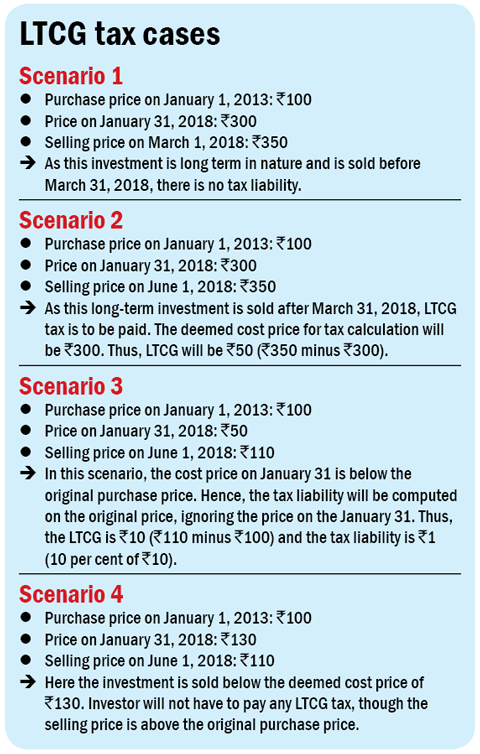

How does 'grandfathering' work for my equity SIPs?

All the capital gains accumulated on your long-term SIPs until January 31, 2018, will be exempt from LTCG tax. But calculating this 'grandfathered' portion of LTCG for SIPs poses a real challenge. It requires you to arrive at the acquisition cost for all the SIP instalments you have made so far on each of your equity funds. Provided you've made a profit, you then deduct this acquisition cost from the January 31 market value (NAV) of the accumulated units.

But this is easier said than done. While obtaining the January 31 NAV for your funds is easy enough (your NSDL CAS statement will provide it), finding out the cost of acquisition for all of your SIP instalments over the years is a tall order. It is also not clear if one must apply first-in-first-out principles to arrive at the gain.

Given this problem, if you use the services of a distributor or an advisor for your mutual fund investments, it would be best for you to request them for a capital-gains statement on all your mutual fund holdings. If you are a direct investor, your life is tougher and you may have to place a request with individual AMCs to get your hands on this data.

Why shouldn't I just sell all my equity funds before April 1 so that I can avoid this LTCG tax?

That's a bad idea for three reasons. One, you've probably invested in those equity funds to meet specific long-term goals like your children's education or retirement. Therefore, if you sell your entire equity portfolio today, you will have to look for other asset classes that can match those funds' returns over the next several years (on a post-tax basis) to get you to your long-term goal. This is quite challenging, especially if the interest rates in the Indian markets are going to head lower in the long run. There's no point in selling equity funds now and buying them back later because you will eventually end up paying the same LTCG tax on your equity gains.

Two, arriving at a comfortable asset allocation and choosing the right equity funds to suit your temperament and return expectations is no easy task. So, if you are happy with your current returns but decide to suddenly liquidate your portfolio to avoid tax, you will have to devote a lot of time and effort to rebuilding your portfolio from scratch. Remember, a falling market is the ideal time to add to your equity holdings and not to sell them! Plus, if you make mistakes in your allocation or fund selection during this major rejig, it may cost you dear on returns in the long run.

Three, by slapping a 10.4 per cent tax on equity funds without indexation, the FM has made it very important indeed for equity fund investors to keep the churn in their portfolio to a minimum. After April 1, each time you sell one set of funds you've held for long and buy another, you will end up shelling out 10.4 per cent of those gains to the taxman. If you change those fund choices two or three times a year, instead of paying 10.4 per cent tax on your profits, you will end up paying 15.6 per cent (short-term capital-gains tax) or even a multiple of that. Churn too often and all your hard-earned gains will be happily swallowed up by the taxman!

But yes, selling your funds before April 1 makes sense if you are unhappy with the performance of any of your funds and were anyway looking to sell them. If you were planning to rebalance your asset allocation this year, then doing it before April 1 is good, too. If you have investment goals coming up in the next one year, for which you need cash, it again makes sense to take advantage of the window up to April 1.

Don't worry about double taxation!

How unfair is LTCG

Ask Value Research ![]()