I am a retail investor who has chosen to invest equivalent of my six-month salary in gold to respond to emergencies. Are gold mutual funds a suitable alternative to physical gold/gold ETF? What is the level of trading liquidity in the gold ETFs in India?

- Vijayaraghavan Sundaravaradan

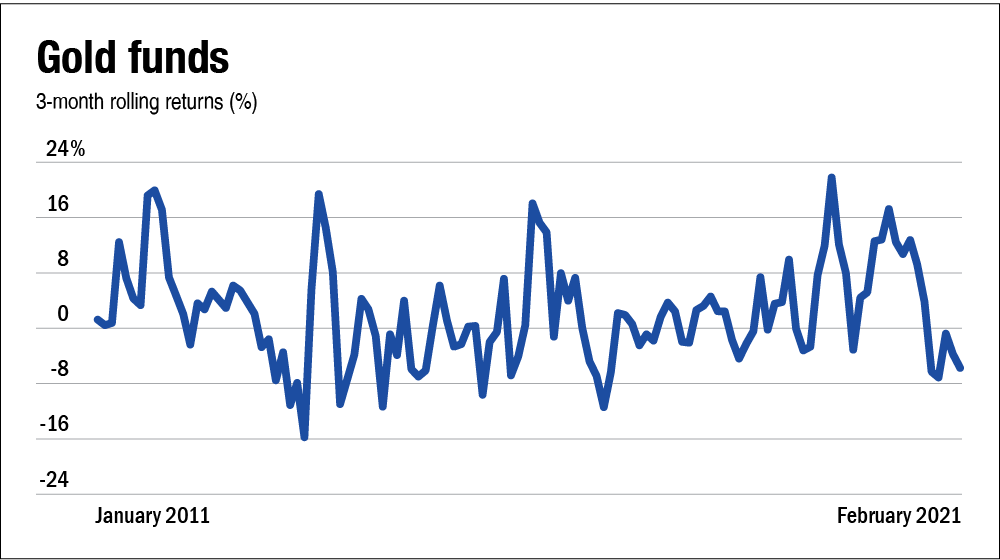

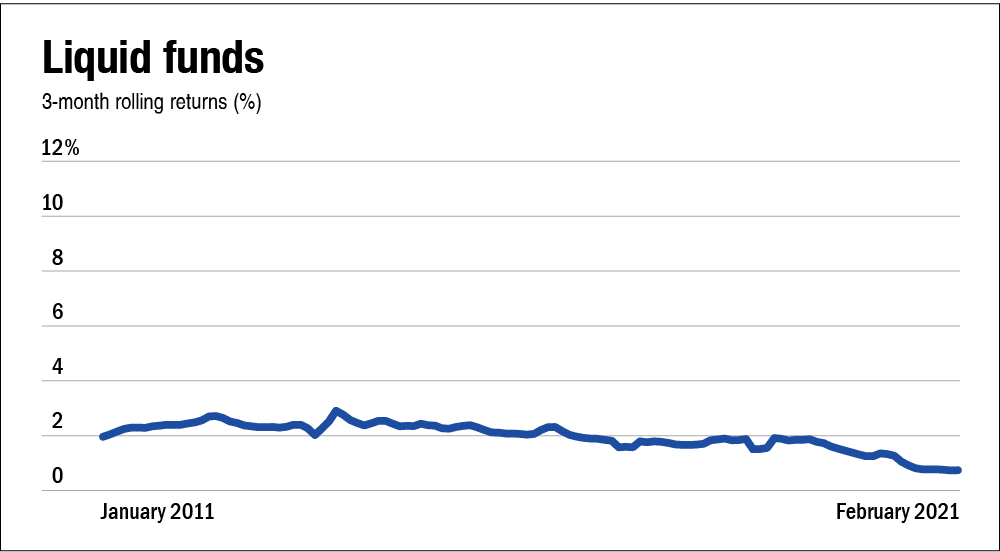

Gold is not a suitable asset class for creating an emergency corpus. That is because gold is far too volatile an asset class to be suitable for this investing need. Just look at the graph: Gold funds, which shows the returns of gold in any block of three months over the last 10 years. You can see that in these three month durations, their returns have oscillated fairly widely in a range from as high as 20 per cent to as low as -15 per cent. That's the kind of volatility that your emergency corpus cannot absorb. For emergency corpus, you want the returns to be much more linear and much smoother, like the ones in the graph: Liquid funds. Similar to the Gold funds graph, this graph shows the returns of liquid funds in any block of three months over the last 10 years. One can see that the returns of the liquid funds are much more moderate, but with your emergency corpus, returns are never a priority. You should prioritise safety, low volatility and liquidity. And those are the kind of tenets that you get from liquid funds. So I would say, to build an emergency corpus, you should select a couple of good liquid funds and park your money over there.

Gold is considered a safe haven but not in the context of creating an emergency corpus. One should look at investing in gold, if they have lost faith in the economy or if the currency is falling apart. That is when gold appears a safe haven as a protector of worth of your money and as the ultimate protector of wealth. Also, some investors like to keep some allocation of their long-term portfolio in gold in steady state as it generally acts as a good hedge against equity because whenever equity markets fall sharply, gold tends to do well. So from that perspective, there is some merit in having some allocation to gold in a steady state. Broadly, those are the kind of uses for which one can look at gold.

Now coming to your question about gold funds vs gold ETFs. Well, the charm of gold funds lie in their convenience because you don't need a demat account or a trading account to be able to invest in them. So that's why investors who do not otherwise invest in stocks prefer gold funds for this convenience. Also, they offer good liquidity because the AMCs stand committed to honour your redemption request and it is not dependent upon the trading volumes on a stock exchange. But the point is that this convenience comes at a slightly higher cost, because in gold funds you incur an additional cost of about 15-20 basis points per annum which is over and above the expense ratio of the gold ETF. However, the numbers suggest that investors are pretty fine paying this extra cost for the convenience they get, because if we compare the assets under management of gold funds vs gold ETFs, you would realise that for a majority of fund companies, about half of their assets under gold ETFs are contributed by the gold funds. So purely on an AUM perspective, investors are fairly divided between their preferences for gold funds and gold ETFs.

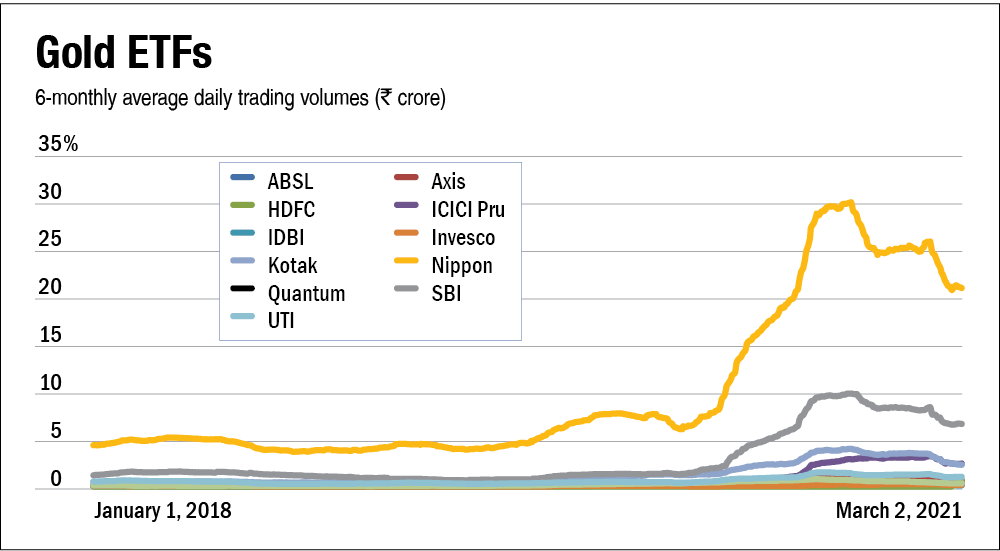

Now coming to the issue of liquidity in gold ETFs, just look at the graph: Gold ETFs, which depicts the average daily trading volumes in gold ETFs in any block of six months over the last three years. You would notice how far ahead the Nippon India ETF Gold BeES is, versus its peers in terms of liquidity. So while this fund generates an average daily trading volume of upwards of Rs 20 crore, others are far behind, while many are well below Rs 1 crore worth of average daily trading volume. Thus, clearly on that matrix, selectivity matters. But in case you are looking to add gold to your portfolio more from a steady state allocation perspective and you don't mind compromising on liquidity, then I would suggest you to look at Sovereign Gold Bonds (SGBs) which appear to be a far superior option because they provide 2.5 per cent guaranteed returns over and above the appreciation in the gold price and they are also more tax efficient.

This article was originally published on March 15, 2021.

Ask Value Research ![]()