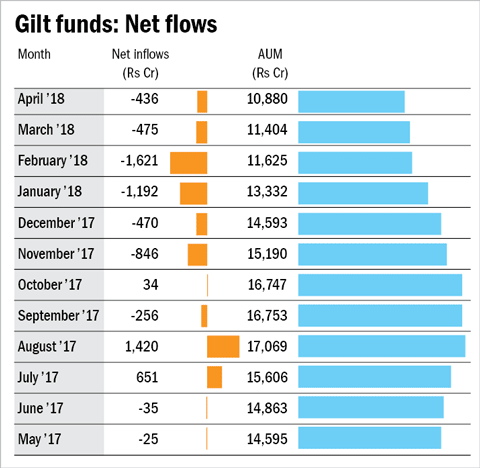

Investors continue to dump gilt funds. Popular with investors who expect interest rates to fall, gilt funds have in recent times have been a pariah among debt funds. The category has seen net outflows for the sixth straight month, one of the longest streaks in its history. AMFI data shows that over Rs 5,000 crore has flown out of debt funds, pushing assets under management of gilt funds to Rs 10,880 crore.

Gilt funds, as you may know, invest solely in government securities or G-Secs. Kotak Mahindra Asset Management Co. Ltd launched India's first gilt fund in December 1998. Thereafter many other fund houses like SBI, ICICI Prudential, Reliance, UTI, and HDFC joined the bandwagon to unveil their very own gilt funds.

Since G-secs are the most liquid of all instruments in the debt market, gilt funds are seen as debt schemes that carry virtually no credit risk because the Government of India is the borrower. Such schemes invest in various state and central government securities including securities which are supported by the ability to borrow from the treasury or supported only by the sovereign guarantee or of the state government or supported by GoI /state government in some other way.

But it is interest rate risk that has upset the gilt funds' applecart. The 10-year benchmark G-Sec yield moved up significantly in the last 8 to 10 months from almost 6.40 per cent level to as high as 7.80 per cent. Most of this yield movement has happened because of a combination of various factors starting with the concerns that began in August-September last year on the possible breach of the fiscal deficit target. This was followed by the up move in the oil prices from close to around $45-$50/barrel to around $75/barrel. Also, nationalized banks (who are the biggest buyers of G-Secs) post demonetization bought a large amount of G-Secs but incurred huge mark to market losses on most of that holding, forcing them to lose their appetite for G-Secs.

As per AMFI data, between November 2017 and April 2018, gilt funds have witnessed net outflows to the tune of Rs 5,040 crore. Assets have dropped from Rs 15,190 crore to Rs 10,080 crore. In the preceding six month period i.e. from May 2017 to October 2017, gilt funds saw net inflows of nearly Rs 1,800 crore.

Explaining the investor behavior, Lakshmi Iyer, CIO (debt) & head products, Kotak Mutual Fund says: "Outlook on interest rates remain uncertain.

Volatility in gilts is unnerving investors. Globally, yields are on the rise. Hence, some investors are choosing to stay out of such volatility. Also, those who have completed 3 years in such funds come under LTCG. So, there is another reason for exit." In case of debt mutual funds, a holding period of 36 months or more is regarded as long-term.

The movement of G-Sec yield has caught everybody by surprise. Yield and debt security prices move in opposite directions. Pankaj Pathak, fund manager - fixed income, Quantum MF said: "Although we had anticipated the rise in bond yields back in August 2017 but the extent of the surge in yields had been much higher than our anticipation. For bond markets, with the yields back up, valuations are getting attractive especially in the short tenor segment from 1to 5 years."

Going ahead, the market will closely watch the extent of Minimum Support Price (MSP) increases for the Kharif crops which will be available by May 2018. By that time, we would also get a clearer assessment of monsoons, which given the low water reservoir levels, assumes significance for food production and prices. The RBI policy for June 2018 thus holds major significance with implications on future rate trajectory.

Since gilt funds are like sectoral funds in the equity space, investment horizons should be long, preferably three years or more. There will always be phases where you will see a sharp rise in the yield once the rate cycle changes, and gilt fund net asset values (NAV) will reflect those movements.

Ask Value Research ![]()