Ravi (39) invested a lump sum of Rs 1 lakh from his savings in equity funds during the market crash in March 2020. Like many of his friends, he had a view that markets had bottomed out and that it would be the opportune time to make some profits in the near future.

With the markets having recovered so quickly and recorded new highs over the past few days, the value of his investment is close to Rs 2 lakh, giving him an annualised return of more than 55 per cent.

Ravi is overjoyed about his decision to invest during the market fall. Now, he wants to know whether he should book profits by redeeming the investment. And if so, what proportion of the investment should be withdrawn. Here are some suggestions for him.

One cannot always succeed in timing the market

- Ravi has been lucky that the stock market not only recovered sharply but also recorded new highs soon after he made the investment. This may give him an impression that timing the market is an easy thing to do and indeed a good strategy.

- But that's not right. The market moves unpredictably and no one can time it perfectly. Ravi should consider this as a one-off instance. It would be wrong to expect such returns from equity investments in the future.

One should not miss the best days of the market

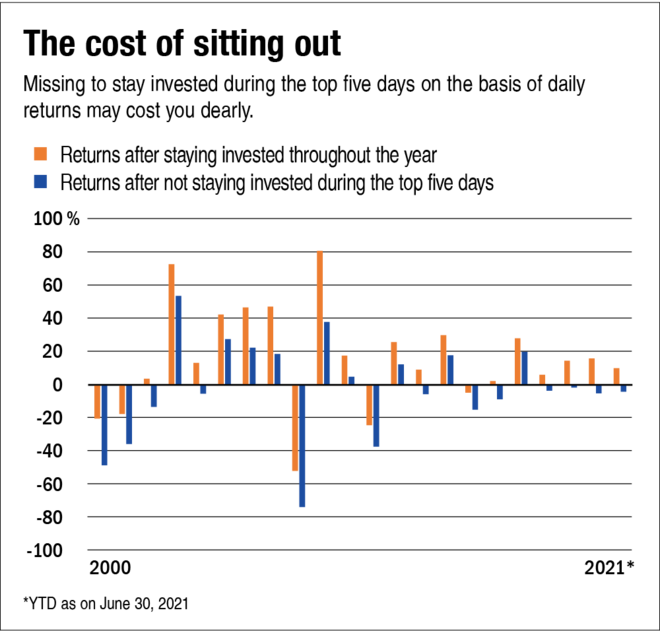

- When you try to time the market, it is quite possible for you to miss out on some of the best days when the stock market makes maximum gains. Look at the graph titled 'The cost of sitting out'. The annual return of the Sensex depletes significantly if you remove the best five days on which the Sensex made maximum gains.

- If considered from the long-term perspective, missing out on a single day just to time the market will deprive you of not only single-day gains but also the benefit of further compounding of the missed returns.

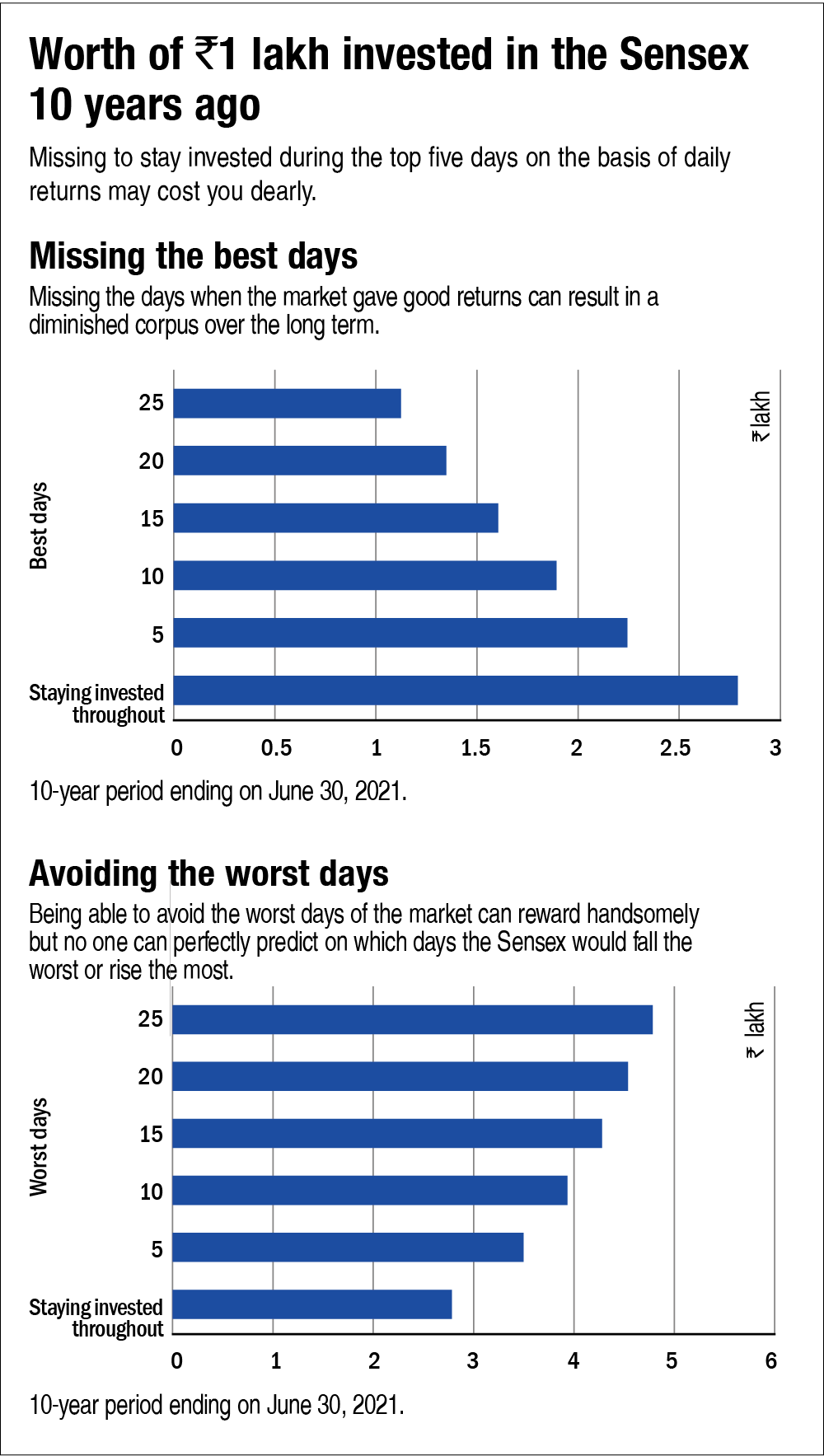

- Similarly, as shown in the graphs titled, 'Missing the best days' and 'Avoiding the worst days', one would have lost about 19 per cent if one had missed staying invested on the five best days of the Sensex over the last 10 years.

Redeem only if your goal is nearing

- Equities are meant for long-term investors with a time horizon of at least five years. Do not invest if you are likely to need the money before the time period.

- One should stay invested throughout the tenure and avoid making unnecessary transactions. You will gain maximum benefits from equities if you stay invested for a longer time period, as you get to benefit from compounding.

- Ravi should, therefore, remain invested and avoid redeeming the investments if he doesn't need the money now. He can link his investment to any of his long-term goals like retirement or his child's education.

An asset-allocation plan is a must

- Having an asset-allocation plan in place helps you book profits in a systematic and methodical way.

- Devise a rule for rebalancing, say, you will rebalance at the end of every financial year or whenever the asset allocation deviates by more than 10 per cent of the desired ratio.

- For example, if Ravi decides a 75:25 allocation between equity and fixed income and now as the markets have gone up, he may liquidate 25 per cent of the portfolio and invest it in fixed income. Likewise, if the market crashes and the ratio becomes 60:40, he should liquidate 15 per cent of the portfolio from the fixed income and invest in equities to again make it 75:25.

Never invest in a lump sum

- Ravi should not have made any lump-sum investments. What if the market would have crashed further, say by 30 per cent, instead of moving up? His investment would have reduced to just Rs 70,000.

- While investing in equities, one should always spread the investments over a period of time. Investing systematically through an SIP or STP reduces the risk of entering the market at the wrong level, as the purchase cost is averaged out.

- If you have a lump sum, it should be spread over a few months. A rule of thumb is to spread it over half the time required to earn that money, up to a maximum of three years.

Don't ignore these

- Emergency fund: Maintain the money equivalent to at least six months' expenses in a combination of a liquid fund and sweep-in deposit. It comes in handy during unforeseen circumstances.

- Life insurance: Adequate life cover is a must if you have financial dependents. For this purpose, consider pure term plans only.

- Health insurance: Owing to COVID, it has become even more important to have adequate health cover for all the family members. Apart from the health insurance provided by your employer, you should have one independent policy as well.

This article was originally published on October 27, 2021.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()