If you have invested in an actively managed large-cap scheme, you might have noticed its dramatic underperformance last year. In 2018, market indices gave actively managed equity funds a run for their money. All of the 31 funds in the actively managed large-cap category struggled to beat the S&P BSE Sensex TRI. This category-wide underperformance has again sparked the question: is paying a higher fee for active management justified?

But to assess whether the underperformance by large-cap funds is a sustainable trend, looking at one-year returns through the lump-sum route is far from ideal. Many fund investors today take the SIP route, and the right period to judge the performance of any equity fund is at least five years, not one.

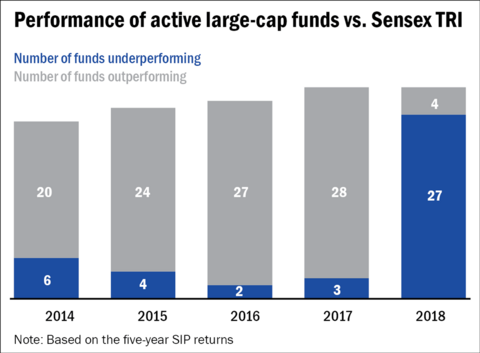

We compared the performance of actively managed large-cap funds with that of the S&P BSE Sensex Total Return Index (TRI) on the basis of five-year SIP returns at the end of each of the last five calendar years. The analysis showed that while the five-year block ended 2018 didn't see active-fund SIPs beating the index, they did manage the feat until 2017. In the five-year blocks ending 2014 to 2017, over 80 per cent of the active large-cap funds outperformed the S&P BSE Sensex TRI (see the first graph).

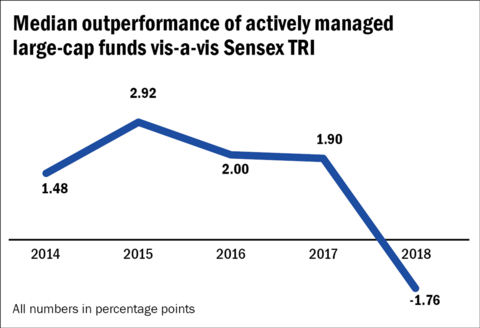

2018 was an exceptionally harsh year for active managers. It was a year when the returns of the index itself didn't appear to represent the performance of its constituents, leave alone the market (see the box - Annual returns: The bigger picture to know why). With a narrow set of stocks powering the index, 27 of the 31 active large-cap funds lagged behind the index on the basis of their five-year SIP returns. But also noteworthy is the fact that their margin of outperformance has slipped steadily over these years (see the second graph).

So what does this tell investors? Actively managed large-cap funds are clearly under more pressure than they have been any time in the past to justify their higher expenses. They have to pull up their socks or risk losing the battle for investors' wallets to the lower-cost index funds and ETFs. But it would be premature to write them off.

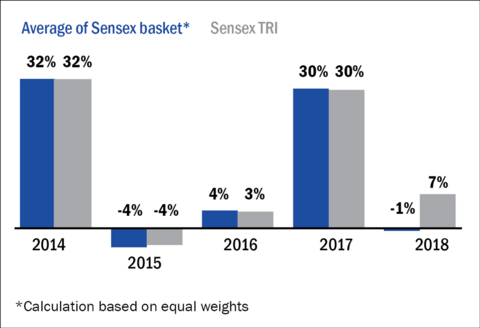

Annual returns: The bigger picture

2018 was a milestone year for passive funds. But it was an exception. The returns of the widely used benchmark S&P BSE Sensex TRI would make one believe that large-cap stocks were doing fine but that was only because of a handful of top-weighted constituents.

See the graph below. If you compare the average return of all the Sensex constituents weighted equally against actual index returns (using their assigned weights), the difference has widened substantially in 2018. The equal-weighted returns were negative while the index was in positive territory. This is because of strong performance by a handful of index heavyweights. A more diversified portfolio of stocks would often find it difficult to beat the index in such situations.

Bright spots

Amidst all the noise, there are a few funds in the category which have managed to beat the index by a fair margin quite consistently, too. The table lists the set of funds which have built an impressive record in the past five years by outperforming the index by more than 3 percentage points on the basis of five-year SIP returns, excluding the year 2018. Two of these have been able to outsmart the index even in 2018.

Consistent outperformers

| Scheme name | 2014 | 2015 | 2016 | 2017 | 2018 |

| Aditya Birla Sun Life Focused Equity Fund | 22.3 | 17.3 | 14.6 | 18.3 | 9.4 |

| Aditya Birla Sun Life Frontline Equity Fund | 20.9 | 16.7 | 14.4 | 18.0 | 9.8 |

| ICICI Prudential Bluechip Fund | 20.0 | 14.9 | 13.1 | 18.1 | 11.1 |

| Quant Focused Fund | 23.1 | 25.6 | 21.5 | 25.2 | 12.6 |

| Reliance Large Cap Fund | 22.0 | 17.7 | 13.6 | 20.0 | 12.3 |

| SBI Bluechip Fund | 21.0 | 19.6 | 15.7 | 18.9 | 9.8 |

| Sensex TRI | 16.2 | 11.0 | 8.7 | 13.8 | 11.2 |

| 5Y SIP returns at the end of each calendar year | |||||

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()