Many investors feel that looking at a company's basic financial statements suffices. However, what is easily available to us may not be the perfect information. Sometimes we have to remove the veil of reported numbers to see the real picture.

Consider the companies charging high depreciation, amortisation, impairment or other non-cash expenses in their profit-and-loss accounts. As depreciation or other non-cash expenses go up, the resulting net profit decreases and the stock's price-to-earnings (P/E) ratio looks high. At times, this can be misleading and investors might overlook a good investment opportunity due to an artificially high P/E ratio.

Depreciation is one of the most frequent non-cash charges seen in companies' accounts. Companies involved in heavy engineering or construction activities have to spend huge sums of money upfront on their projects, which start generating revenues only after a few years. This initial expenditure is transferred to the company's balance sheet under 'fixed assets' and every year a 'depreciation expense' is charged in the profit-and-loss account till the useful life of the project/asset.

However, it is the management's discretion to decide the useful life of an asset. Hence, the depreciation expense can also be changed, inflating or deflating the reported profit numbers. Thus, it makes sense to add back all non-cash expenses to the net profit of a company and calculate the cash EPS. An easy way to calculate cash EPS is using the cash flow from operations.

Cash EPS = (Net profit + Depreciation)/Number of shares outstanding

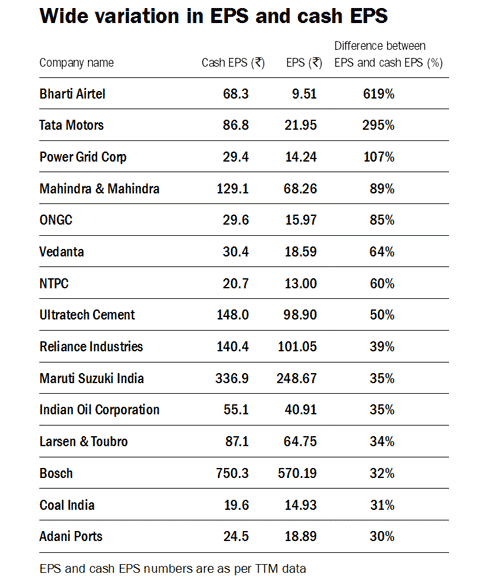

The table lists the companies where the difference between the cash EPS and the EPS is huge. That is, depreciation is more than 50 per cent of the profit before taxes. These companies have earned more cash than what appears in their net-profit numbers.

Ask Value Research ![]()