MAS Financial services is a lender (a non-banking finance company, to be exact). It began operations in 1995 with a focus on microfinance and has come a long way since then. It gives out small loans for the purchase of houses, commercial vehicles and two-wheelers. It also lends to businesses for their working capital requirements or machinery purchases. MAS is modestly sized at an AUM (Assets under Management) of 3,451 crore.This AUM has grown at a scorching 33% since 2013. MAS has more than 500,000 active loan accounts across six states and the NCT of Delhi. However, its operations are concentrated in Gujarat and Maharashtra. It directly lends about half its AUM and gives out the rest to other NBFCs, Housing Finance Companies and microfinance institutions.

MAS Financial services is a lender (a non-banking finance company, to be exact). It began operations in 1995 with a focus on microfinance and has come a long way since then. It gives out small loans for the purchase of houses, commercial vehicles and two-wheelers. It also lends to businesses for their working capital requirements or machinery purchases. MAS is modestly sized at an AUM (Assets under Management) of 3,451 crore.This AUM has grown at a scorching 33% since 2013. MAS has more than 500,000 active loan accounts across six states and the NCT of Delhi. However, its operations are concentrated in Gujarat and Maharashtra. It directly lends about half its AUM and gives out the rest to other NBFCs, Housing Finance Companies and microfinance institutions.

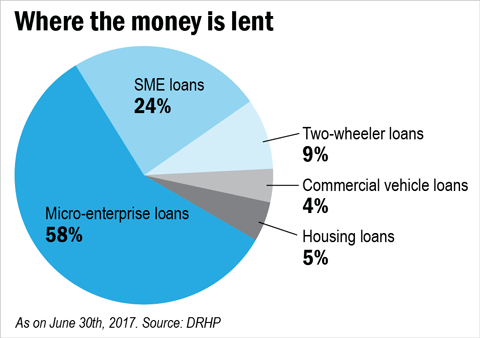

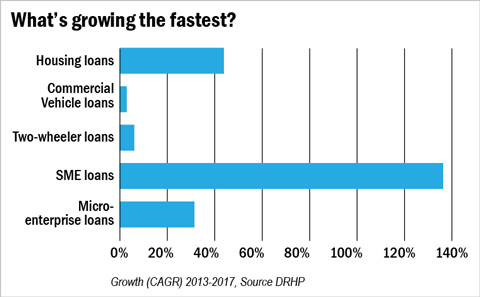

Here's a sectoral break-up:

As the figure above shows, a huge portion of the company's lending goes to business whether micro (under micro-enterprise loans) or small (under SME). In a sign of a maturing economy, it is the SME segment that's growing the fastest.

Advantages

MAS has lent its money fairly prudently. It has a gross NPA ratio of just 1.14%. Its agents share in its losses, if loans raised through them turn bad. It has a fairly diversified portfolio in sectoral terms (though not geographically) with money going into housing, vehicles and businesses. Its revenues and profits have grown at a CAGR of 26% and 32% respectively from FY13-17. India's push for affordable housing finance holds out a route to rapid growth in this segment.

Disadvantages

MAS has plenty of indirect exposure to agriculture through its SME and micro-enterprise loans. It is trying to increase this by moving further into financing agricultural equipment. This leaves it vulnerable to India's farm loan waivers. These waivers might not hit it directly but can trigger a behavioural change among its small borrowers in rural India. It is also heavily concentrated in Gujarat and Maharashtra which leaves it exposed to local politics in the way that the erstwhile SKS Microfinance was. The company's Net Interest Margin (NIM) has been steadily falling over the years. Not being a bank forces it to borrow money at a fairly high cost. Its cost of capital of 9.45% is fairly high compared to its peers. They have either become banks (such as Bandhan and Ujjivan) or are planning to merge with one (such as Bharat Financial Inclusion).

Who's selling and how much

Fresh Issue: 233 crore (To increase its capital base)

Offer for Sale: 227 crore (by DEG, FMO and Sarva Capital)

Current Ownership

Promoters: 80.7%, DEG- 5% , FMO -3.5%, Sarva Capital- 2.6%, Others: 8.2%

Post-Issue ownership

Management

- Has the company been free of any regulatory penalties?

Yes. However, the RBI has made adverse observations about the company's non compliance with credit concentration, high leverage and its charging higher interest to SMEs. - Does the company adequately provide for its Non-performing assets (NPAs)? More specifically, is the ratio of provisions to Gross NPAs more than 50%?

No, based on five year average MAS only made provision for 32% of Gross NPA during 2013-17. - Do the top five managers have stock as meaningful part of their compensation (More than 50%)?

No. MAS do not have any employee stock options scheme (ESOP). ESOP`s (provided they are awarded within reasonable limits) ensure that interest of management is aligned with that of shareholders. This is important in finance companies where non performing assets (NPA) can erode shareholders wealth.

Financial Strength and stability

- Does the company have a fresh slippages to total advances ratio of less than 0.25%? Fresh slippages are loans which have become NPAs in the last financial year.

No, MAS had fresh slippages of 0.27% of its last year's AUM. Its increasing focus on agriculture can cause them to accelerate as the sector remains vulnerable to climatic volatility and political decisions such as farm loan waivers. - Did the company generate a current and 4-year average return on equity (RoE) of more than 12 per cent and return on assets (RoA) of more than 1 per cent?

Yes, company generated four year average ROE and ROA of 36% and 3% respectively adjusted for dilution by preference shares. - Did the company increase its loan book by 20% annually over the last four years?

Yes, MAS increased its loan book at healthy CAGR of 33% during from 2013-17. - Did the company increase its Net Interest Income (NII) by 20% annually over the last four years?

Yes, the company's net interest income increased at CAGR of 23% during 2013-17. - Is there a direct relationship between the increase in loan book and the increase in Net Interest Income (NII)?

Yes, from the past two years increase in loan book has been closely followed by increase in net interest income, though this was not so in the two years that preceded it. - Is the company's capital adequacy ratio more than 15%?

Yes, as of June 30,2017 its capital adequacy stood at 23.8% in comparison to 15% mandated by RBI. - Can the company run its business without relying on external funding in the next three years?

Yes. The company's overall growth rate, the proceeds it is gathering from the IPO and the company's comfortable capital adequacy position do not give us cause to believe otherwise. - Did the company generate average NIM of more than 3% in last 5 years?

Yes, MAS generated average net interest margins of 8.3% during last five years. However its NIM currently stands at 7% and has been steadily falling. - Is the Average Gross NPA Ratio (Gross NPAs/Total Advances) over the last 3 years less than 1% and the Net NPA Ratio (Net NPAs/Total Advances) less than 0.5%?

No, its three year average gross and net NPA ratios stand at 1.03% and 0.87% respectively. Its current Gross and Net NPA ratios are also above these thresholds. - Does the company have a cost-income ratio of less than 50%?

Yes, its cost to income ratio currently stands at 29% which is lower than 5 year average of 32% indicating increased operational efficiency.

Growth and Business

- Will the company be able to scale up its business?

Yes. India still has relatively low micro-finance penetration. MAS is geographically concentrated in Gujarat and Maharashtra offering a large opportunity for geographic expansion. It will also be able to generate growth through segments such as housing-finance. - Does the company have a loan book of more than Rs 100,000 crores?

No, MAS has a loan book of Rs 3,330 crores. - Does the company have a recognizable brand, truly valued by its customers?

No, it is a small company operating in a highly competitive industry where interest rates play a very vital role. Player offering lower interest rates will capture the market. - Does the company have a credible moat?

No, size is a big moat in the lending business with big and well-diversified lenders protected better from defaults. MAS is a small company with a small book size and with little ability to withstand major financial shocks. - Is the level of competition faced by the company, relatively low?

No, it operates in a highly competitive industry. It faces stiff competition from large banks, small finance banks, non banking financial companies and microfinance companies.

Valuation

- Is the company's price to earnings ratio less than its peer median level?

No, its PE is 36 times based on post IPO diluted earnings compared to a median PE of 19 times for its peers. - Is the company's price to book value less than its peer median level?

No, its price to book stands at 4.3 times based on post IPO diluted book value. This is just 2.75 for its peers on average. - Is the company's PEG ratio less than 1?

No, its PEG ratio stands at 1.25 times based on 4 year CAGR earnings growth.

One or more authors may have subscribed to this IPO.

Ask Value Research ![]()