Note: This article has no recommendation to either buy or avoid this IPO. Instead, we have presented all the relevant information based on which you can make your own decision.

What is reinsurance

Reinsurance is secondary insurance. An existing insurer 'cedes' the premium on a policy it has written and also passes the risk on to the reinsurer. Non-life insurers in India are obliged by the IRDA to cede at least 5% of their policies to a reinsurer.

Background

GIC or General Insurance Corporation of India was incorporated in 1972 as a general insurer and converted itself to a reinsurer (exclusively) in 2000. It is India's largest reinsurance company in terms of gross premiums and accounts for 60% of the premium ceded to reinsurers.30% of its gross premiums were connected to risks outside India. GIC makes money by collecting premiums and investing them in various assets. It is an efficient operation with a return on equity of 16%. This was above 15% in both 2016 and 2015.

GIC's Indian assets (the bulk of its portfolio) have a fair value of Rs 69,162 crore. Its investment portfolio is split 25:75 between equity and debt. About 54% of its equity investments are in Nifty 50 companies. About 53% of its debt portfolio is invested in bonds with a maturity of 5 years or more.

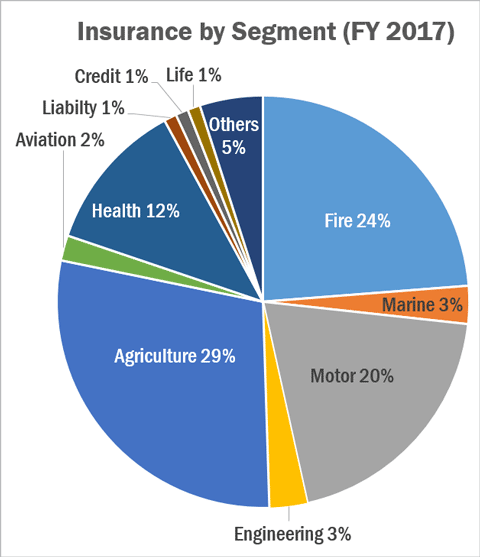

The share of agriculture in GIC's premiums has shot up dramatically, driven by the government's push for crop insurance (think Pradhan Mantri Fasal Bima Yojana). The premiums for crop insurance are subsidised heavily by the government. The share of agriculture in GIC's segment basket was about 4% in 2015.

GIC accounts for almost half of the reinsurance market for agricultural insurance in India. Its policies covered 30% of India's gross cropped area in FY 2017 according to the General Insurance Council of India.

GIC's top 10 clients accounted for 56% of its premiums.Its top client was the Agricultural Insurance Company of India (in which it has a 35% stake) followed by National Insurance Company and ICICI Lombard Insurance.

Strengths

Industry leader - GIC commands 60% of the Indian reinsurance market. It has a presence in over 160 Countries and a diversified risk profile.

Cost Efficiency - It's a low-cost operator with net expense ratio of 21.3% (how much net premium is spent on operating expenses and commissions) while the average for its peers is 33.7%.

Capital Buffer - GIC has a solvency ratio of 2.41 compared to the statutory requirement of 1.5. However, this has fallen from 3.32 in 2015. The solvency ratio tells us how an insurance company will fare if all its liabilities and claims become due at the same time.

Investments - GIC has a large investment base of 69,162 crores on which it generated a net yield of 7.8% in FY17 compared to its peers' average of 3.8%. It had a 5-year average net yield of 8.7%. This investment base not only generate decent returns but also help the company support its liabilities and claims.

Weaknesses

Dependant on Investment Income - The Combined ratio of the company is 100.16% meaning that it's paying more in claims and expenses then the premium it's collecting. Though the company is operationally profitable, but that is more due to its investment income. However this has fallen from 107.03% in 2016 and 108.8% in 2015.

Association with Related party - 13% of GIC's gross premium is from the Agricultural Corporation of India (Primarily due to Pradhan Mantri Fasal Bima Yojana). Excessive dependency on one customer and one segment (agriculture) can cause significant pain in case of draughts or floods causing liabilities to arise.

IRDA Regulations - Insurance have a legal obligation to buy a certain level of reinsurance. IRDA has mandated that 5% of non-life insurance has to be reinsured.This rate has been reduced from 20% in 2006 to 5% in 2013. Any further reduction would affect GIC's business.

Increasing competition - Subsequent to the decision to allow foreign reinsurers to set up branch offices in India, many renowned international reinsurers like Swiss Re, Munich Re have set up shop. As more competition creeps in, pricing pressure on GIC would increase.

Valuation - Globally reinsurance companies are valued in relation to their book value. For GIC this is about 4x at its current price band while its peers' average of 1.3 times book value. It''s price to equity also comes to about 24.

Who's selling and why

The Government of India currently has nearly 100% ownership. Post the IPO its holding would come down to around 86%.

The IPO also comprises of fresh issue totalling to 1570 crores at the higher band, which would be used for increasing GIC's capital base and for general corporate purposes

Issue Dates: 11th-13th October, 2017

Ask Value Research ![]()