Mutual fund investors have to deal with broadly two asset classes: equity and debt. Depending on your goals, both have a role to play in your portfolio. At Value Research, we have frequently professed equity for long-term goals - those that are at least five years away. Children's education and marriage, your own retirement, etc., are classic long-term goals.

Debt is for short-term goals. Unlike equity, debt carries less risk and hence will not likely cause a capital loss in the short term. However, this safety comes with comparatively lower returns than equity. An investor has to find out the right asset allocation for him, i.e. combine equity and debt in the right proportion. To fulfil your equity and debt requirements, you have equity and debt funds.

The convenience of hybrid funds

Hybrid funds, as their name suggests, combine both equity and debt in various proportions. For someone who wants the convenience of readymade asset allocation, they can be a good choice. Currently, you can invest in seven types of hybrid funds. Aggressive hybrid funds invest 65-80 per cent in equity and the rest in debt. Among hybrid funds, they have the highest equity allocation. On the other end of the spectrum are conservative hybrid funds that invest 10-25 per cent in equity and the rest in debt. You also have other types such as multi-asset-allocation funds, equity-savings funds and so on.

Hybrid funds can solve the problem of asset allocation for many investors. If you are happy with the equity-debt split of your hybrid fund, by buying just one fund, you get the advantage of both equity and debt in the desired proportion. What's more, you don't have to maintain that proportion as the fund manager will do that for you.

But what about the cost?

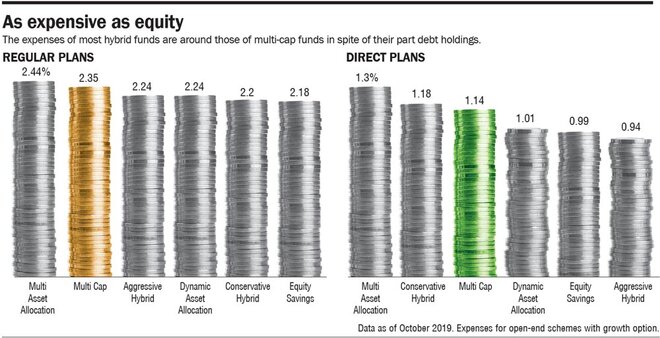

Logically, the more the debt portion in the asset mix of hybrid funds, the closer their expenses should be to those of debt funds. However, that's not the case. As the graph titled 'As expensive as equity' suggests, the median expenses of the various categories of hybrid funds are not very far from the median expenses of multi-cap funds, the classic equity funds.

In December 2018, the regulator had capped the expenses that mutual funds can charge based on their assets. Broadly, now expenses taper as the assets rise. This change was also welcome as it lowered the cost of investing in mutual funds. But one category of funds that perhaps requires a deeper scrutiny is hybrid funds.

An alternative model

Any mutual fund investor knows that costs have a direct bearing on returns. But how do you cut the expenses of your hybrid? By scratching your own itch.

Any enterprising investor can create a hybrid fund of his own by combining a multi-cap fund and a short-duration debt fund [let's call it the 'do-it-yourself' (DIY) hybrid]. By doing so, one can benefit from the lower expenses of the debt fund. If you are a risk-averse investor, a Nifty-based index fund can take the place of the equity fund. Since index funds have very low costs, your DIY 'hybrid' fund can have much lower expenses than the readymade one.

Of course, a readymade hybrid fund provides you flexibility and tax efficiency. When your fund manager rebalances the portfolio, he doesn't have to pay any tax but if you are doing it on your own, you will have to.

So given these, is there a case for a DIY hybrid fund? To answer this question, we take a closer look at conservative hybrid funds. These funds invest only 10-25 per cent of their assets in equity and the rest in debt. In spite of a sizeable debt allocation, their expenses are similar to those for equity funds. Hence, they make for the best choice for our analysis.

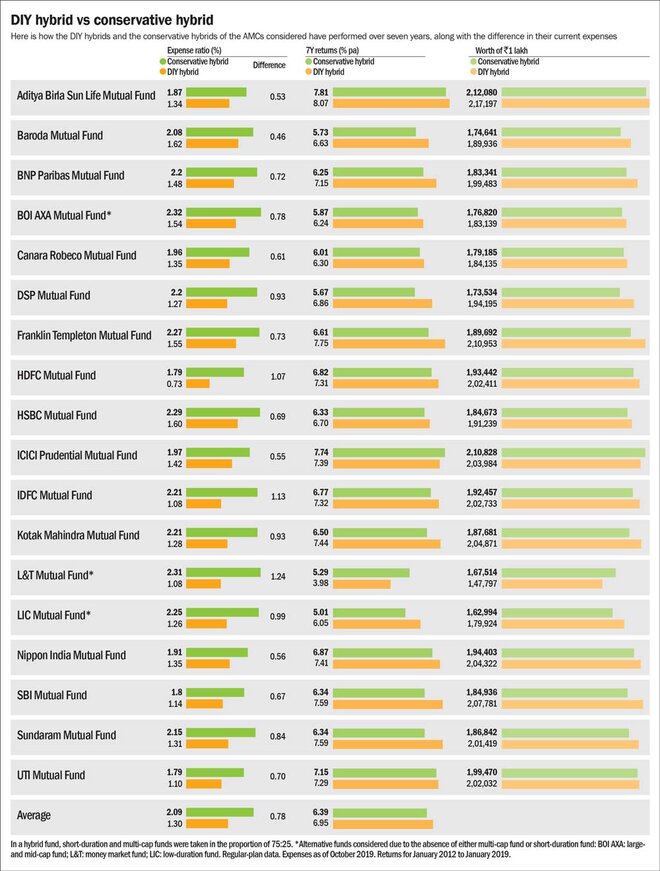

DIY hybrid fund vs conservative hybrid fund

In order to compare a DIY hybrid with an existing conservative hybrid fund, we considered the conservative hybrid funds of the AMCs given in the graphic 'DIY hybrid vs conservative hybrid'. Only those AMCs whose conservative hybrid funds and diversified equity funds both are at least seven years old are included.

Now to create our own hybrid funds, we took a multi-cap fund and a short-duration fund from the same fund houses. If a multi-cap fund was not available, we took a large- and mid-cap fund; and if a short-duration fund was not available, we considered a fund with a lower duration. The equity-debt allocation was set at 25:75. Only regular plans with growth options were taken.

We then compared the expenses and returns of the 'DIY hybrid funds' and the conservative hybrid funds for the last seven years, from January 2012 to January 2019, with rebalancing carried out in January every year. We assumed a one-time investment of Rs 1 lakh at the start of the period.

The graphic 'DIY hybrid vs conservative hybrid' details the difference in expenses between the conservative hybrid funds and the DIY hybrid fund. On average, a conservative hybrid fund charges 0.78 percentage points more than our DIY hybrid fund.

In terms of performance, the DIY hybrids outperformed their corresponding conservative hybrid funds in 16 out of 18 cases under consideration. The average pre-tax outperformance of the DIY hybrids was about 0.65 percentage points per annum. As stated earlier, a DIY hybrid would require yearly rebalancing. So, you will have to sell part of the equity or debt component that has gained and buy the one that has lost value in such a way that the original equity-debt allocation of 25:75 is restored. This selling would require you to pay tax.

For equity, one has to pay long-term capital-gains tax of 10 per cent of the gains above Rs 1 lakh. In order to make our analysis rigorous, we did not consider the Rs 1 lakh exemption. For debt, your capital gain would be a short-term gain and would be taxed according to your tax slab. In our analysis, we considered the highest tax slab of 30 per cent.

Even after taking the tax effect into account, the DIY hybrids outperformed the conservative hybrid funds in 16 out of the 18 cases. The graphic 'DIY hybrid vs conservative hybrid' captures the analysis.

Overall, the DIY hybrids outperformed the conservative hybrids by 0.55 percentage points per annum post tax. While this difference might not look substantial, over very long periods, such as 15 or 20 years, the impact will be much more pronounced, thanks to the power of compounding.

Wait... there's more

The message is quite clear: by creating your own hybrid, you can save on expenses and get better returns as well despite the taxation. This analysis is food for thought for fund houses to rationalise their hybrid-fund expenses. The DIY hybrid has many other positives.

In our analysis, we considered the multi-cap and short-duration funds from the same fund houses. As an investor, you don't have any such restriction. You can invest in funds from different AMCs and get the best funds, which could further boost your overall returns.

In terms of asset allocation, hybrid funds are bound by their mandates. Your DIY hybrid doesn't have any such restrictions. You can invest in any debt-equity proportion of your choice.

If you can handle an online investment account, rebalancing might take a few minutes of your time per year! Often enough, you can maintain the desired allocation by inflows alone. Just invest more in the asset class that has fallen in value such that your desired allocation is achieved.

What should you do?

The final call rests with you. By creating your own hybrid fund, you can save on expenses. But this comes at the cost of convenience. When you create your own hybrid, you will have to not only rebalance periodically, but also pick the right funds and monitor them. If either your debt or equity funds go haywire, you will have to replace it. The reward will be in terms of less expenses and hopefully better returns. If you choose to go with the readymade hybrid, your fund manager will take care of rebalancing and there will be no capital-gains taxes unless you sell.

Ask Value Research ![]()