Note: This article has no recommendation to either buy or avoid this IPO. Instead, we have presented all the relevant information based on which you can make your own decision.

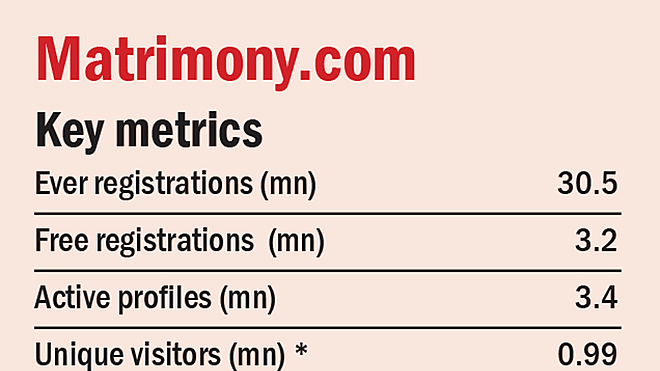

About 30% of the population of India is within marriageable age. 11.70 million marriages took place in 2016 of which 88% were 'arranged marriages'. Internet portals accounted for just 6% of them, a drop in a very large bucket. Matrimony.com is the largest among these portals with about 3 million registered users and nearly 1 million unique visitors each month. Of course, not all of them are paid subscribers but a good number are - about 700,000 people.

Matrimony is India's largest wedding portal and possibly its oldest (launched in 2001). The website has a fairly compelling pull factor. After subscribing, users can send personalized messages to other users, view verified mobile numbers, chat and in case you were wondering, compare horoscopes. For users who aren't comfortable with a wholly online experience, the company has a workforce, spread across 140 retail centers to help (incidentally called 'relationship managers'). The site also has a real time 'recommendation engine' called MMA that uses algorithms and machine learning to help users find life partners. For its numerous services, Matrimony's subscribers pay it a hefty Rs 4242 on average. The company has tried its hand at related products such as wedding gifts, venues and assorted services but hasn't seen much success with them so far.

Matrimony.com is a strange beast. It made a profit of 44 crores on 293 crores of revenue in FY 2017. However, if you go back to the last four years, it made losses in each of them. It employs an astonishing 4212 people, many of whom are spread across its retail centers to help customers who aren't net savvy. Wages account for a whopping 40-50% of its costs. A festering dispute with an investor in its US operation accounted for losses in two of the past four years. The company is also facing regulatory wrangles concerning the alleged transfer of funds outside India through its promoter in contravention of the FEMA and an alleged transfer of assets to its promoter below 'fair value'.

Nonetheless, you may see that the negatives outweigh the positives. Our questions will help you navigate.

Where the money's going?

- IPO Size - Rs 500 crores

- Promoters get 12%

- PE Funds get 63%

- Matrimony.com gets (Fresh Issue of Shares) 25%

- The company plans to use the money to invest in a new office, for advertising, to repay outstanding overdrafts and for general corporate purposes

Company / Business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

No. The earnings before tax were Rs 44 Crores for the past 12 months.

2. Will the company be able to scale up its business?

Yes. Since this is an internet business, scaling up both geographically and product-wise should not be an issue. Its efforts in this direction include the provision of marriage services such as wedding photography, mandap booking etc via its affiliated platforms.

3. Does the company have recognizable brand(s), truly valued by its customers?

Yes. The company has recognisable brands like BharatMatrimony. It benefits from a first mover advantage and possesses the largest profile database in the industry.

4. Does the company have high repeat customer usage?

No. Since marriages are a one-time affair (generally), once the customer has found his/her soulmate, they would not come back to Matrimony.

5. Does the company have a credible moat?

No. It is relatively easy for new players to set up competing databases and services

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No.The company keeps confidential data of individuals who have created profiles on its platform and any changes in laws related to data privacy and data security can affect its business operations significantly.

7. Is the business of the company immune from easy replication by new players?

No. By aggressively marketing its platform or through free services, a new entrant can replicate its business.

8. Is the company's product able to withstand being easily substituted or outdated?

No. The company provides matchmaking and marriage services. The only long term threat to them is the demise of arranged marriages in India. Social habits and preferences such as arranged marriages do not easily alter and in any case, take a long time to change.

9. Are the customers of the company devoid of significant bargaining power?

No. Its customers are free to choose any platform for this need. They in effect provide content to the company and are not bound by any exclusivity with the company's portal.

10. Are the suppliers of the company devoid of significant bargaining power?

No. The company's suppliers are providers of search rankings and web hosting. The company relies on search engines such as Google to drive customers to its website. There have been instances in the past where Google showed sponsored links to pages of rival portals if users searched for bharatmatrimony or other sites owned by the company. The company entered into litigation about this practice which is currently ongoing. The practice has been halted by Google for the time being.

11. Is the level of competition the company faces relatively low?

No. The company faces tough competition from not only from online platforms like shaadi.com but also from traditional marriage bureaus and classified ads in newspapers.

Management

1. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes. The founder/promoter Murugavel Janakiraman holds 55.57% of the company.

2. Do the top three managers have more than 15 years of combined leadership at the company?

Yes. Two out the top three managers have a combined experience of 28 years with the company. However, during the past 12 months, employees holding key positions in the company have left it.

3. Is the management trustworthy? Is it transparent in disclosures which are consistent with Sebi?

Yes, we have no significant reason to believe otherwise.However, in the past. the company has settled claims made by Mr Rajan Desai and Real Soft, Inc. who had invested in it and claimed an award of an equity interest in 'bharatmatrimony.com' and a constructive trust on 'bharatmatrimony.com' and all associated businesses alleging siphoning of assets from USA. The company has settled the aforementioned case by paying an amount of 53 Crores in 2016.

4. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

No. A few pending cases related to Provident Fund and FEMA regulations are particularly worrisome. According to the RBI, the company allegedly transferred shares of a subsidiary to its promoters at less than fair value and funded entities outside India owned by its promoters without complying with FEMA norms. Both cases are still ongoing.

5. Is the company's accounting policy stable?

Yes, we have no reason to believe otherwise. However, In 2014, the company wrote off its accumulated losses through securities premium with a special court permission (in effect recognizing a burn through of its share capital). The write-off didn't fully absorb its accumulated losses.

6. Is the company free of promoter pledging of its shares?

Yes, no promoter holding is pledged.

Financial

1. Did the company generate current and five-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

No. The company had negative net worth as well as negative capital employed during the past 5 years.

2. Was the company's cash flow-positive during the previous year and at least four out of the last five years?

No. The company had positive cash flows during the previous year. However, the cash flows has been negative in 2 out of the previous 4 years.

3. Did the company increase its revenue by 10 per cent CAGR in the last five years?

No. The revenue of the company has grown from Rs 188 Crores in 2013 to Rs 293 Crores in 2017 translates into a CAGR of 9.18%.

4. Is the company's debt-to-equity ratio less than 1 or is its interest coverage ratio more than 2?

Yes.The company has no long term borrowings as on June 30, 2017. As on March 31, 2017 its interest coverage ratio was 11 times.

5. Is the company free from reliance on huge working capital for day to day affairs?

Yes.The company receives subscription fees from customers in advance which are used to run day to day operations of the company. It has a negative working capital of 72 crores and a negative cash conversion cycle meaning it gets paid by customers before it pays suppliers, a very comfortable position indeed.

6. Can the company run its business without relying on external funding in the next three years?

Yes. The company funds the business primarily through internal cash generated from operations. However, the company has previously raised short term borrowings to pay off litigation claims and a legal settlement.

7. Have the company's short term borrowings remained stable or declined (not increased by greater than 15%)?

No. After decreasing by 42% in 2014, short term borrowings shot up by 80% in each of the next 2 years. As on June 30,2017 the short term borrowings stood at Rs 43 Crores.

The Stock/Valuation

1. Does the stock offer operating earning yield of more than 8 per cent on its enterprise value?

No, the post IPO operating earnings yield of the company will range from 0.86%-0.85% based on the price band range.

2. Is the stock's price to earnings less than its peers' average level?

Not Applicable. There are no suitable listed peers for Matrimony.com. At a price band of Rs 983-985, it's PE will range from 48.2-48.3.

3. Is the stock's price to book value less than its peers' average level?

Not applicable. There are no suitable listed peers for Matrimony.com. Also, the company has negative net worth (book value) currently and for the past 4 years.

Ask Value Research ![]()