With the lowering of interest rates in recent years, retirees who rely on fixed deposits are in a tight spot. While the decline in rates may seem small in absolute terms, it can make a significant dent in the earnings of regular-income seekers. In the short term, retirees may continue to withdraw amounts in line with their growing needs as a result of inflation; however, their corpus cannot generate enough interest to last as long as they will need it to and poverty becomes a very real possibility. Thankfully, there is a solution, and this involves investing both in equity and in fixed income.

But first, let's understand the problem better with an example. The other day I met my uncle. He looked worried. I asked him if everything was okay. He told me that he was worried about the incessantly falling interest rates on fixed deposits. He said that the fixed deposit of Rs 50 lakh that he had made three years ago fetched him around Rs 30,000 per month at the then prevailing rate of about 7.50 per cent. But recently, when he renewed the deposit, he found that the rate had dropped to 6.75 per cent. This caused a drop of around 10 per cent in his monthly income. So while his living expenses are on the rise, his income has actually shrunk. This is keeping him awake at night.

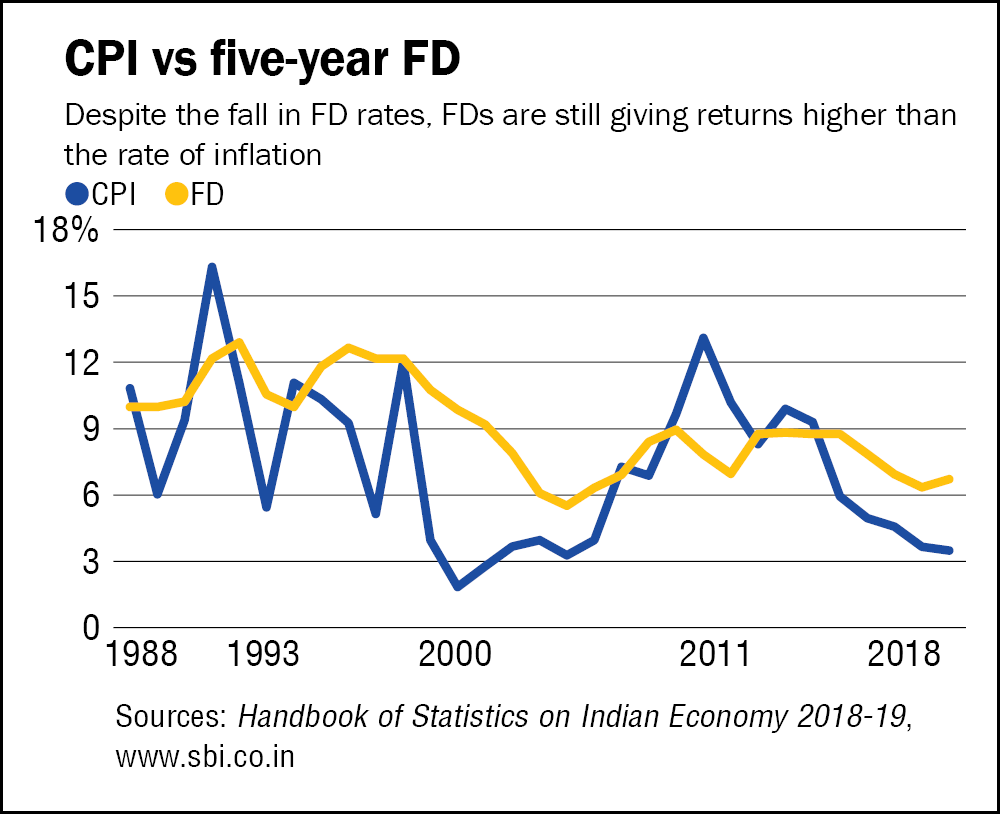

Before we get to a solution, let's look at how rate cuts impact real returns, that is returns earned after adjusting for inflation.

The graph above shows the spread between inflation and the average rate of return on a five-year fixed deposit. Despite the fall in FD rates, FDs are actually yielding better real returns now than at any other time in the recent past. However, the official inflation rate is calculated on a fixed basket of goods and services that make up the Consumer Price Index (CPI). But the composition of your household expenses could be quite different from this.

For instance, healthcare expenses account for only a five to six per cent weight in the CPI. But medical bills and other healthcare expenses are likely to take up a much higher proportion of a retiree's monthly budget. And since the health inflation is much higher than the CPI, this will automatically contribute to a sharper rise in the cost of living for a retiree. This is why you need to factor a higher personal inflation rate into your investment plan.

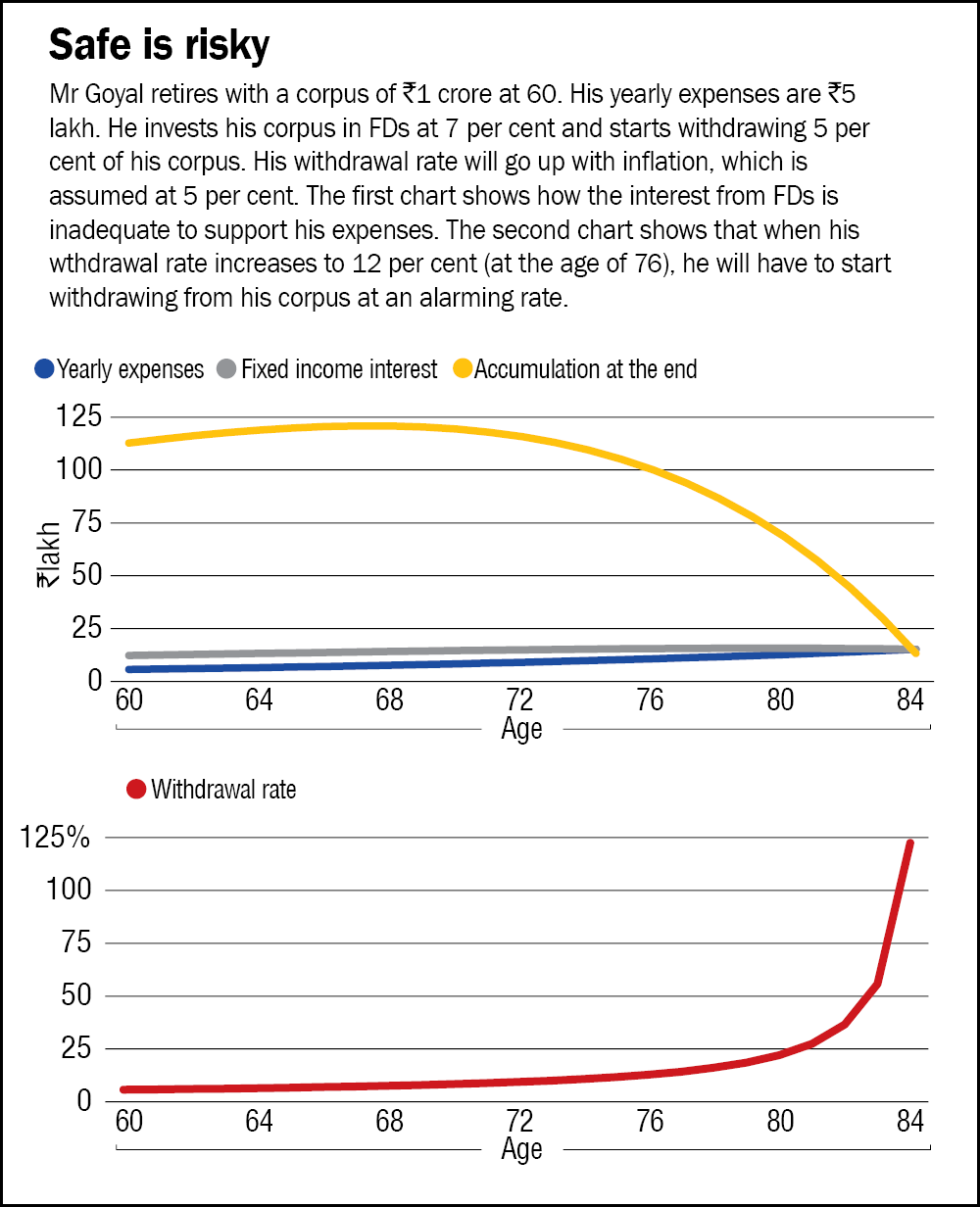

In order to get a better grip of the situation, let's look at another example. Mr Goyal retires today with a capital accumulation of Rs 1 crore as retirement savings. His annual expenses are around Rs 5 lakh. He puts the entire corpus in a bank fixed deposit yielding seven per cent. Now if inflation were to remain around five per cent, which is well within the RBI's target range, here is how his retired years would look.

In the first year, accommodating for his expenses of Rs 5 lakh, his interest income will increase his accumulation to about Rs 1.02 crore. However, in subsequent years, the fixed-income interest will no longer be adequate to meet the rising expenses.

This dependence on a fixed deposit will take him through a good 20 years of retirement. But after that, Mr Goyal will start dipping rapidly into his own capital and eventually end up outliving it (see the graph 'Safe is risky').

This is a dire situation indeed, but one that can be prevented through an investment plan that includes both fixed income and equity. We show what such a plan might look like in the story 'The ultimate portfolio for a retiree.'

This article was originally published on January 01, 2020.

Ask Value Research ![]()