Incorporated in 2016, this B2C company is engaged in the business of home healthcare and wellness products. Its diversified portfolio primarily caters to the home-healthcare sector. Nureca's products are classified into five categories, which are as follows:

1. Chronic-device products: Sold under the brand name of 'Dr Trust', products under this category include blood pressure monitors, pulse oximeters, thermometers, nebulisers, self-monitoring glucose devices, humidifiers and steamers.

2. Orthopedic products: Sold under the brand name of 'Dr. Physio', products under this category include rehabilitation products, such as wheelchairs, walkers, lumbar and tailbone supports and physiotherapy electric massager.

3. Mother and child products: Sold under the brand name of 'Trumom', products include breast pumps, bottle sterilisers, bottle warmers, and baby carrycots.

4. Nutrition supplements: Products include fish oil, multivitamins, probiotics, apple cider and vinegar.

5. Lifestyle products: Products include smart weighing scales, aroma diffusers and fitness trackers.

Strengths

- Online presence: The company generates 95 per cent of its revenues by selling its products online on its website drtrust.in, as well as on other third-party e-commerce platforms such as amazon. Buoyed by a high volume of online sales, the company is all set to expand its presence offline, which could be a growth driver for the company. For this, the company has joined hands with Croma, an electronic retailer of the Tata Group.

- Chronic-disease products: Since the onset of COVID-19, there has been a rise in the demand for self-monitoring products, such as pulse oximeter, blood pressure monitors, to name a few. Also, the home-health markets in India and neighbouring countries are expected to grow at a CAGR of 11 per cent as per a report of F&S.

- Asset-light Model: Since the company outsources the manufacturing of its product, it does not need to invest heavily in physical assets, including plants and machinery, land and property. It will enable the company to scale up its business quickly as and when required.

Risks

- High competition: The company operates in a very fragmented industry, which means that a large number of small players are there to compete. Also, it faces stiff competition from organised and unorganised players, which leads to pricing pressure, resulting in reduced margins and lower profitability.

- Uncertainty about the accuracy of results: Home-health products are considered consumer-grade, due to concerns regarding the accuracy measures of products. Therefore, many big institutions don't use them.

- High dependence on third-party manufacturing: The company does not enter into long-term contracts for the manufacturing of its products and any manufacturing-related disruption could seriously impact its business.

IPO Questions

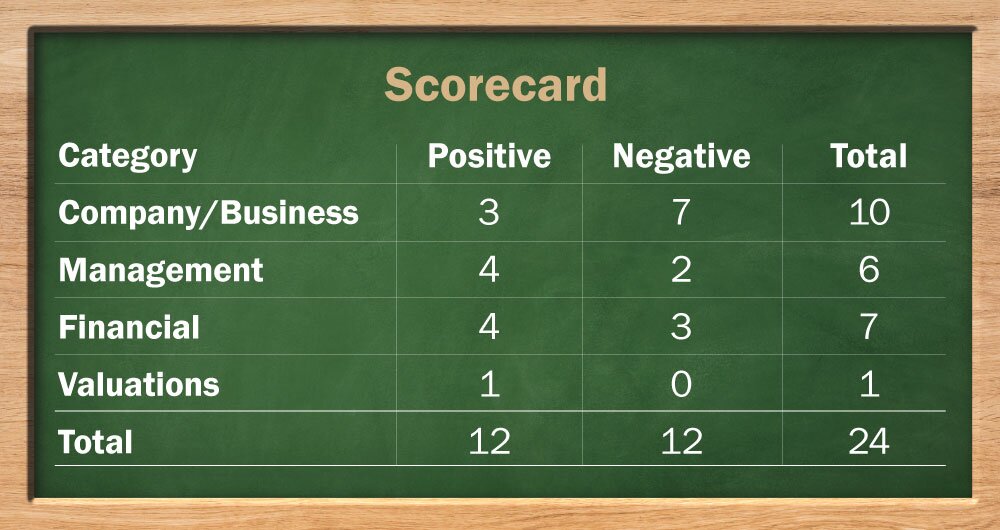

The company/business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

N/A. TTM (Trailing twelve months) numbers are not available, however, the company reported earnings before tax of Rs 48.6 crore in the six months ending September 2020 due to the pent-up demand for its products.

2. Will the company be able to scale up its business?

Yes, the increasing awareness of healthcare and the growing demand for self-monitoring and home-health products owing to COVID-19 have paved the way for the company to scale up its business. Moreover, the company follows an asset-light model, which makes its business model scalable.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes, the company sells products under its three brands - Dr. Trust, Dr. Physio and Trumom - mostly online.

4. Does the company have high repeat customer usage?

No, company's products, such as oximeters, BP monitors, etc., have a long usage time, mostly exceeding three-four years. Moreover, these technology products are mostly used on a need basis. Hence, repeat usage isn't there.

5. Does the company have a credible moat?

No, the company operates in a highly fragmented industry, wherein it competes with several other players from the organised and unorganised markets.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the company's operations are subject to extensive government regulations, such as the Drugs and Cosmetics Act and Food Safety and Standards Act, to name a few.

7. Is the business of the company immune from easy replication by new players?

No, Nureca is a B2C company which outsources its manufacturing, making its business model asset-light, which could be easily replicated by new players.

8. Is the company's product able to withstand being easily substituted or outdated?

No, the company faces stiff competition from well-established brands, such as Omron and Dr. Morepen, having market shares of 20 per cent and 15 per cent. respectively.

9. Are the customers of the company devoid of significant bargaining power?

No, the customers of the company have a variety of other options to choose from, which gives them the flexibility to switch to other brands.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes, the key raw materials used in products such as mono carton, batteries, inner corrugated box, among others, are readily available from several manufacturers located around the globe, including India.

11. Is the level of competition the company faces relatively low?

No, the company faces stiff competition from several players from the organised and unorganised markets.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, the promoter of the company, Mr Saurabh Goyal, holds a 46.6 per cent stake in the company. In total, the promoter group holds 93.3 per cent stake in the company.

13. Do the top three managers have more than 15 years of combined leadership at the company?

No, the company commenced its business in 2016.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

No, material litigation is going against the company. A search and seizure operation was conducted by the Income Tax Department at the promoters residences under the Wealth Tax Act.

16. Is the company's accounting policy stable?

Yes, we have no reason to believe otherwise.

17. Is the company free of promoter pledging of its shares?

Yes, the promoter's shares are free of pledging.

Financials

18. Did the company generate the current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

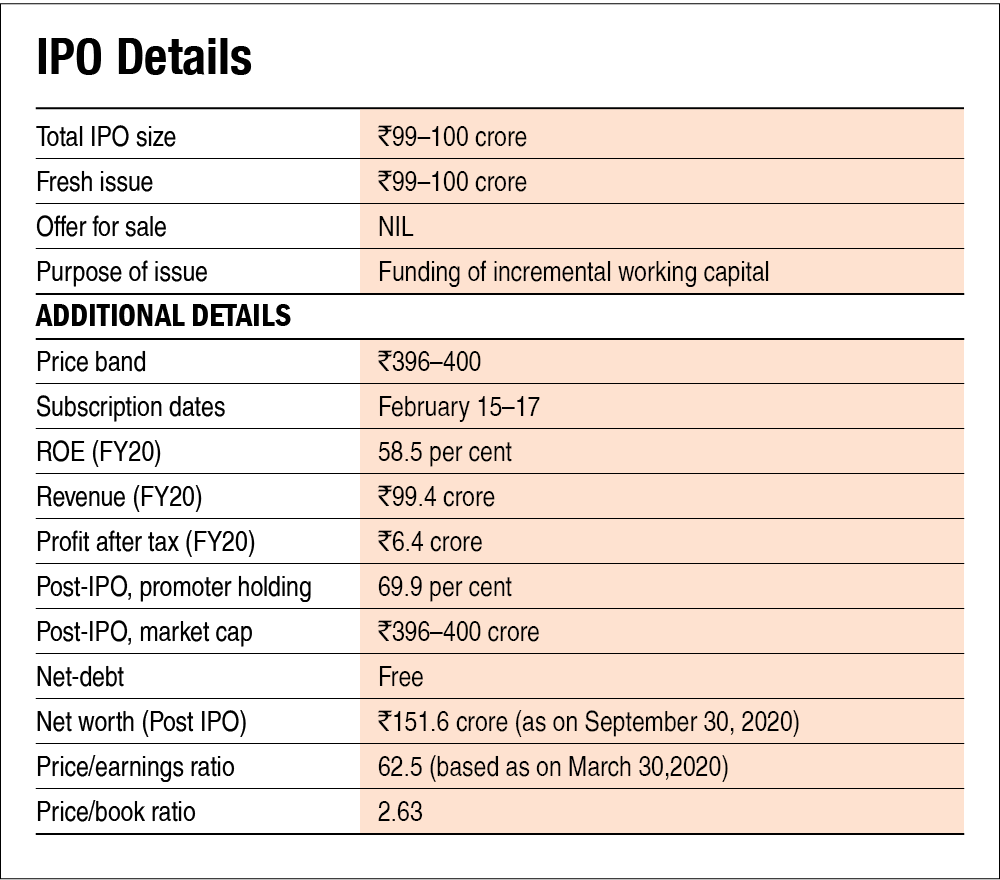

Yes, the company generated current ROE and ROCE of 58.5 per cent and 57.5 per cent, respectively. The three-year average ROE and ROCE stood at 215.6 per cent and 164.1 per cent, respectively.

19. Was the company's operating cash flow positive during the previous three years?

No, the cash flow from operating activities was negative in the financial year ending March 2020.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

N/A. The company commenced its business in November 2016. So, enough data is not available.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

Yes, the company is net-debt free.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

No, the company's working capital stood at around 23.2 per cent of its sales and the working-capital days stood at 58 days as of FY20.

23. Can the company run its business without relying on external funding in the next three years?

Yes, the company plans to use 75 per cent of the proceeds from the IPO to fund the incremental working-capital requirement and the fund will be deployed in the next three years.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

No, the company has increased its short-term borrowings in the last six months.

25. Is the company free from meaningful contingent liabilities?

Yes, the company is free from contingent liabilities.

The stock/valuations

26. Does the stock offer operating-earnings yield of more than 8 per cent on its enterprise value?

Yes, the stock offers an operating yield of 26.5 per cent post-IPO based on March 2020 numbers.

27. Is the stock's price-to-earnings less than its peers' median level?

N/A. The company does not have any listed peers engaged in similar lines of business. However, the stock's current P/E ratio stood at 62.5 based on March 2020 numbers (TTM numbers not available).

28. Is the stock's price-to-book value less than its peers' average level?

N/A. The company does not have any listed peers engaged in similar lines of business. However, the stock's current P/B ratio stood at 2.63 based as on September 30, 2020.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()