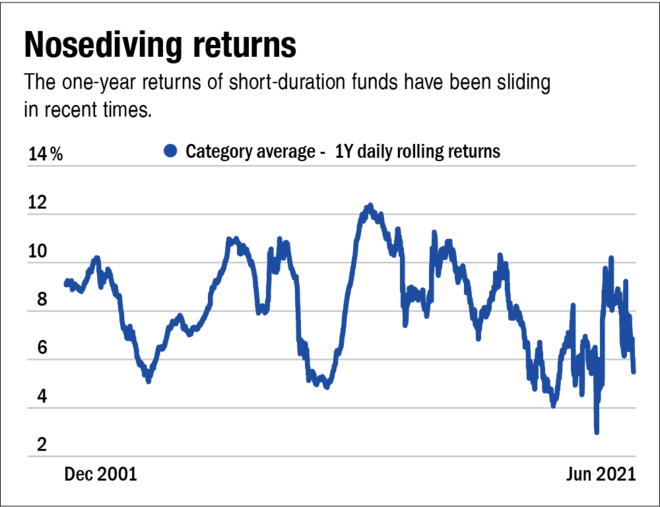

The graph 'Nosediving returns' shows how the one-year returns of short-duration funds have started plummeting in the recent times. As of June 2021, the category has managed to deliver an average one-year return of about 5.4 per cent. This is in sharp contrast to 9-9.5 per cent that the category was delivering over the last one to one-and-a-half years. Having said that, this trend is in sync with what you see across the fixed-income space.

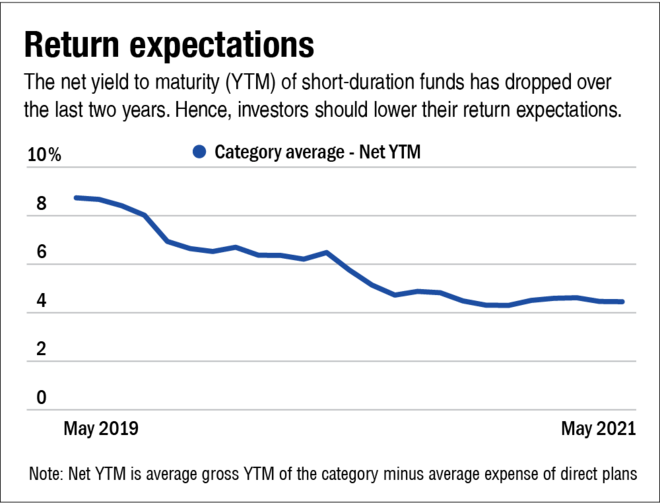

The graph 'Return expectations' shows the average net yield to maturity (YTM; after factoring in expenses) in the last two years. As can be seen, the current average YTM is under 5 per cent. If the current YTMs are anything to go by, debt-fund investors must brace themselves up for lesser returns in the near future.

In the current context, there are two conflicting things happening in the debt-fund space. One, with low yields, the accrual income that an investor generates is low. Two, while the RBI has communicated that it will continue with the accommodative stance as long as it's needed, there is an expectation that the rate cycle may only gradually reverse from here. Now when yields rise, the NAV of debt funds fall. But short-duration funds are relatively better equipped to handle the rising-rate environment. Given their relatively shorter maturity profile of one year to three years, the impact of rising rates will be limited here. Also, as and when short-term rates increase progressively, the underlying bonds will get reinvested at better yields. We believe that over a holding period of three years, the impact should be moderate.

For an investment manager, another challenge is the trust issue. Because of the lockdown and the impact on the economy and business, the fear of credit events has risen. In these times, the last thing a fund manager would want is to be hit by unfortunate credit events. Thus, fund managers are on a tight rope currently.

Strategies adopted by short-duration funds

Fund managers are navigating the current tricky environment by adopting the following strategies.

Playing it safe

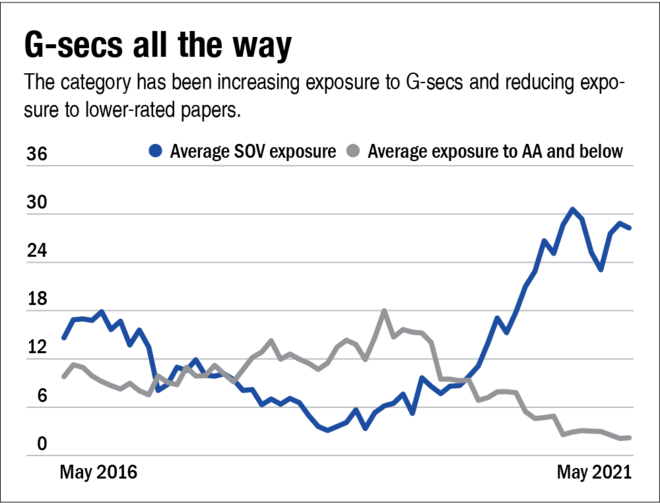

The short-duration category, which was hit hard in the aftermath of the IL&FS crisis, is currently playing it safe with most of the funds avoiding credit calls and investing in top-rated assets. Given the risk aversion we have been seeing since the pandemic, there has been a shift to quality papers. So, the funds have raised their sovereign exposures while exposure to lower-rated papers have been comparatively muted. Look at the graph titled 'G-secs all the way'. Having said that, there are funds which have always been quality-focused.

Adopting a barbell strategy

Some fund managers are adopting barbell strategies, where he/she builds the portfolio with a blend of shorter and longer-duration bonds. Short-maturity bonds shield the portfolio from rising rates, given the low maturity. Further, the money that comes up for redeployment gets reinvested at better yields. As for the longer-duration bonds, they help generate better returns, given their comparatively higher rates.

Axis Mutual Fund is one such fund house that actively uses this strategy. Devang Shah, Co-Head -Fixed Income, Axis Mutual Fund says, "Our portfolios endeavour to play our cautious stance through carry and leverage barbell strategies across the yield curve where opportunities present themselves. In our short- and medium-duration strategies, we are following barbell strategies - a strategy where we mix long-duration assets (eight to 10 years) with ultra-short assets, including credits (up to two years), to build a desired portfolio maturity. The ultra-short assets will help us play the reinvestment trade whilst limiting the impact of MTM [mark-to-market loss] as yields rise. Long bonds will likely add value in capturing higher accruals with relatively lower credit risk and lower MTM movement in the current context."

What should investors do?

With falling returns from their debt investments, investors are tempted to invest in riskier products to boost their returns. But that would be a mistake. Here's what to do then.

Don't fall for the lure of high returns

Accept the market reality of low yields and don't fall for the lure of high returns as that doesn't come without high risk. Thus, for your core debt allocation, short-duration funds should be your mainstay and the bulk of your money should stay invested here.

Now, for some yield enhancement, an investor has two options: either assume credit or duration risk. On the credit side, besides a host of high-yielding low-rated bonds, some innovative products are hitting the market. While these products may get higher ratings, the fact remains that they are a riskier variety. So, if you want to assume credit risk, don't take more than what you can digest and take only limited exposures. Most investors are sensitive to losses when it comes to their debt allocations. So, it's important to first understand and acknowledge the risks associated with such instruments.

On the duration front, it is not an opportune time to go for longer-duration funds. Until last year, long-duration funds and gilt funds (which typically invest in medium- to long-duration government securities) had been high on popularity on the back of the RBI cutting rates multiple times. With the expectation of gradual rise in rates, long-duration bonds are most vulnerable and so are funds investing in such bonds.

Consider target-maturity funds

To supplement the returns of high-quality short-duration funds, one can look for alternatives like target-maturity funds, which aim to capture the yields on specific maturity segments. Since the gap between the yields of medium-to-long-term bonds and short-term bonds is wide enough, there is a chance to earn better returns. As of today, the five- to seven-year maturity range seems to be the sweetest spot as their yields look attractive relative to shorter-term rates. Thus, you may look to take limited exposure to such funds.

These are high-quality funds which follow a roll-down maturity style. So, the fund manager sets a maturity target at the outset and the maturity rolls down over a period. Therefore, the interest-rate risk reduces here and so these funds can be useful amidst a rising-rate scenario. Further, the visibility of returns is a big plus here. So, if you can tolerate some intermittent volatility and have sufficient time in hand, then target maturity funds can benefit you.

Conclusion

For your core debt holdings, short-duration funds are a worthwhile choice. Although the yields are low currently, it is better to not put your core capital at risk for a marginally higher return. So, rationalise your returns expectations. For our selection of quality-focused short duration funds see the August issue of 'Mutual Fund Insight'.

Ask Value Research ![]()